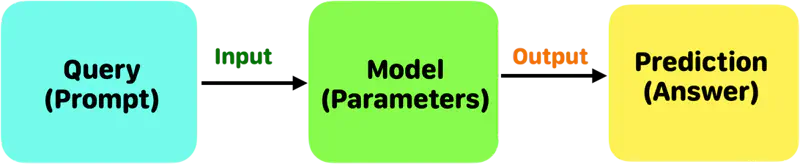

To gain knowledge or understanding of a skill, by study, instruction, or experience.

Machine Learning

To teach computers 💻 to learn from data, find patterns 🧮, and make decisions or predictions

without being explicitly programmed for every task, as humans🧍♀️🧍 learn from experience.

Phases of Machine Learning

The machine learning lifecycle ♼ is generally divided into two main stages:

Training Phase

Runtime (Inference) Phase

Training Phase: Where the machine learning model is developed and taught to understand a specific task using a large volume

of historical data.

Runtime (Inference) Phase: Where the fully trained and deployed model is put to practical use in a real-world 🌎 environment, i.e.,

to make predictions on new, unseen data.

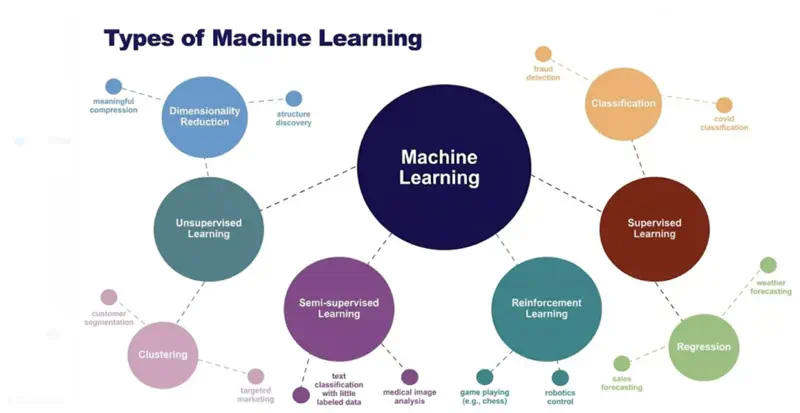

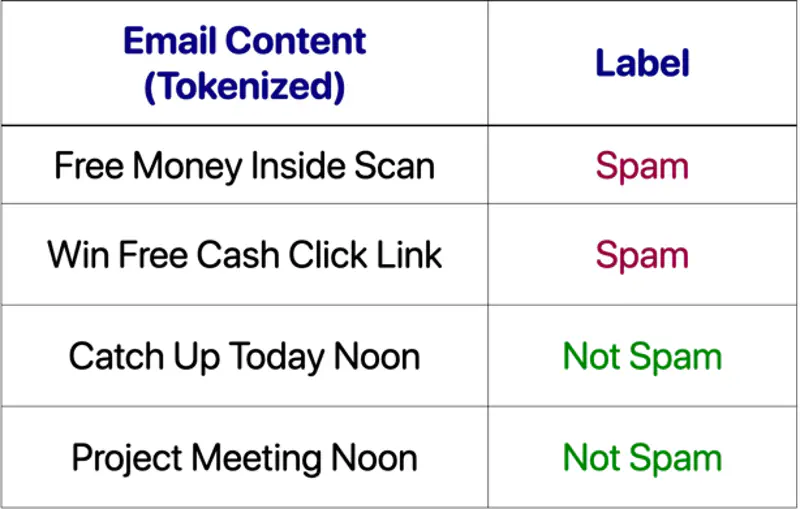

Supervised Learning uses labelled data (input-output pairs) to predict outcomes, such as, spam filters.

Regression

Classification

Unsupervised Learning

Unsupervised Learning finds hidden patterns in unlabelled data (like customer segmentation).

Clustering (k-means, hierarchical)

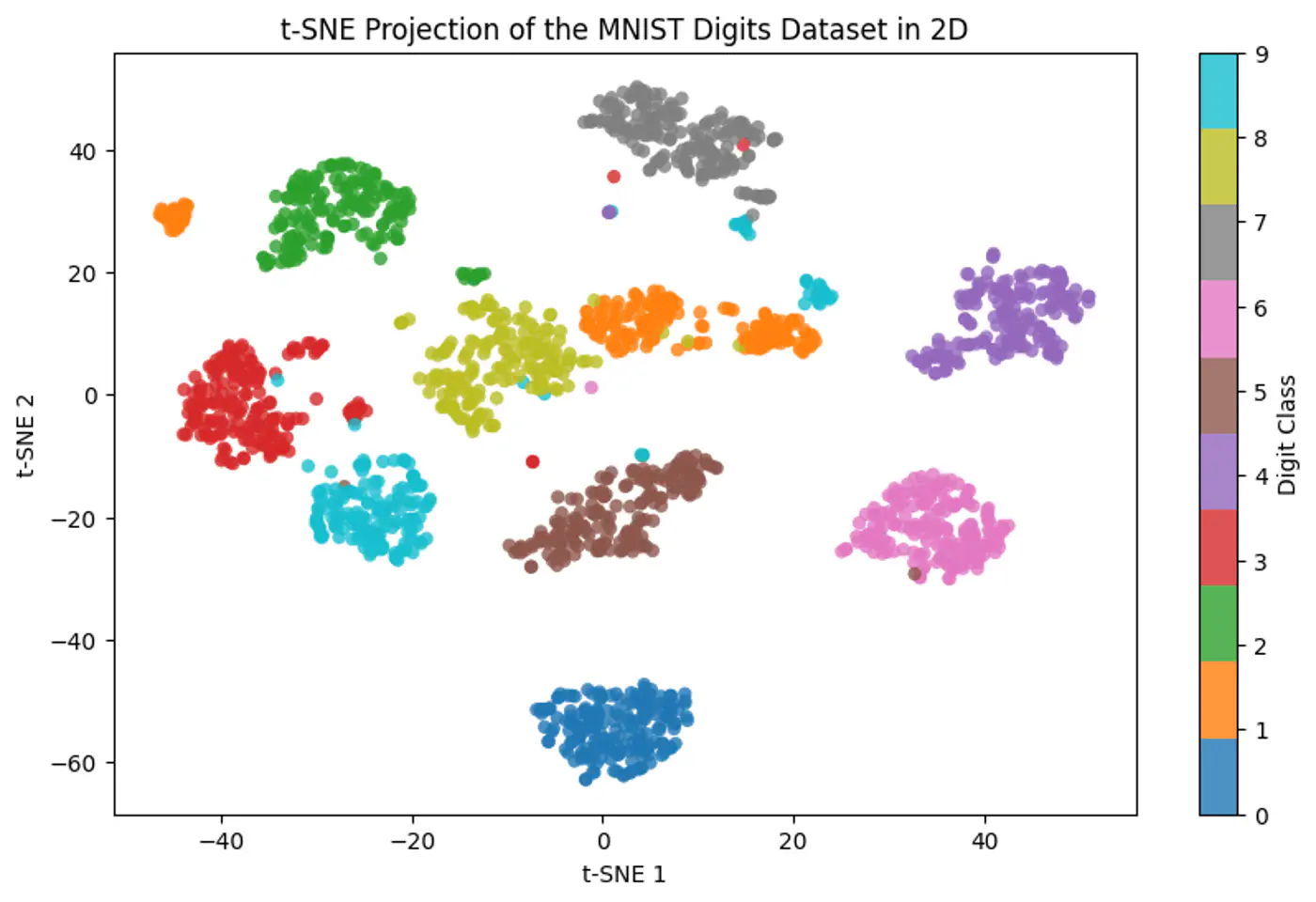

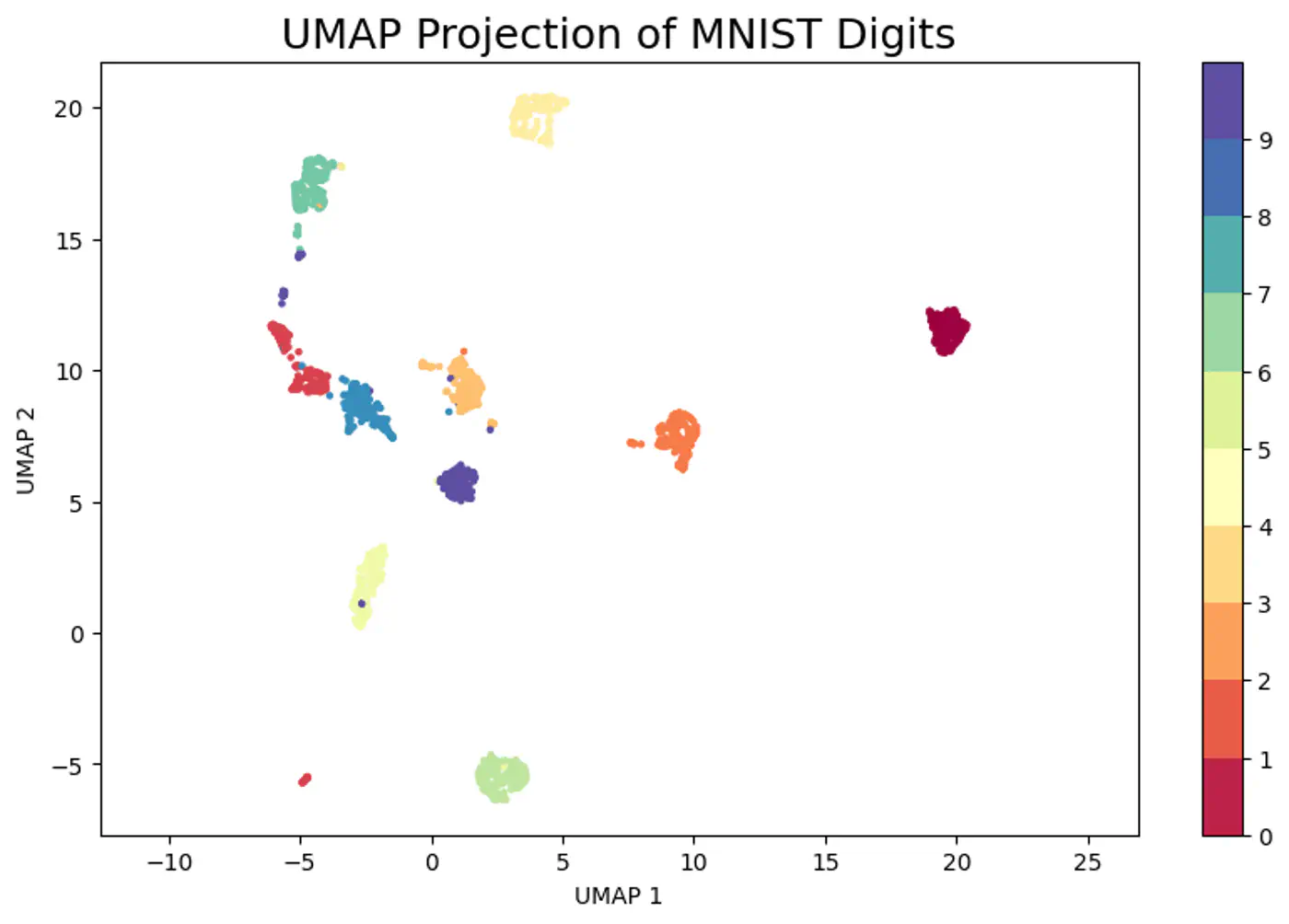

Dimensionality Reduction and Data Visualization (PCA, t-SNE, UMAP)

Semi-Supervised Learning

Semi-Supervised Learning uses a mix of both, leveraging a small amount of labelled data with a large amount of

unlabelled data to improve accuracy.

Pseudo-labeling

Graph-based methods

Types of Semi-Supervised Learning

1. Pseudo-labelling:

A model is initially trained on the available, limited labelled dataset.

This trained model is then used to predict labels for the unlabelled data.These predictions are called ‘pseudo-labels’.

The model is then retrained using both the original labelled data and the newly pseudo-labelled data.

Benefit: It effectively expands the training data by assigning labels to previously unlabelled examples,

allowing the model to learn from a larger dataset.

2. Graph-based methods:

Data points (both labelled and unlabelled) are represented as nodes in a graph.

Edges are established between nodes based on their similarity or proximity in the feature space.The weight of an edge often reflects the degree of similarity.

The core principle is that similar data points should have similar labels.This assumption is propagated through the graph, effectively ‘spreading’ the labels from the labelled nodes to the unlabelled nodes based on the graph structure.

Various algorithms, such as label propagation or graph neural networks (GNNs), can be employed to infer the labels of unlabelled nodes.

Benefit: These methods are particularly useful when the data naturally exhibits a graph-like structure or when local

neighborhood information is crucial for classification.

Reinforcement Learning

Agent learns to make optimal decisions by interacting with an environment, receiving rewards (positive feedback)

or penalties (negative feedback) for its actions.

Mimic human trial-and-error learning to achieve a goal 🎯.

Key Components of Reinforcement Learning

Agent: The learning entity that makes decisions and takes actions within the environment.

Environment: The external system with which the agent interacts.It defines the rules, states,

and the consequences of the agent’s actions.

State: A specific configuration or situation of the environment at a given point in time.

Action: A move or decision made by the agent in a particular state.

Reward: A numerical signal received by the agent from the environment, indicating the desirability of an action taken

in a specific state. Positive rewards encourage certain behaviors, while negative rewards (penalties) discourage them.

Policy: The strategy or mapping that defines which action the agent should take in each state to maximize long-term rewards 💰.

How Reinforcement Learning Works ?

Exploration: The agent tries out new actions to discover their effects and potentially find better strategies.

Exploitation: The agent utilizes its learned knowledge to choose actions that have yielded high rewards in the past.

Note: The agent continuously balances exploration and exploitation to refine its policy and achieve the optimal behavior.

Large Language Models

Large Language Models (LLMs) are deep learning models that often employ unsupervised learning

techniques during their pre-training phase.

LLMs are trained on massive amounts of raw, unlabelled text data (e.g., books, articles, web pages) to predict the next

word in a sequence or fill in masked words. This process, often called self-supervised learning, allows the model to learn grammar, syntax, semantics,

and general world knowledge by identifying statistical relationships within the text.

LLMs generally also undergo supervised fine-tuning (SFT) for specific tasks, where they are trained on

labeled datasets to improve performance on those tasks.

Reinforcement Learning from Human Feedback (RLHF) allows LLMs to learn from human judgment,

enabling them to generate more nuanced, context-aware, and ethically aligned outputs that better meet human expectations.

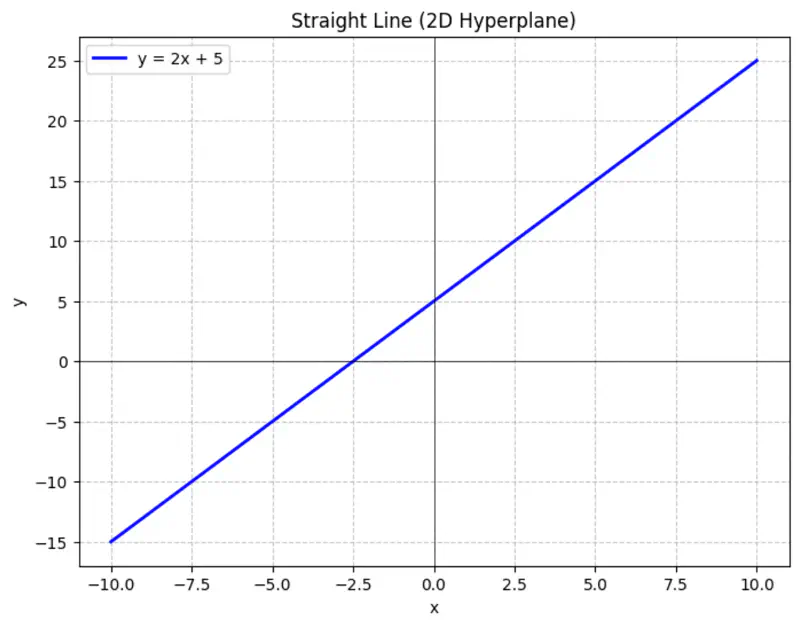

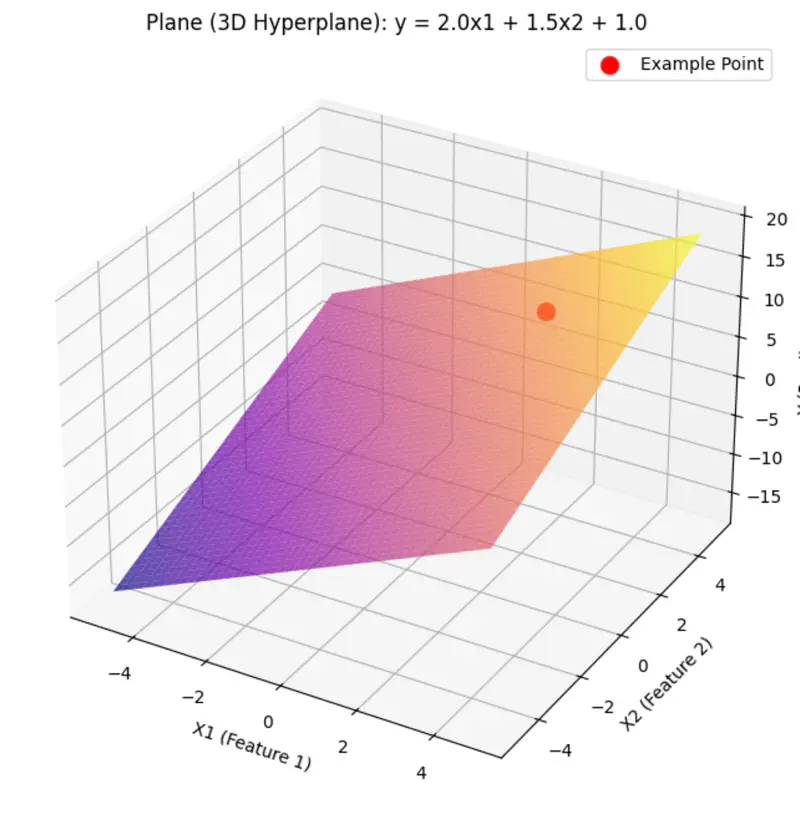

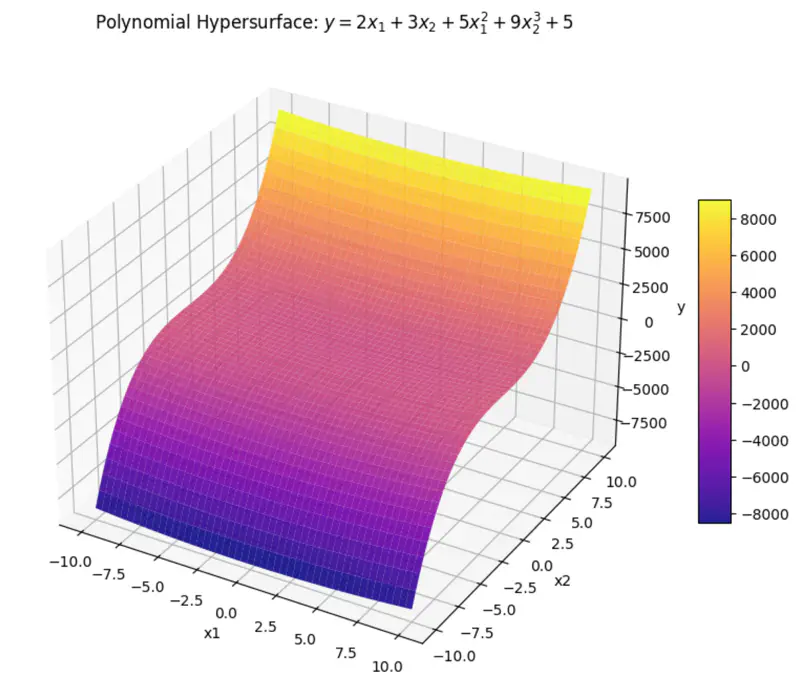

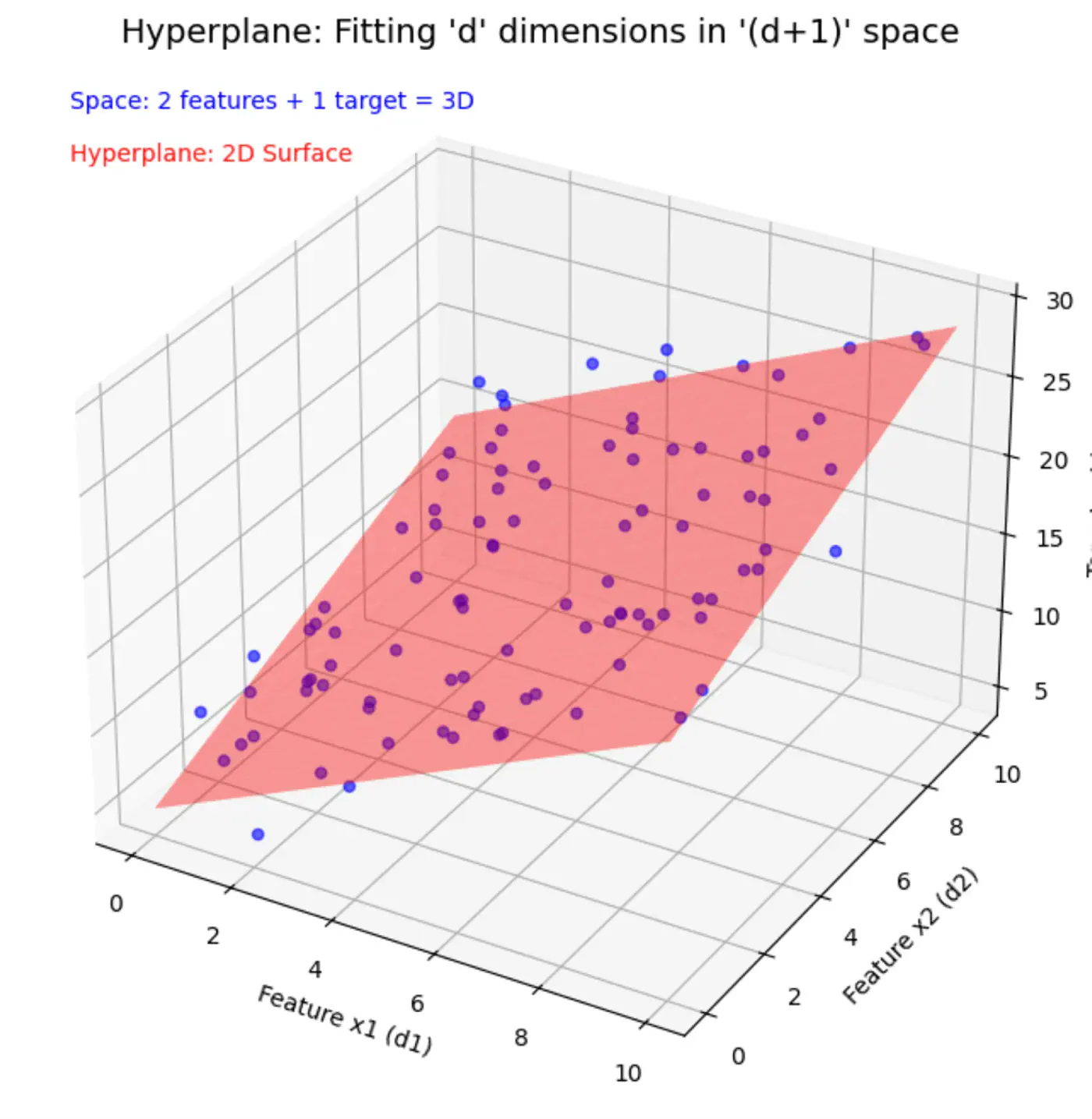

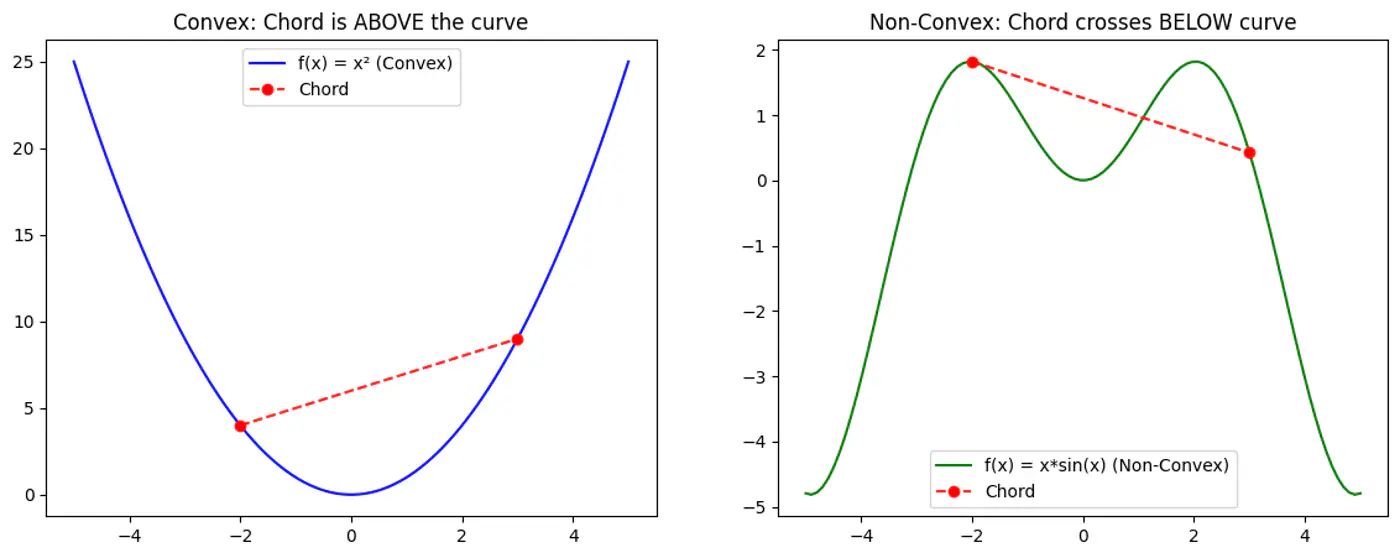

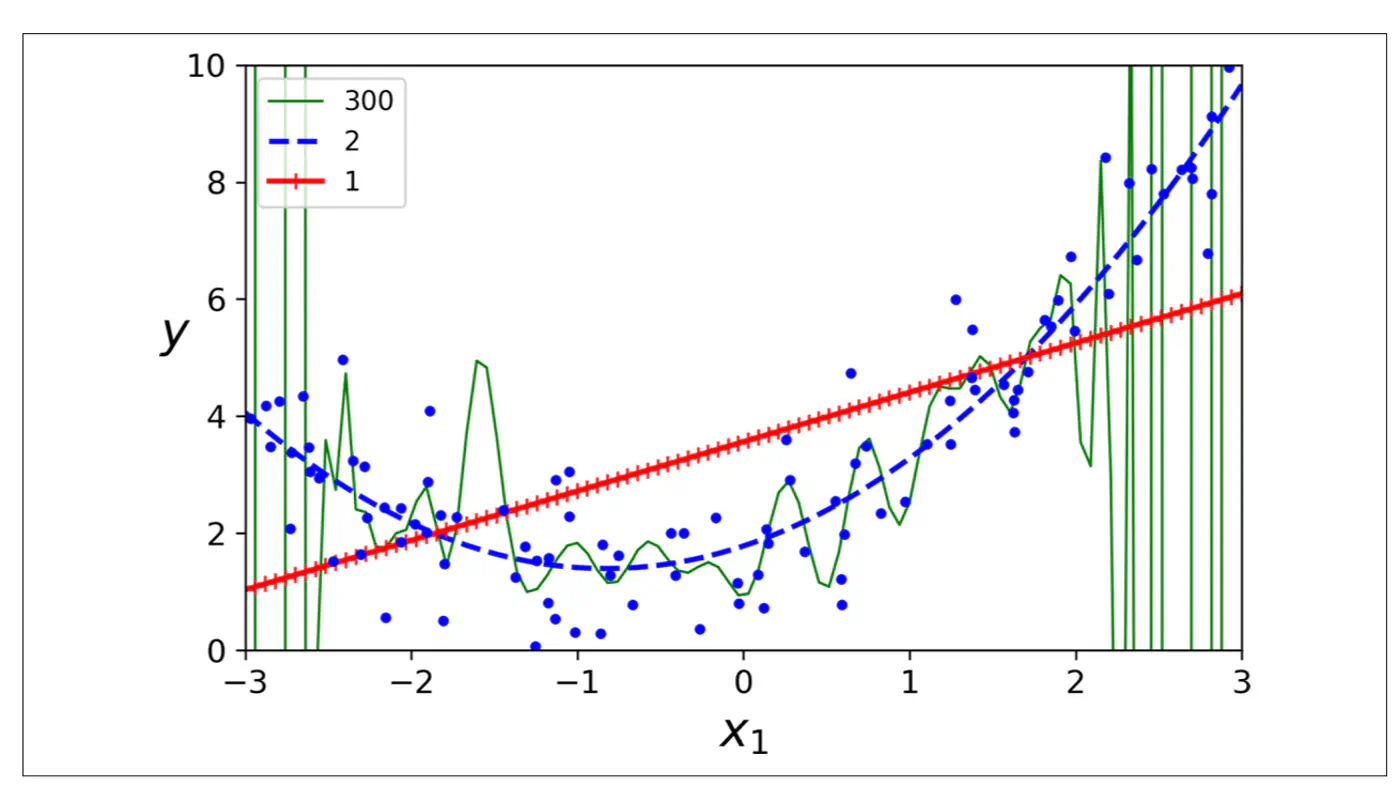

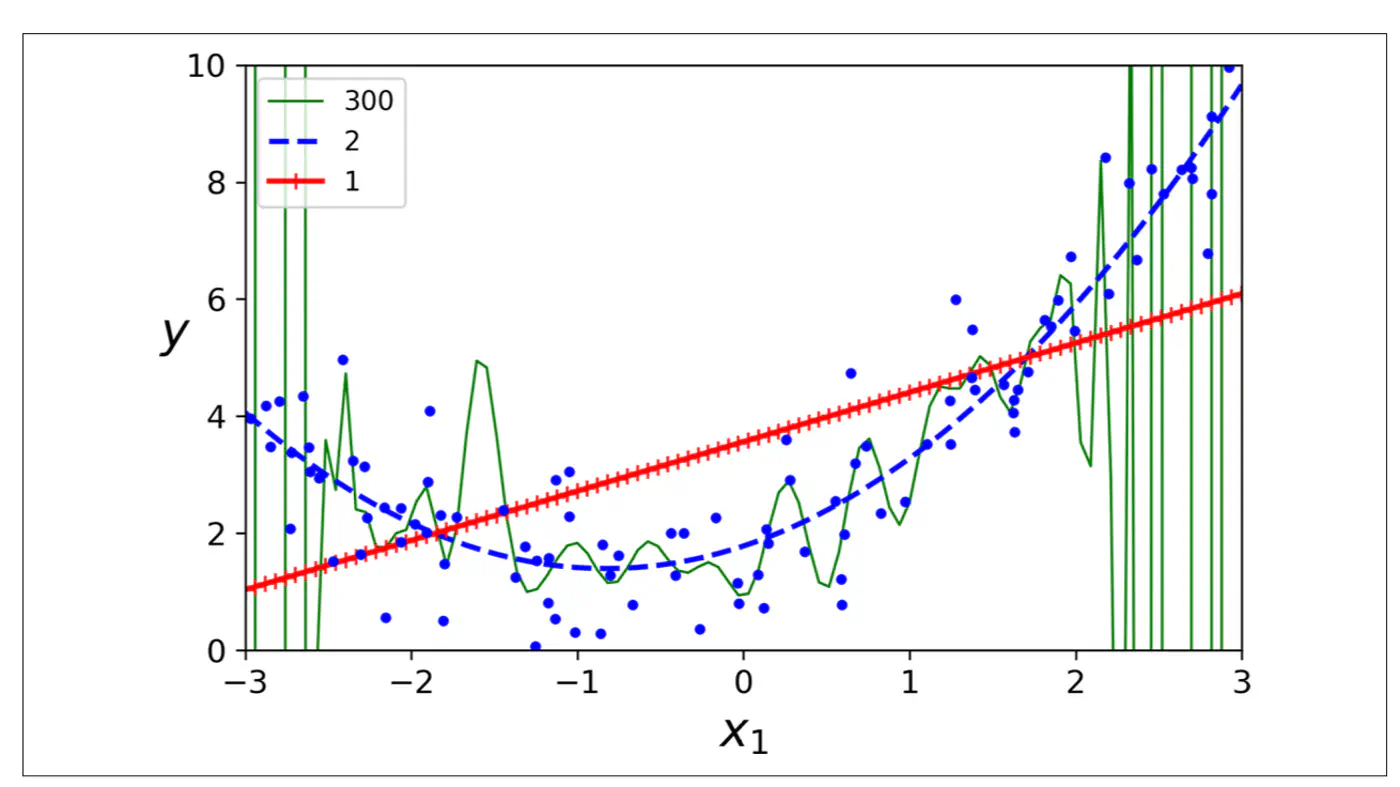

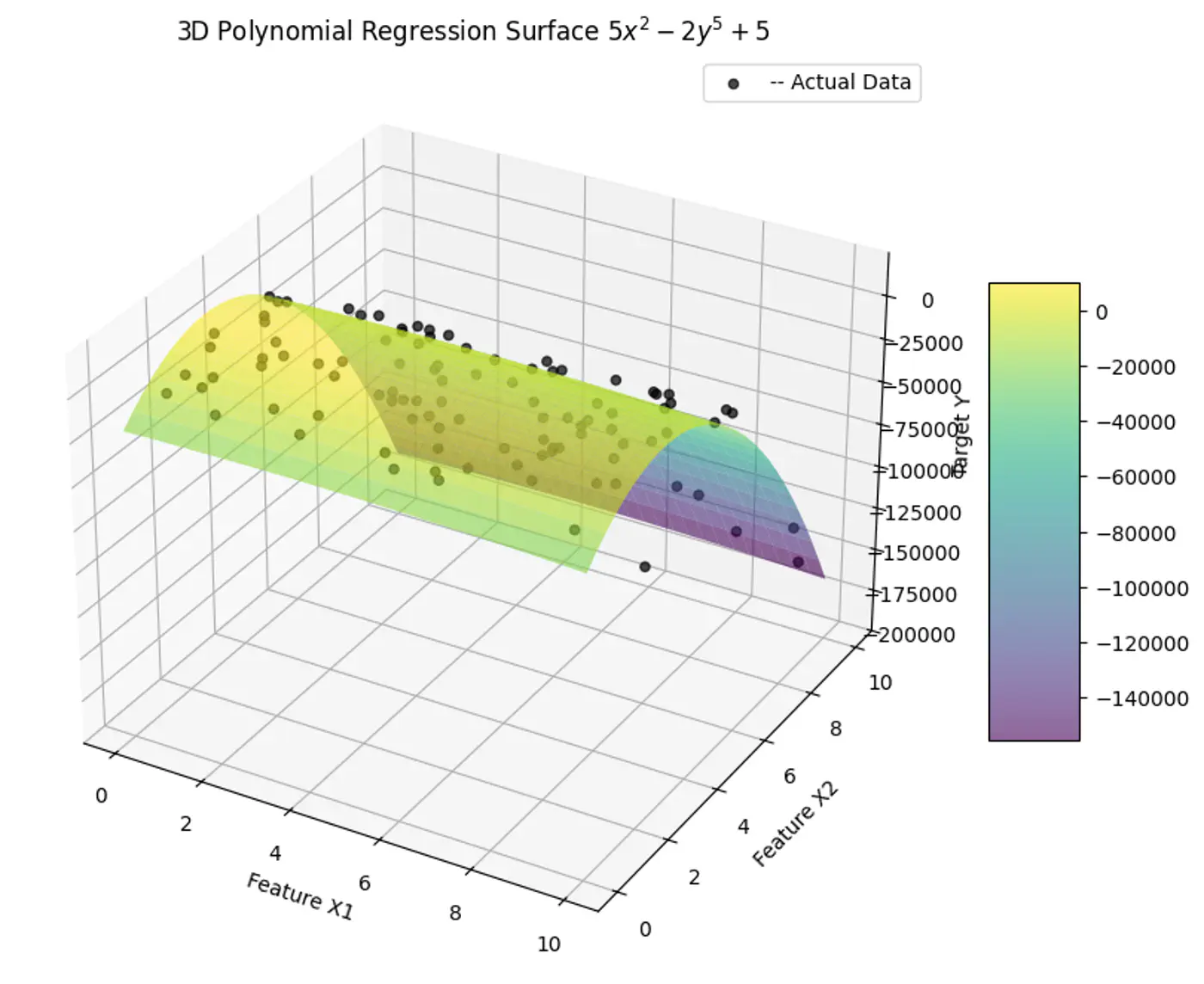

Here, ‘y’ is expressed as a linear combination of parameters - \( w_0, w_1, w_2, \dots, w_n \) Hence - Linear means the model is ‘linear’ with respect to its parameters NOT the variables. Read more about Hyperplane

where, \(x_3 = x_1^2 ~ and ~ x_4 = x_2^3 \) \(x_3 ~ and ~ x_4 \) are just 2 new (polynomial) variables. And, ‘y’ is still a linear combination of parameters: \(w_0, w_1, \dots w_4\)

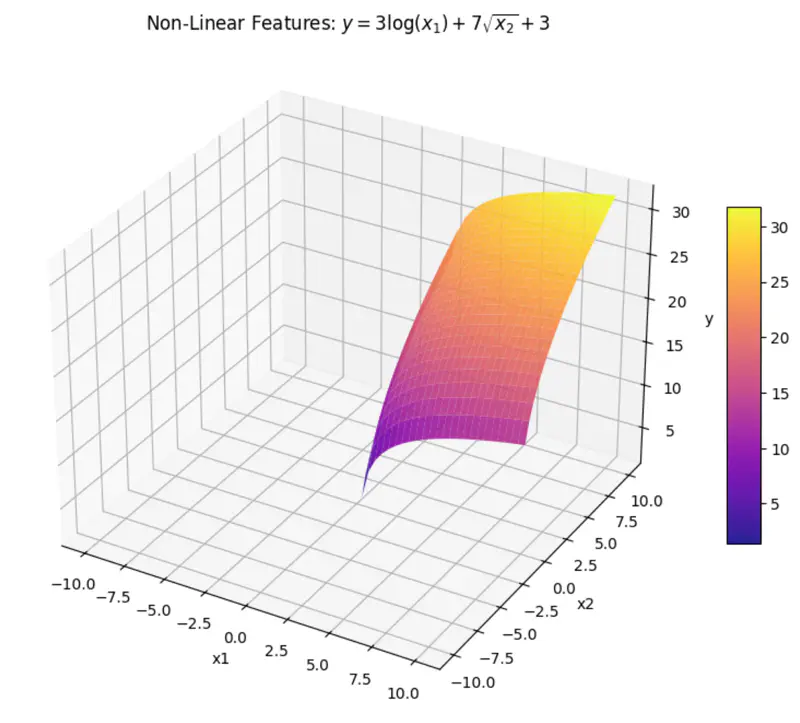

Non-Linear Features ✅

\[ y = w_1log(x) + w_2\sqrt{x}+ w_0 \]

can be rewritten as:

\[y = w_1x_1 + w_2x_2 + w_0\]

where, \(x_1 = log(x) ~ and ~ x_2 = \sqrt{x} \) \(x_1 ~ and ~ x_2 \) are are transformations of variable \(x\). And, ‘y’ is still a linear combination of parameters: \(w_0, w_1, ~and~ w_2\)

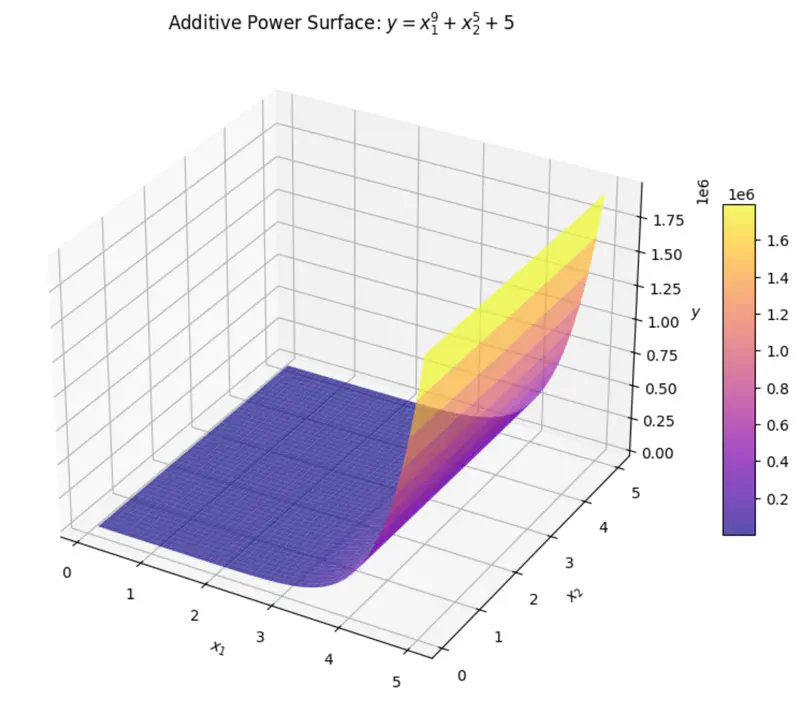

Non-Linear Parameters ❌

\[ y = x_1^{w_1} + x_2^{w_2} + w_0 \]

Even if we take log, we get:

\[log(y) = w_1log(x_1) + w_2log(x_2) + log(w_0)\]

here, \(log(w_0) \) parameter is NOT linear.

Importance of Linearity

Linearity in parameters allows to use Ordinary Least Squares (OLS) to find the best-fit coefficients by solving

a set of linear equations, making estimation straightforward.

What is the meaning of “Regression” in Linear Regression ?

Regression = Going Back

Regression has a very specific historical origin that is different from its current statistical meaning.

Sir Francis Galton (19th century), cousin of Charles Darwin, coined 🪙 this term.

Observation: Galton observed that - the children 👶 of unusually tall ⬆️ parents 🧑🧑🧒🧒,

tended to be shorter ⬇️ than their parents 🧑🧑🧒🧒, and children 👶 of unusually short ⬇️ parents 🧑🧑🧒🧒,

tended to be taller ⬆️ than their parents 🧑🧑🧒🧒.

Galton named this biological tendency - ‘regression towards mediocrity/mean’.

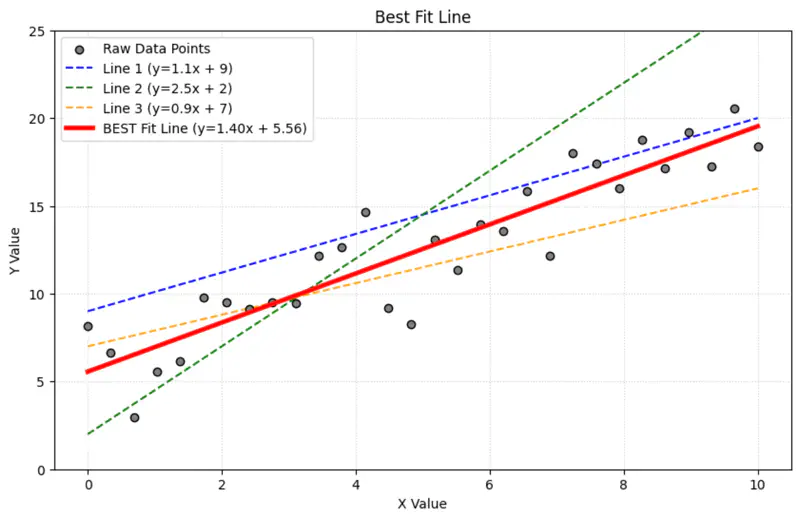

Galton used method of least squares to model this relationship, by fitting a line to the data 📊.

Regression = Fitting a Line Over time ⏳, the name ‘regression’ got permanently attached to the method of fitting line to the data 📊.

Today in statistics and machine learning, ‘regression’universally refers to the method of finding the ‘line of best fit’ for a set of data points, NOT the concept of ‘regressing towards the mean’.

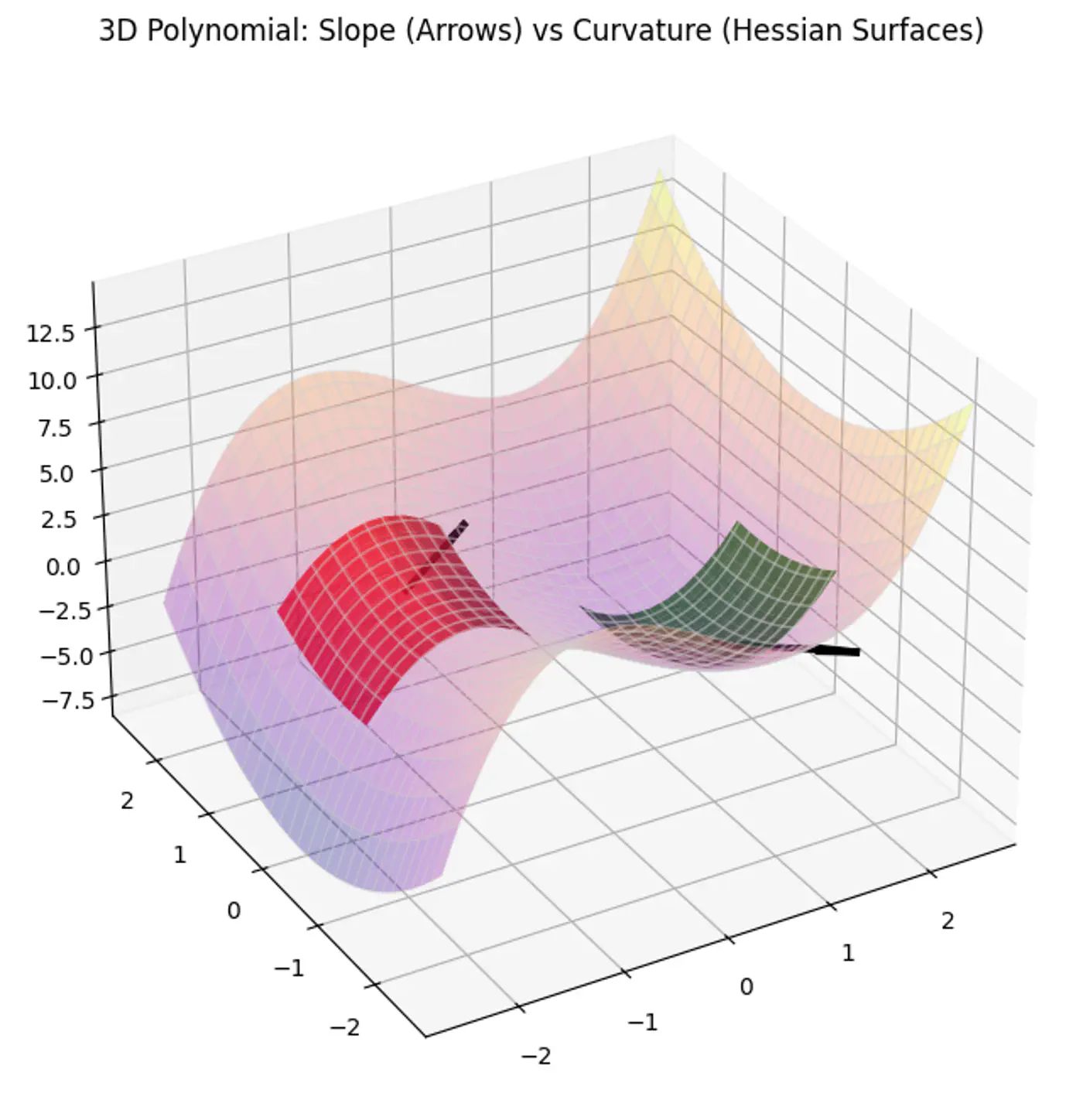

Note: \(\frac{\partial{(a^T\mathbf{x})}}{\partial{\mathbf{x}}} = a\) and

\(\frac{\partial{(\mathbf{x}^TA\mathbf{x})}}{\partial{\mathbf{x}}} = (A + A^T)\mathbf{x}\)

This is the closed-form solution of normal equations.

Issues with Normal Equation

Inverse may NOT exist (non-invertible).

Time complexity of calculating the inverse is O(n^3).

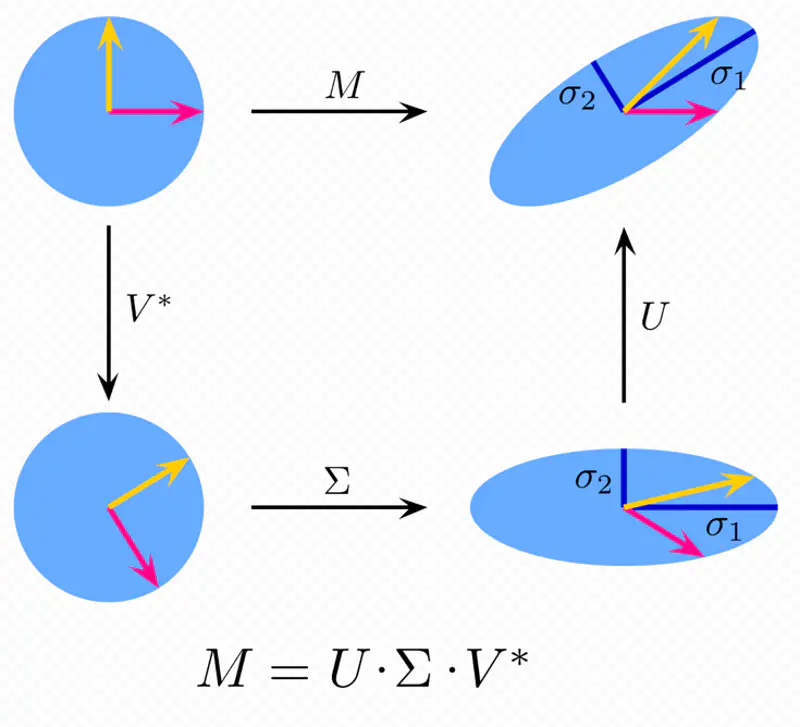

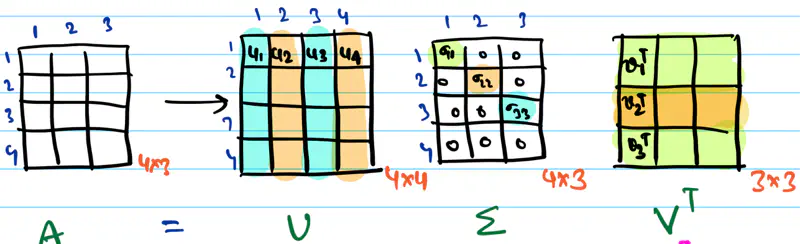

Pseudo Inverse

If the inverse does NOT exist then we can use the approximation of the inverse, also called Pseudo Inverse

or Moore Penrose Inverse (\(A^+\)).

Moore Penrose Inverse ( \(A^+\)) is calculated using Singular Value Decomposition (SVD).

SVD of \(A = U \Sigma V^T\)

Pseudo Inverse \(A^+ = V \Sigma^+ U^T\)

Where, \(\Sigma^+\) is a transpose of \(\Sigma\) with reciprocals of non-zero singular values on its diagonals. e.g:

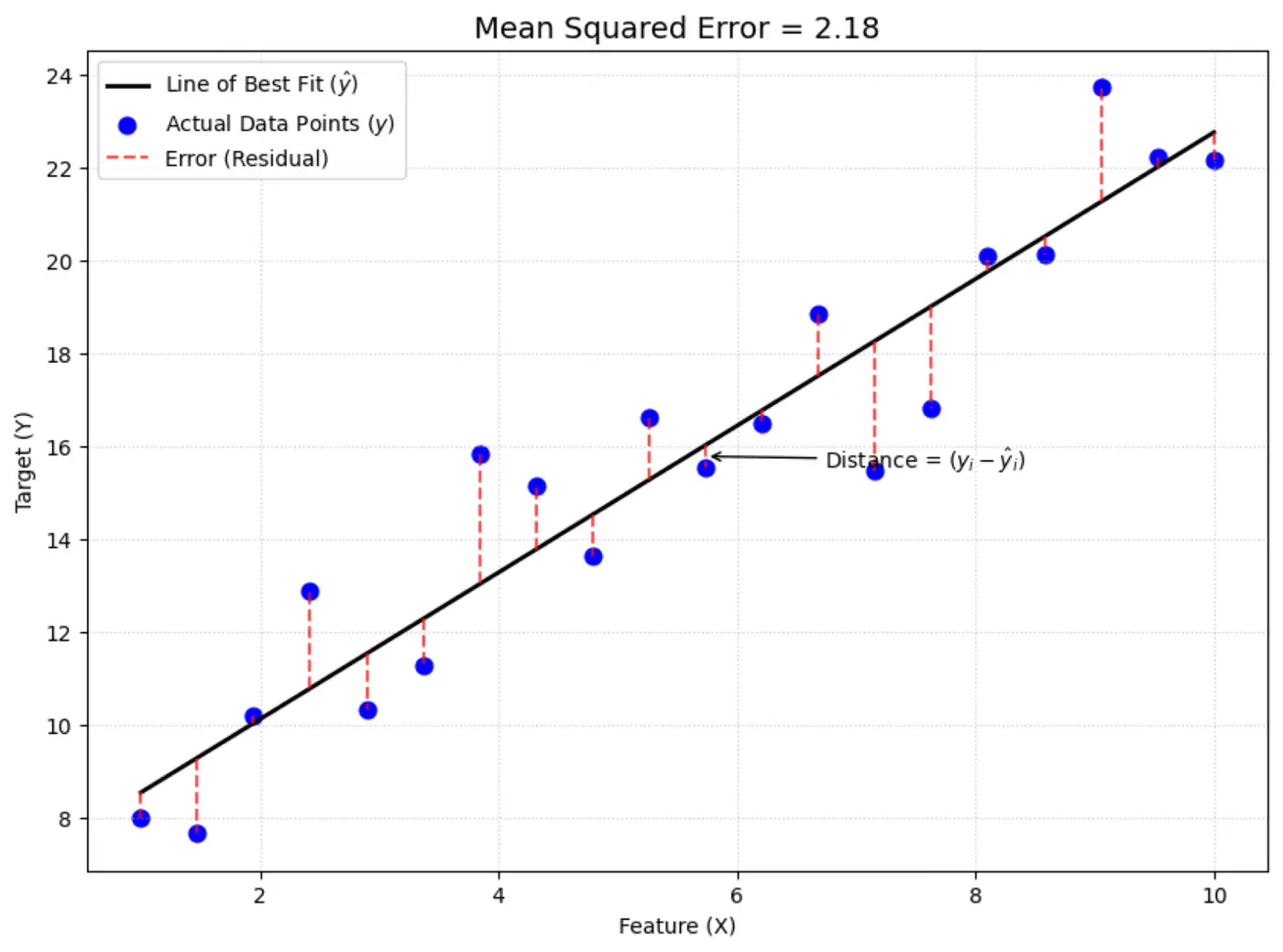

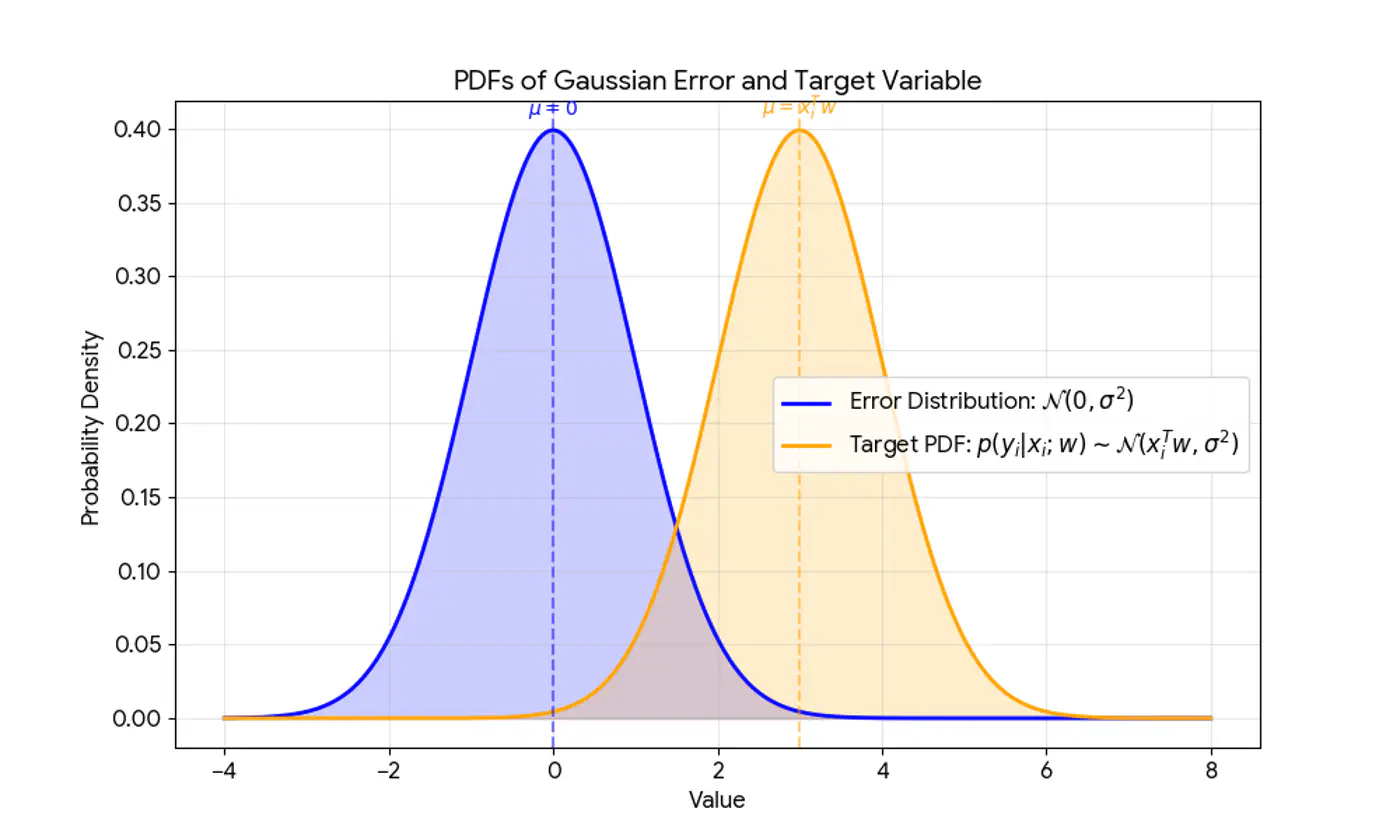

Actual value(\(y_i\)) = Deterministic linear predictor(\(x_i^Tw\)) + Error term(\(\epsilon_i\))

Error Assumptions

Independent and Identically Distributed (I.I.D): Each error term is independent of others.

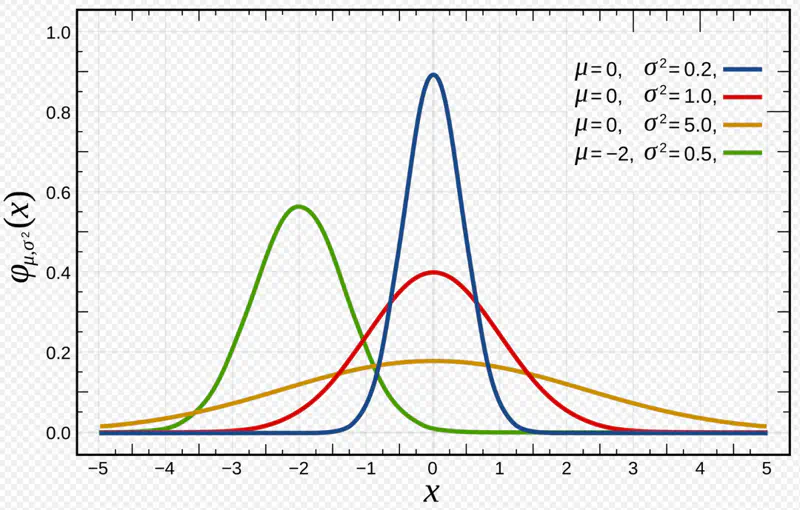

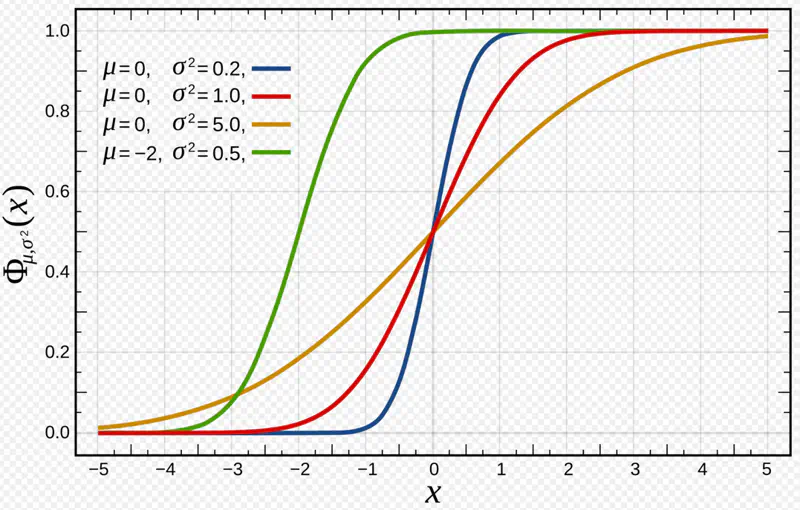

Normal (Gaussian) Distributed: Error follows a normal distribution with mean = 0 and a constant variance, .

This implies that the target variable itself is a random variable, normally distributed around the linear relationship.

\[(y_{i}|x_{i};w)∼N(x_{i}^{T}w,\sigma^{2})\]

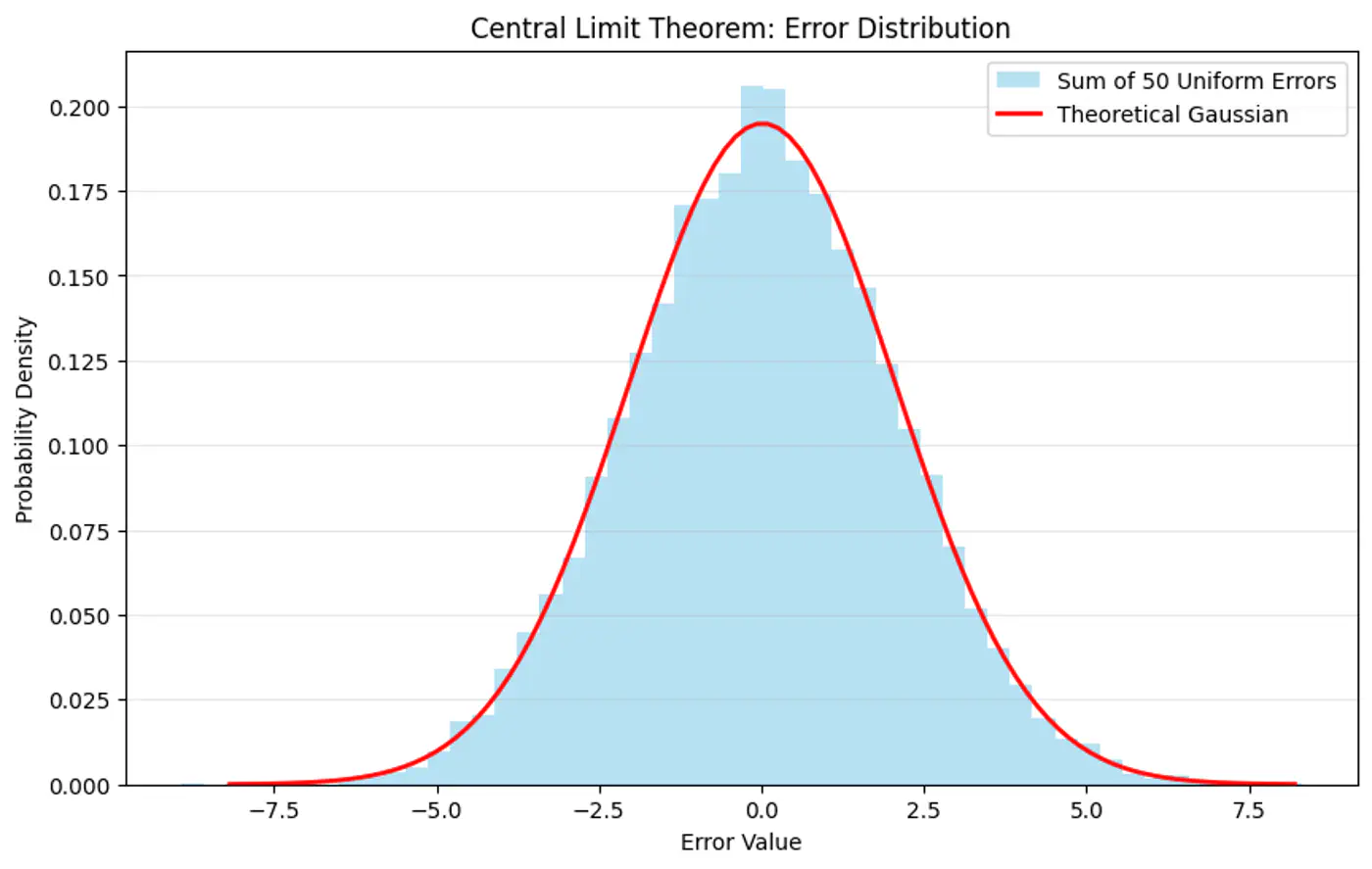

Why is Error terms distribution considered to be Gaussian ?

Central Limit Theorem (CLT) states that for a sequence of I.I.D random variables,

the distribution of the sample mean(sum) approximates to a normal distribution,

regardless of the original population distribution.

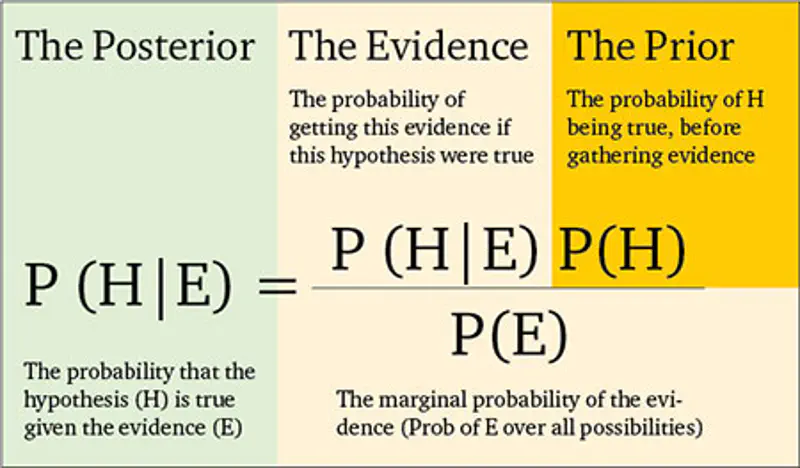

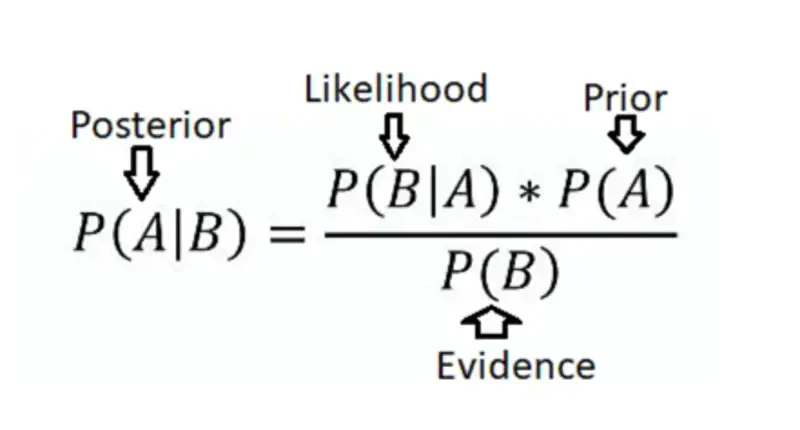

Probability Vs Likelihood

Probability (Forward View): Quantifies the chance of observing a specific outcome given a known, fixed model.

Likelihood (Backward/Inverse View): Inverse concept used for inference (working backward from results to causes). It is a function of the parameters and measures how ‘likely’ a specific set of parameters makes the observed data appear.

Maximum Likelihood Estimate (MLE)

‘Find the most plausible explanation for what I see.'

The goal of the probabilistic interpretation is to find the parameters ‘w’ that maximize the probability (likelihood) of observing the given dataset.

Maximizing the log-likelihood is equivalent to minimizing the sum of squared errors, which is the exact

objective of the ordinary least squares (OLS) method.

Note: The 1/2 term is included simply to make the derivative cleaner (it cancels out the 2 from the square).

Issues with Normal Equation

Normal Equation (Closed-form solution) jumps straight to the optimal point in one step.

\[w=(X^{T}X)^{-1}X^{T}y\]

But it is not always feasible and computationally expensive 💰(due to inverse calculation 🧮)

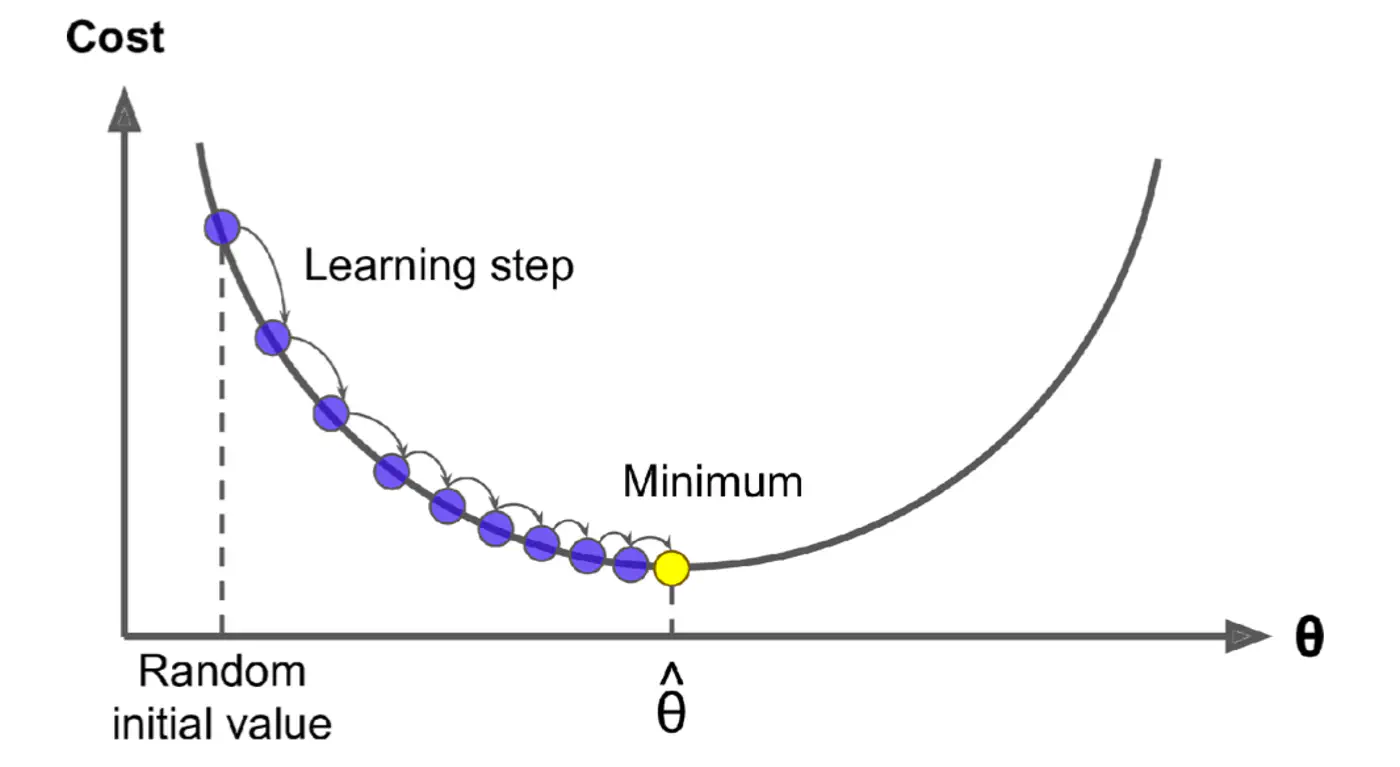

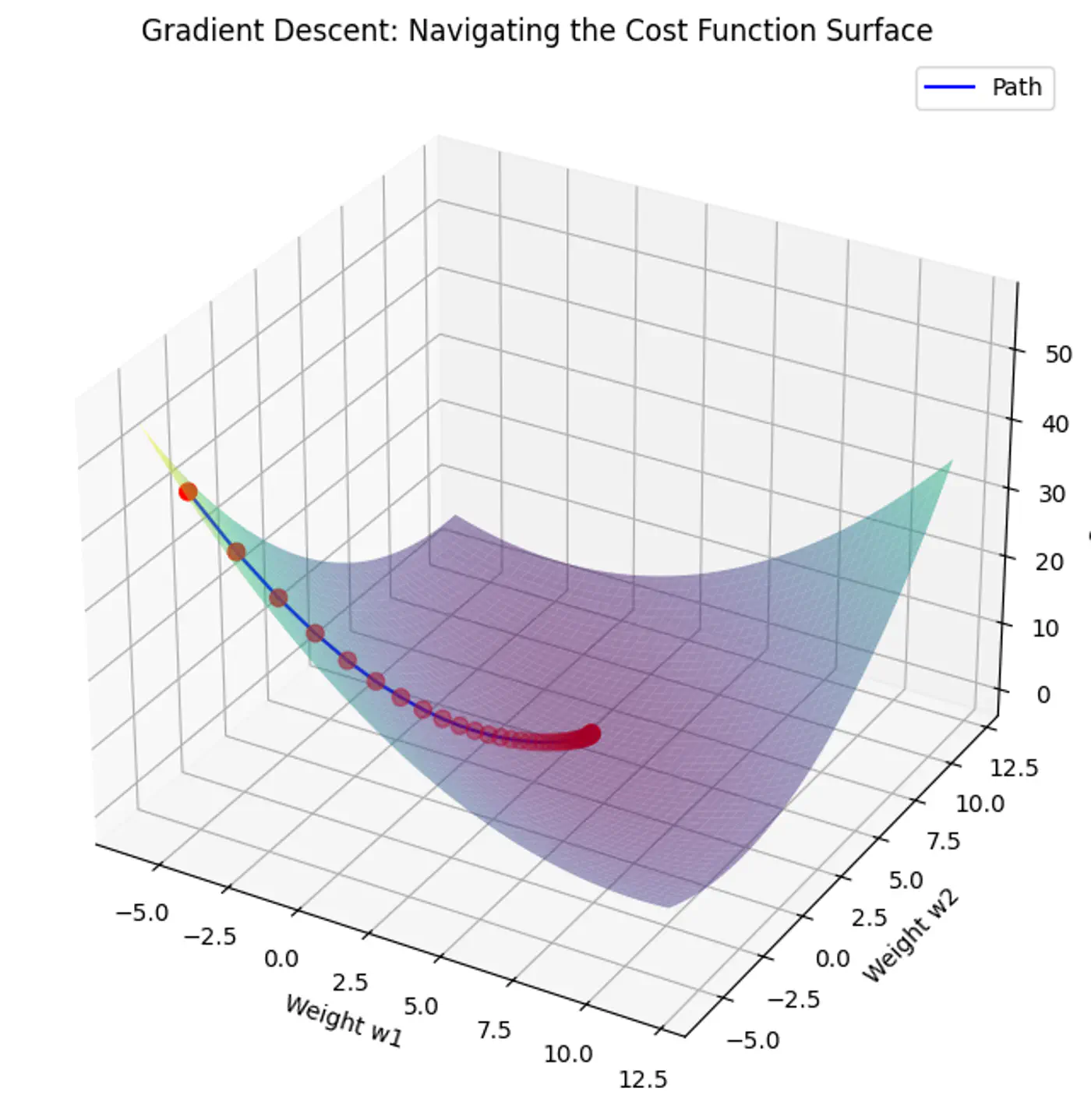

Gradient Descent 🎢

An iterative optimization algorithm slowly nudges parameters ‘w’ towards a value that minimize the cost💰 function.

Algorithm ⚙️

Initialize the weights/parameters with random values.

Calculate the gradient of the cost function at current parameter values.

Update the parameters using the gradient.

\[ w_{new} = w_{old} - \eta \frac{\partial{J(w)}}{\partial{w_{old}}} \]

\( \eta \) = learning rate or step size to take for each parameter update.

Repeat 🔁 steps 2 and 3 iteratively until convergence (to minima).

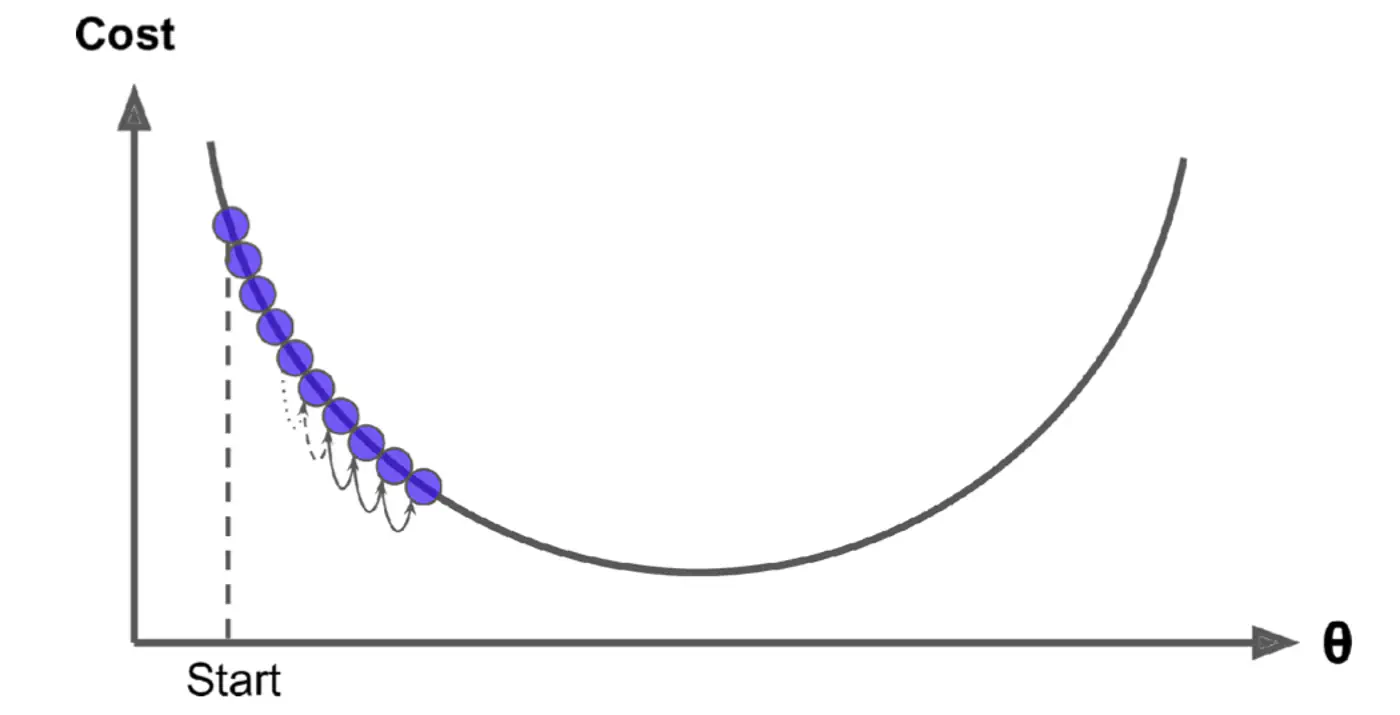

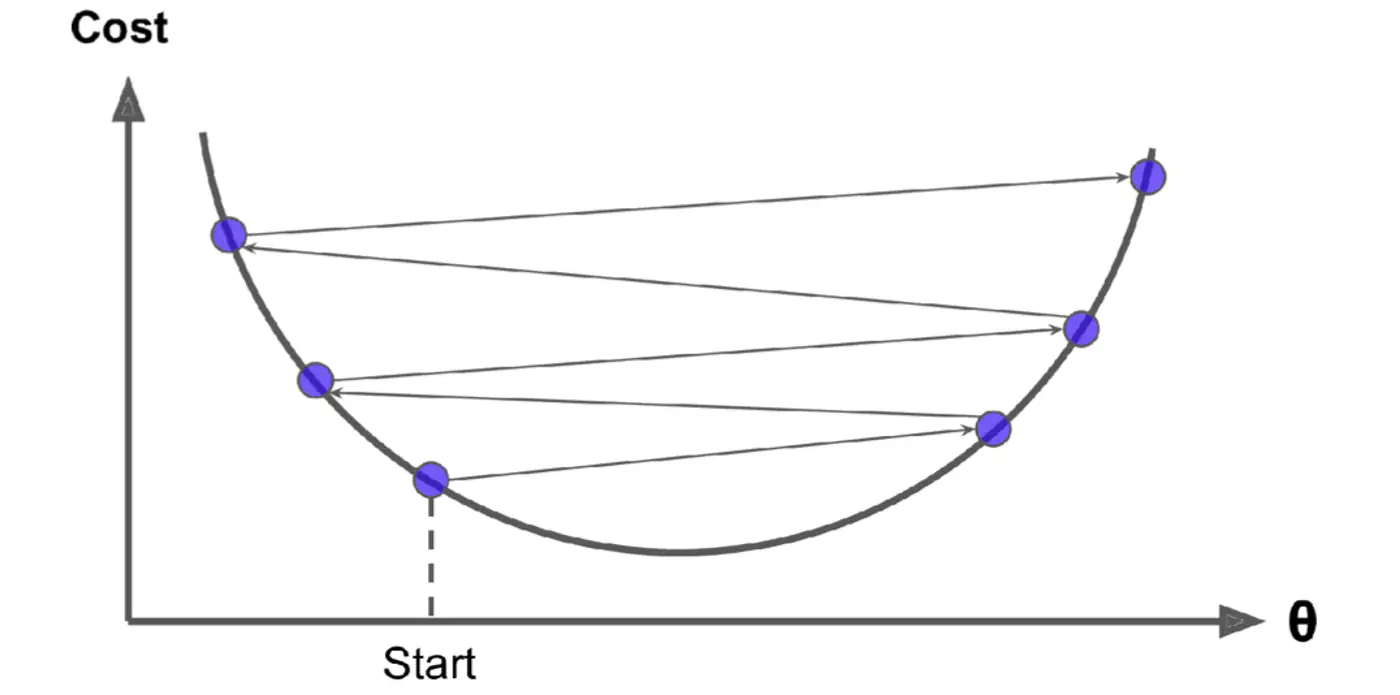

Most important hyper parameter of gradient descent.

Dictates the size of the steps taken down the cost function surface.

Small \(\eta\) ->

Large \(\eta\) ->

Learning Rate Techniques

Learning Rate Schedule: The learning rate is decayed (reduced) over time. Large steps initially and fine-tuning near the minimum, e.g., step decay or exponential decay.

Adaptive Learning Rate Methods: Automatically adjust the learning rate for each parameter ‘w’ based on the history of gradients. Preferred in modern deep learning as they require less manual tuning, e.g., Adagrad, RMSprop, and Adam.

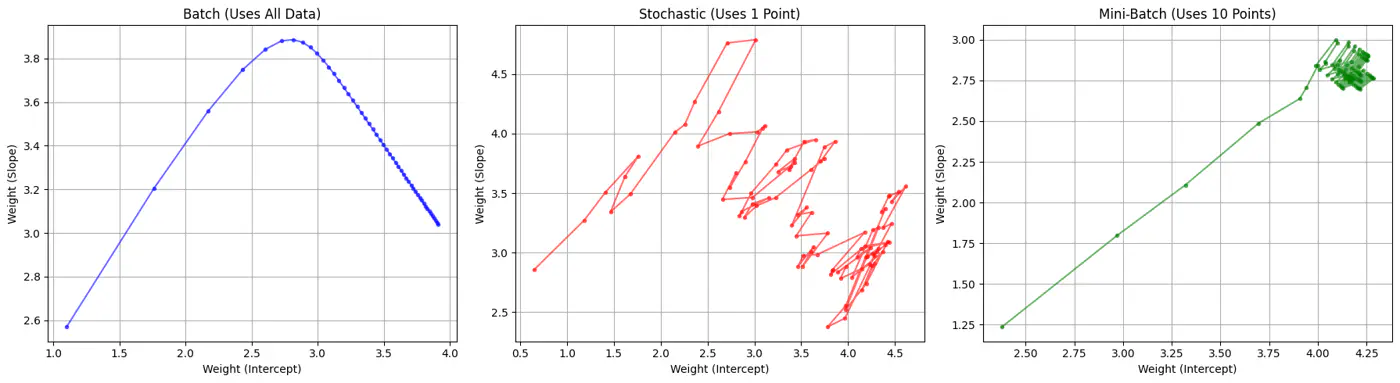

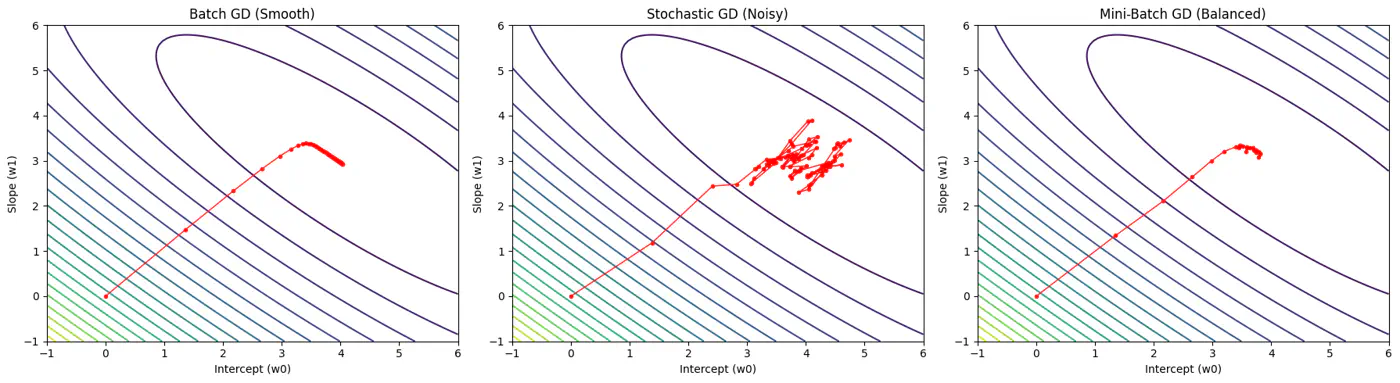

Batch, Stochastic, Mini-Batch are classified by data usage for gradient calculation in each iteration.

Batch Gradient Descent (BGD): Entire Dataset

Stochastic Gradient Descent (SGD): Random Point

Mini-Batch Gradient Descent (MBGD): Subset

Batch Gradient Descent 🎢 (BGD)

Computes the gradient using all the data points in the dataset for parameter update in each iteration.

\[w_{new} = w_{old} - \eta.\text{(average of all ’n’ gradients)}\]

🔑Key Points:

Slow 🐢 steps towards convergence, i.e, TC = O(n).

Smooth, direct path towards minima.

Minimum number of steps/iterations.

Not suitable for large datasets; impractical for Deep Learning, as n = millions/billions.

Stochastic Gradient Descent 🎢 (SGD)

Uses only 1 data point selected randomly from dataset to compute gradient for parameter update in each iteration.

\[w_{new} = w_{old} - \eta.\text{(gradient at any random data point)}\]

🔑Key Points:

Computationally fastest 🐇 per step; TC = O(1).

Highly noisy, zig-zag path to minima.

High variance in gradient estimation makes path to minima volatile, requiring a careful decay of learning rate to ensure convergence to minima.

Mini Batch Gradient Descent 🎢 (MBGD)

Uses small randomly selected subsets of dataset, called mini-batch, (1<k<n), to compute gradient for parameter update in each iteration.

\[w_{new} = w_{old} - \eta.\text{(average gradient of ‘k' data points)}\]

🔑Key Points:

Moderate time ⏰ consumption per step; TC = O(k<n).

Less noisy, and more reliable convergence than stochastic gradient descent.

More efficient and faster than batch gradient descent.

Standard optimization algorithm for Deep Learning.Note: Vectorization on GPUs allows for parallel processing of mini-batches; also GPUs are the reason for the mini-batch size to be a power of 2.

Test Data: Evaluate model performance (Real (final) exam)

Data Leakage

Data leakage occurs when information from the validation or test set is inadvertently used to

train 🏃♂️ the model.

The model ‘cheats’ by learning to exploit information it should not have access to, resulting in artificially

inflated performance metrics during testing 🧪.

Typical Split Ratios

Small datasets(1K-100K): 60/20/20, 70/15/15 or 80/10/10

Large datasets(>1M): 98/1/1 would suffice, as 1% of 1M is still 10K.

Note: There is no fixed rule, its trial and error.

Imbalanced Data

Imbalanced data refers to a dataset where the target classes are represented by an unequal or

highly skewed distribution of samples, such that the majority class significantly outnumbers the minority class.

Stratified Sampling

If there is class imbalance in the dataset, (e.g., 95% class A , 5% class B), a random split might result in the

validation set having 99% class A.

Solution: Use stratified sampling to ensure class proportions are maintained across all splits

(train️/validation/test).

Note: Non-negotiable for imbalanced data.

Time-Series ⏳ Data

In time-series ⏰ data, divide the data chronologically, not randomly, i.e, training data time ⏰ should precede validation data time ⏰.

We always train 🏃♂️ on past data to predict future data.

Do not trust one split of the data; validate across many splits, and average the result to reduce randomness and bias.

Note: Two different splits of the same dataset can give very different validation scores.

Cross-validation

Cross-validation is a statistical resampling technique used to evaluate how well a machine learning model generalizes

to an independent, unseen dataset.

It works by systematically partitioning the available data into multiple subsets, or ‘folds’,

and then training and testing the model on different combinations of these folds.

K-Fold Cross-Validation

Leave-One-Out Cross-Validation (LOOCV)

K-Fold Cross-Validation

Shuffle the dataset randomly (except time-series ⏳).

Split data into k equal subsets(folds).

Iterate through each unique fold, using it as the validation set.

Use remaining k-1 fold for training 🏃♂️.

Take an average of the results.Note: Common choice for k=5 or 10.

Iteration 1: [V][T][T][T][T]

Iteration 2: [T][V][T][T][T]

Iteration 3: [T][T][V][T][T]

Iteration 4: [T][T][T][V][T]

Iteration 5: [T][T][T][T][V]

Leave-One-Out Cross-Validation (LOOCV)

Model is trained 🏃♂️on all data points except one, and then tested 🧪on that remaining single observation.

LOOCV is an extreme case of k-fold cross-validation, where, k=n (number of data points).

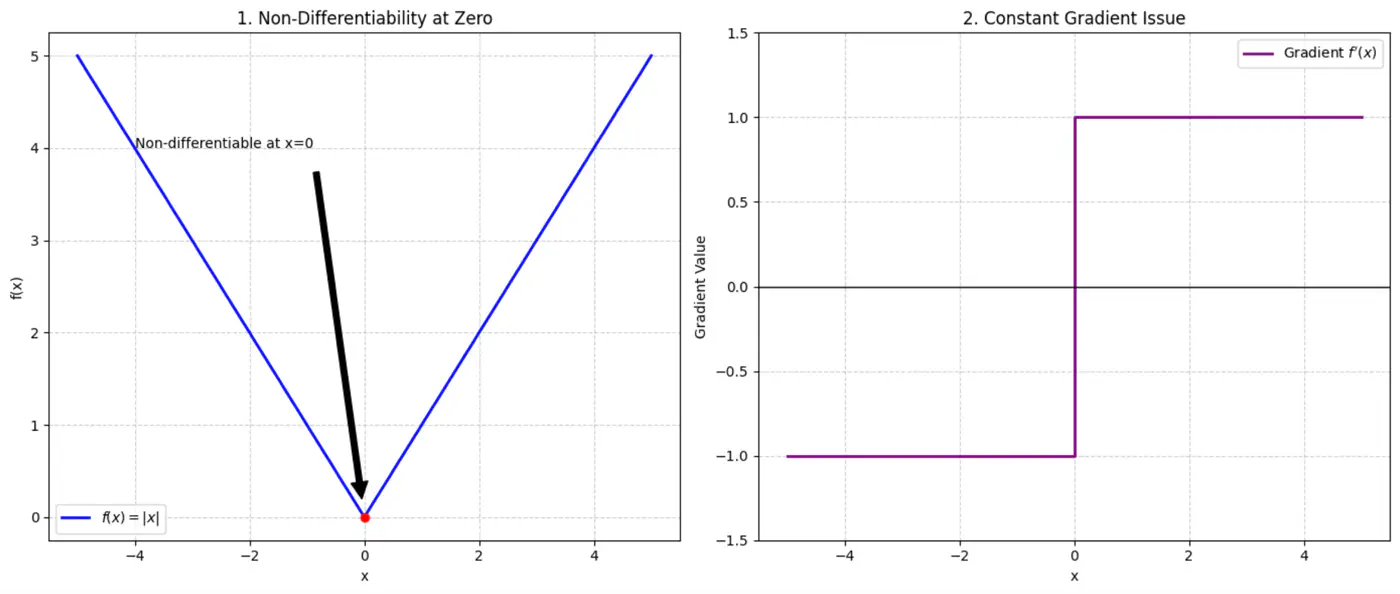

Note: Co-adaptation refers to a phenomenon where neurons in a neural network become highly dependent on each other to detect features, rather than learning independently.

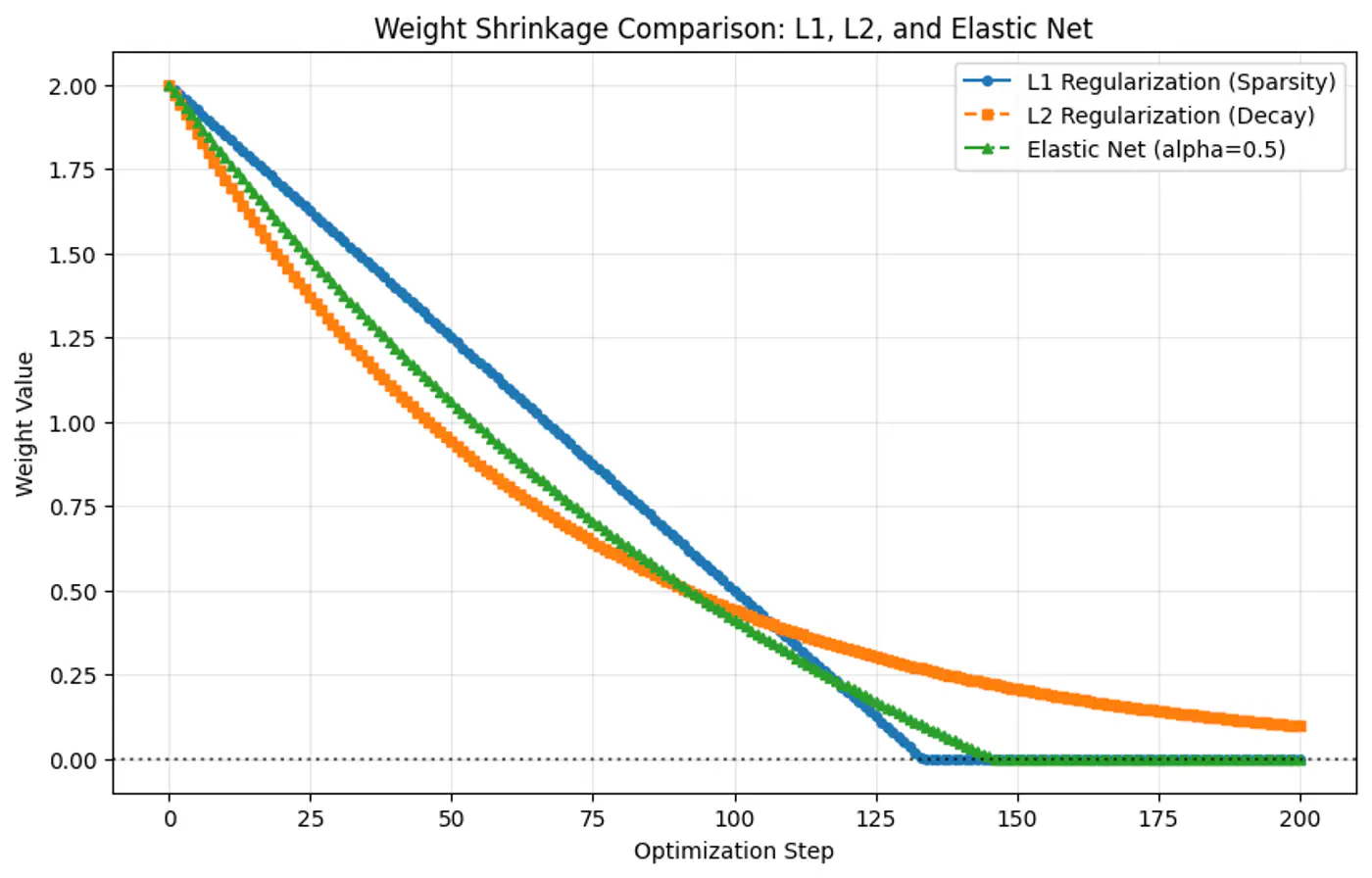

Shrinks some weights exactly to 0, effectively performing feature selection, giving sparse solutions.

For a group of highly co-related features, arbitrarily selects one feature and shrinks others to 0.

Use case: Best when using high-dimensional datasets (d»n) where we suspect many features are irrelevant or redundant, or when model interpretability matters.

Also known as Lasso (Least Absolute Shrinkage and Selection Operator) regression.

Computational hack: \(\frac{\partial{|w_j|}}{\partial{w_j}} = 0\), since absolute function is not differentiable at 0.

Sparsity(feature-selection) of L1 and stability/grouping effect of L2 regularization.

Use case: Best when we have high dimensional data with correlated features and we want sparse and stable solution.

L1/L2/Elastic Net Regularization Comparison

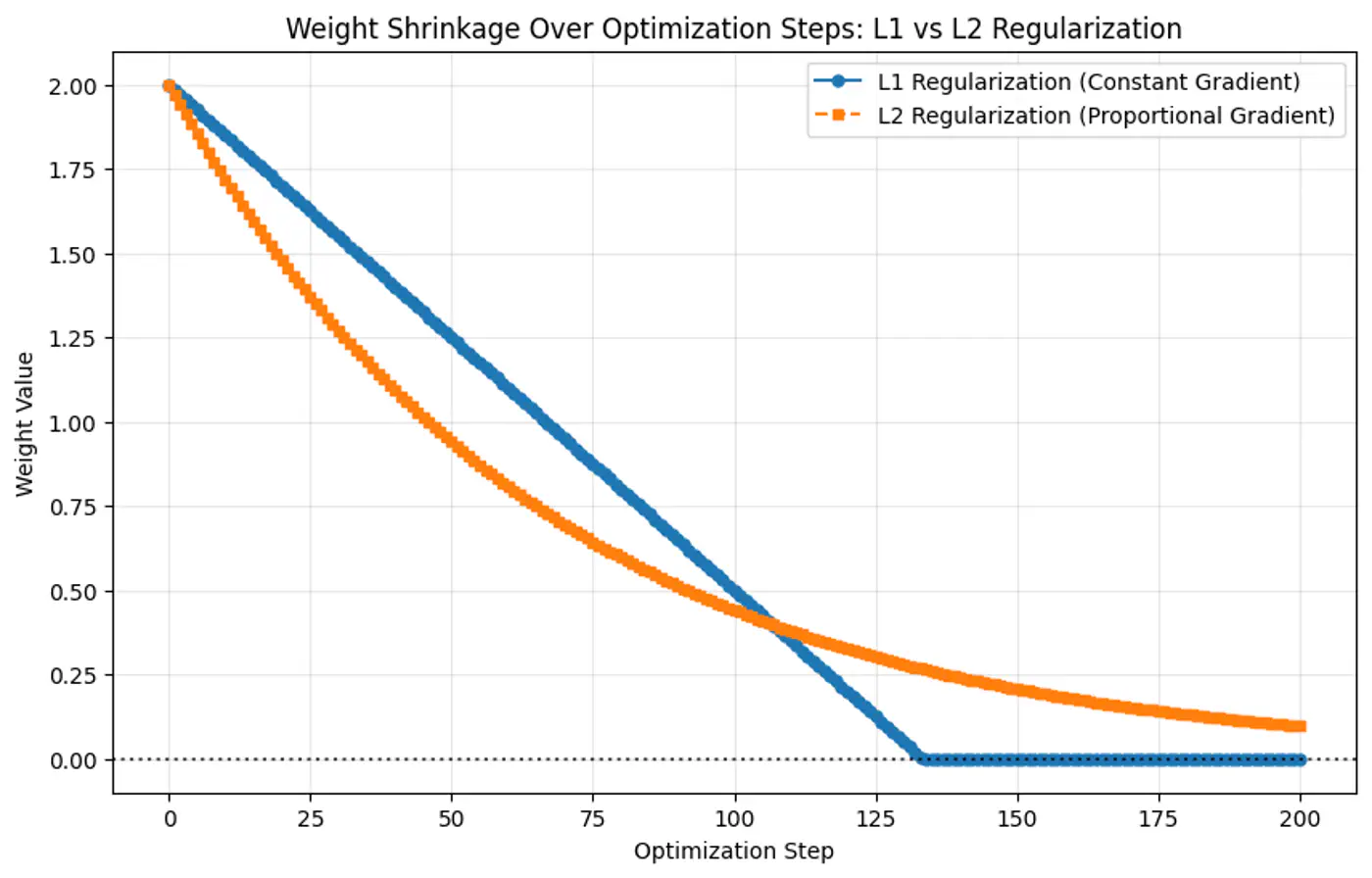

Why weights shrink exactly to 0 in L1 regularization but NOT in L2 regularization ?

Because the gradient of L1 penalty (absolute function) is a constant value, i.e, \(\pm 1\), this means a constant reduction in weight at each step, making it gradually reach to 0 in finite steps.

Whereas, the derivative of L2 penalty is proportional to the weight (\(2w_j\)) and as the weight reaches close to 0, the gradient also becomes very small, this means that the weight will become very close to 0, but not exactly equal to 0.

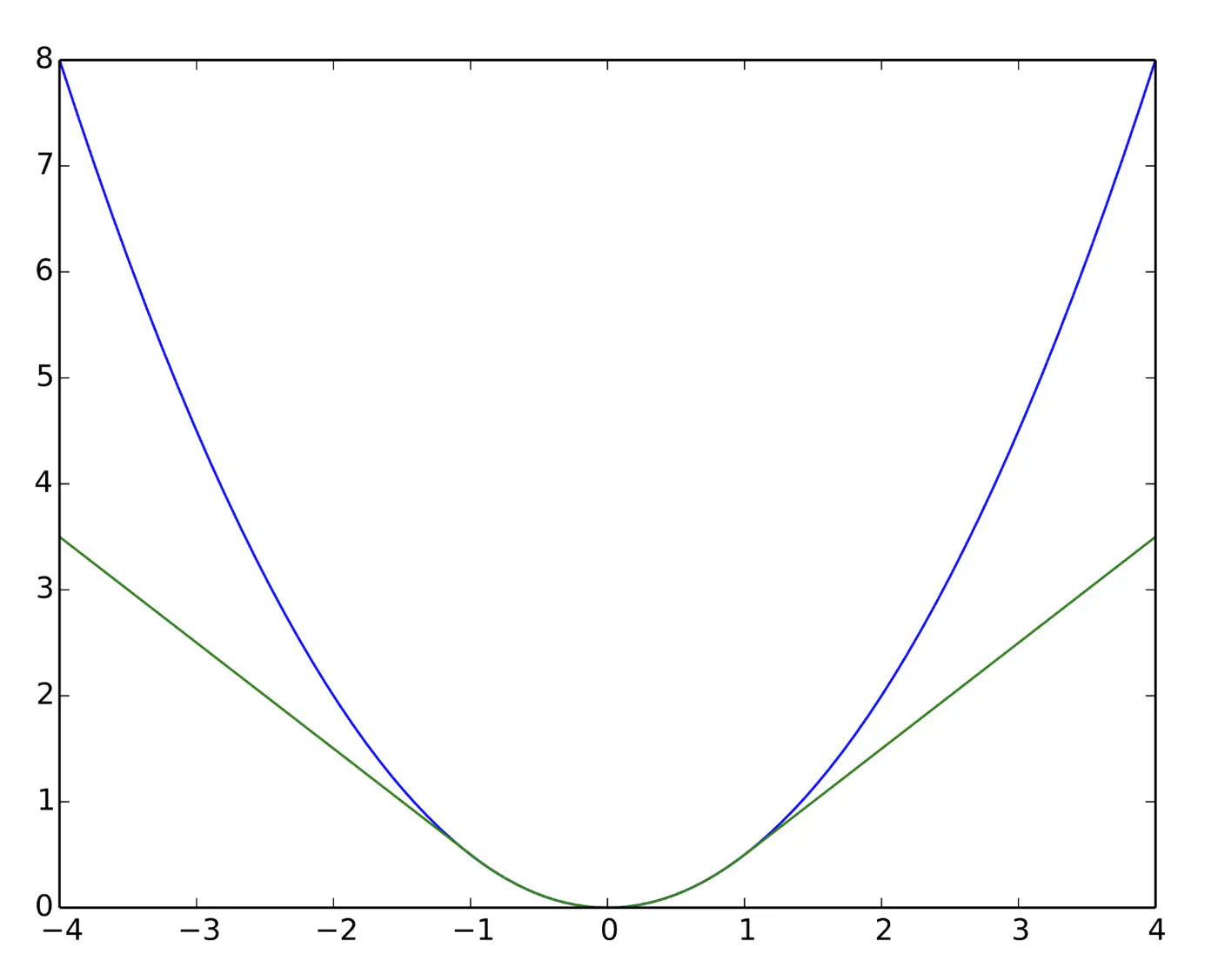

Differentiable at 0; smooth convergence to minima.

Delta (\(\delta\)) knob(hyper parameter) to control.

\(\delta\) high: MSE

\(\delta\) low: MAE

Note: Tune \(\delta\): MAE, for outliers > \(\delta\); MSE, for small errors < \(\delta\). e.g: = 95th percentile of errors or 1.35\(\sigma\) for standard Gaussian data.

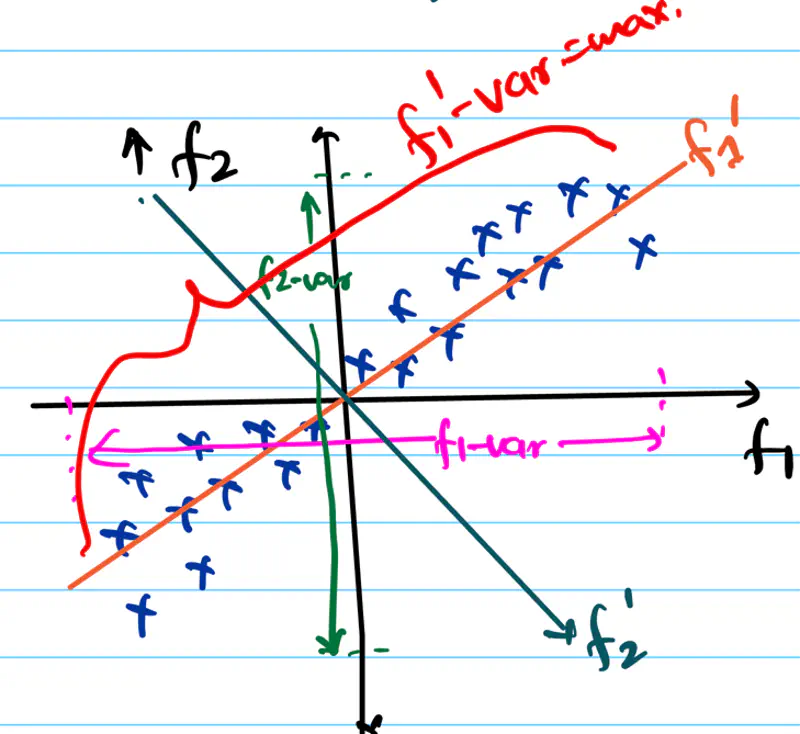

Linear Regression works reliably only when certain key 🔑 assumptions about the data are met.

Linearity

Independence of Errors (No Auto-Correlation)

Homoscedasticity (Equal Variance)

Normality of Errors

No Multicollinearity

No Endogeneity (Target not correlated with the error term)

Linearity

Relationship between features and target 🎯 is linear in parameters.

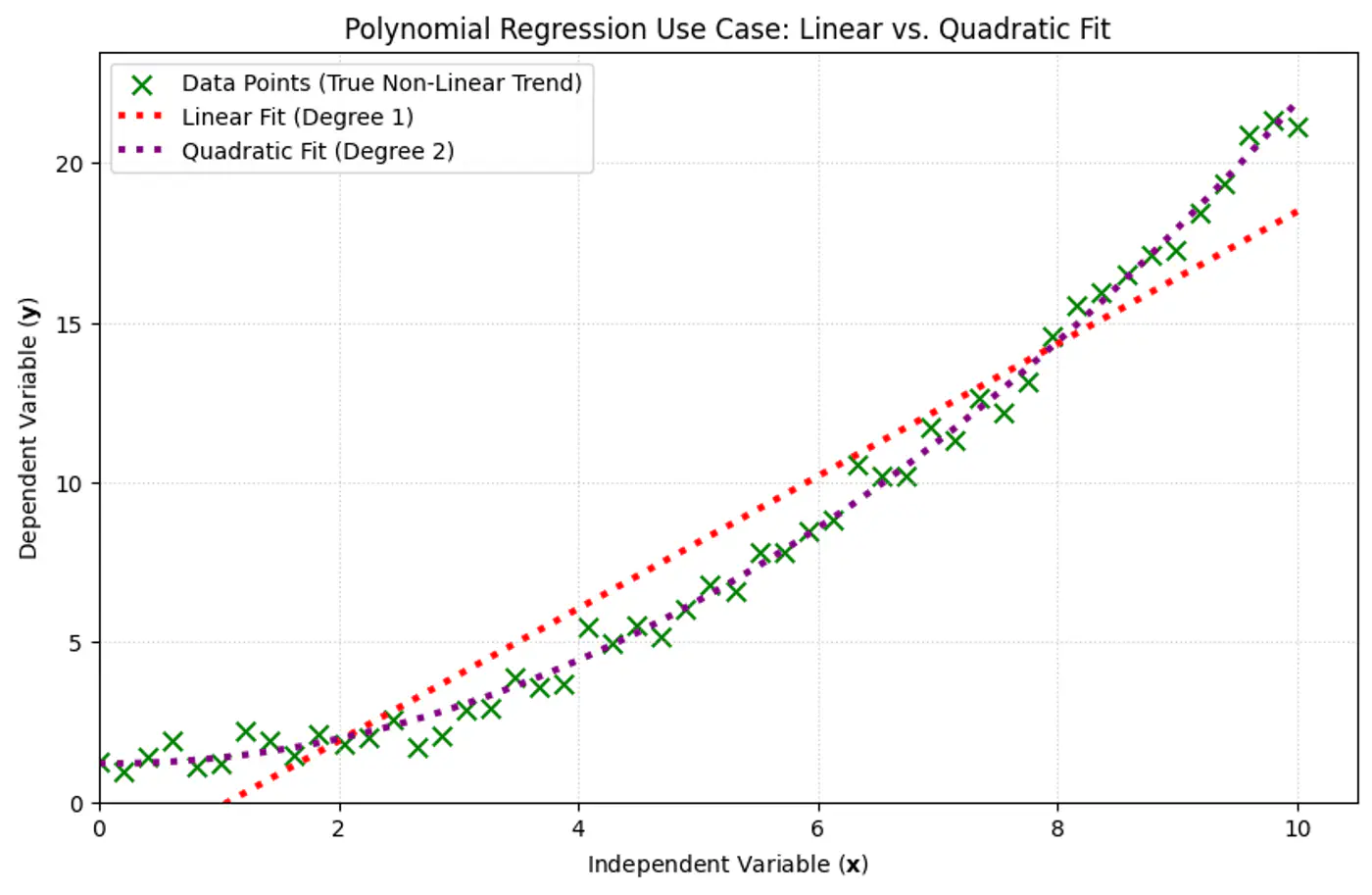

Note: Polynomial regression is linear regression. \(y=w_0 +w_1x_1+w_2x_2^2 + w_3x_3^3\)

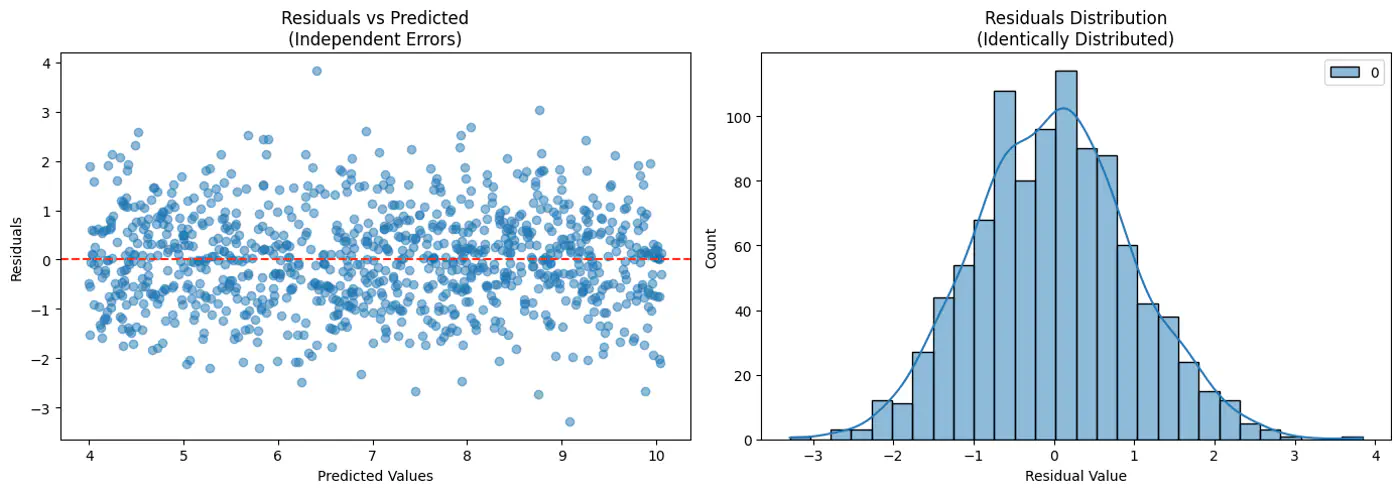

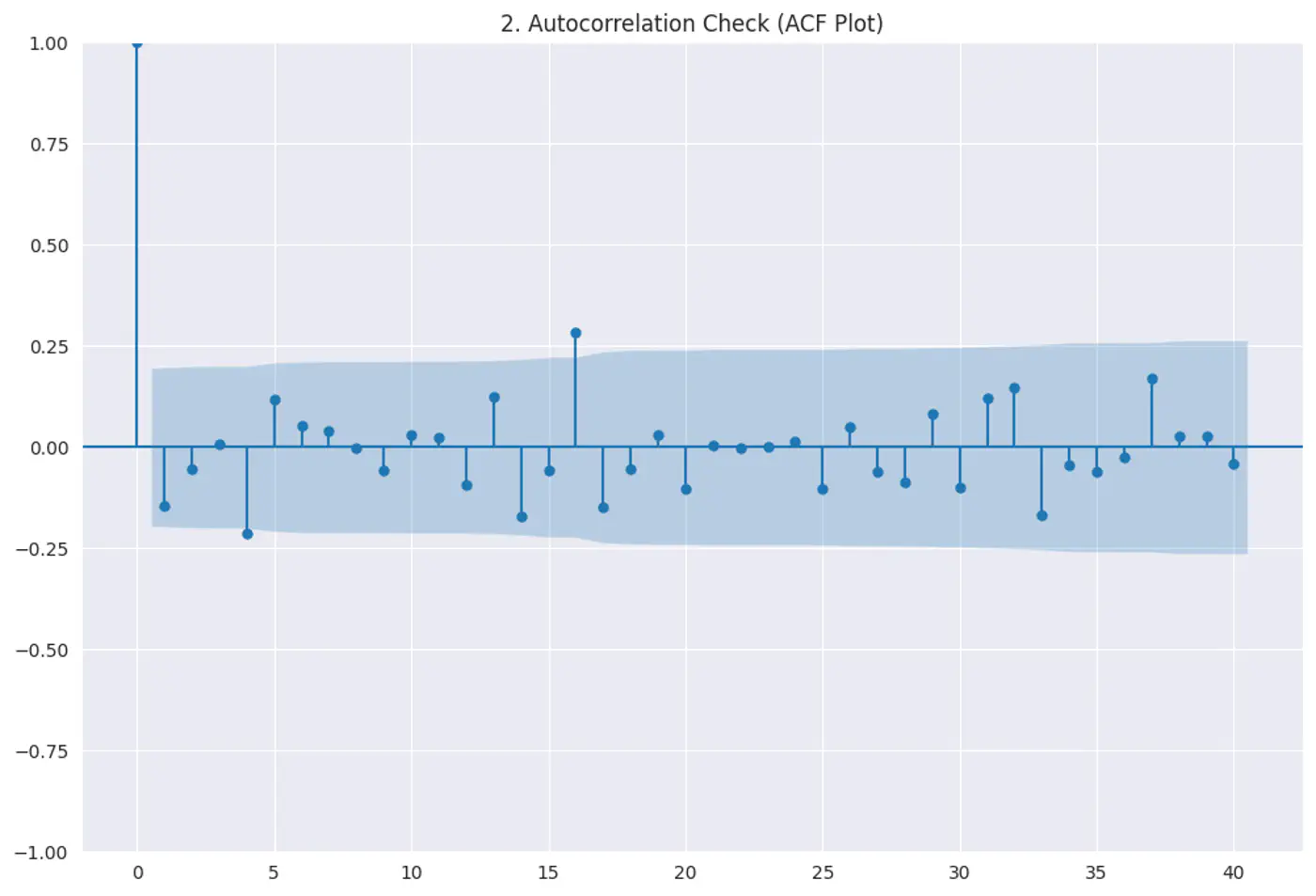

Independence of Errors (No Auto-Correlation)

Residuals (errors) should not have a visible pattern or correlation with one another (most common in time-series ⏰ data).

Risk: If errors are correlated, standard errors will be underestimated, making variables look ‘statistically significant’ when they are not.

Test:

Durbin–Watson test

Autocorrelation plots (ACF)

Residuals vs time

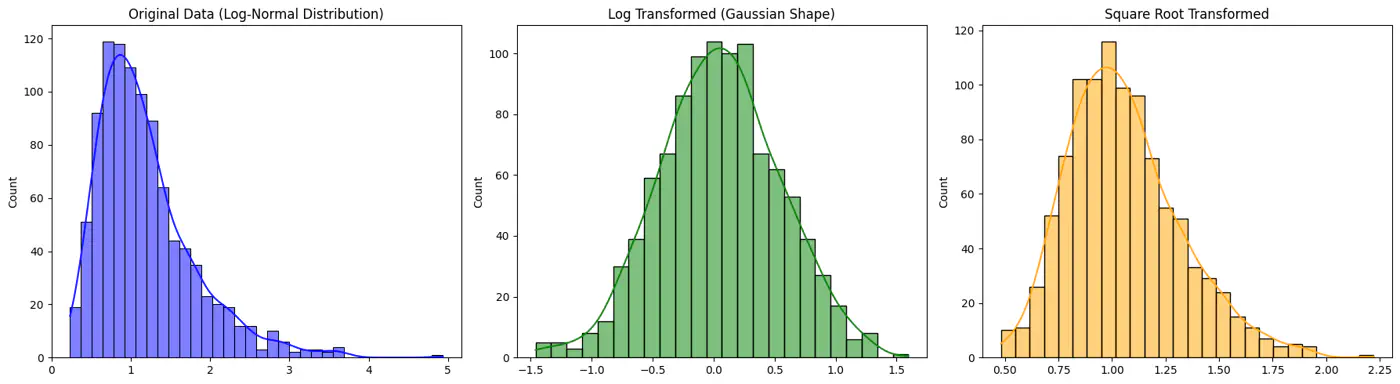

Homoscedasticity

Constant variance of errors; Var(ϵ|X)=σ

Risk: Standard errors become biased, leading to unreliable hypothesis tests (t-tests, F-tests).

Test:

Breusch–Pagan test

White test

Fix:

Log transform

Weighted Least Squares(WLS)

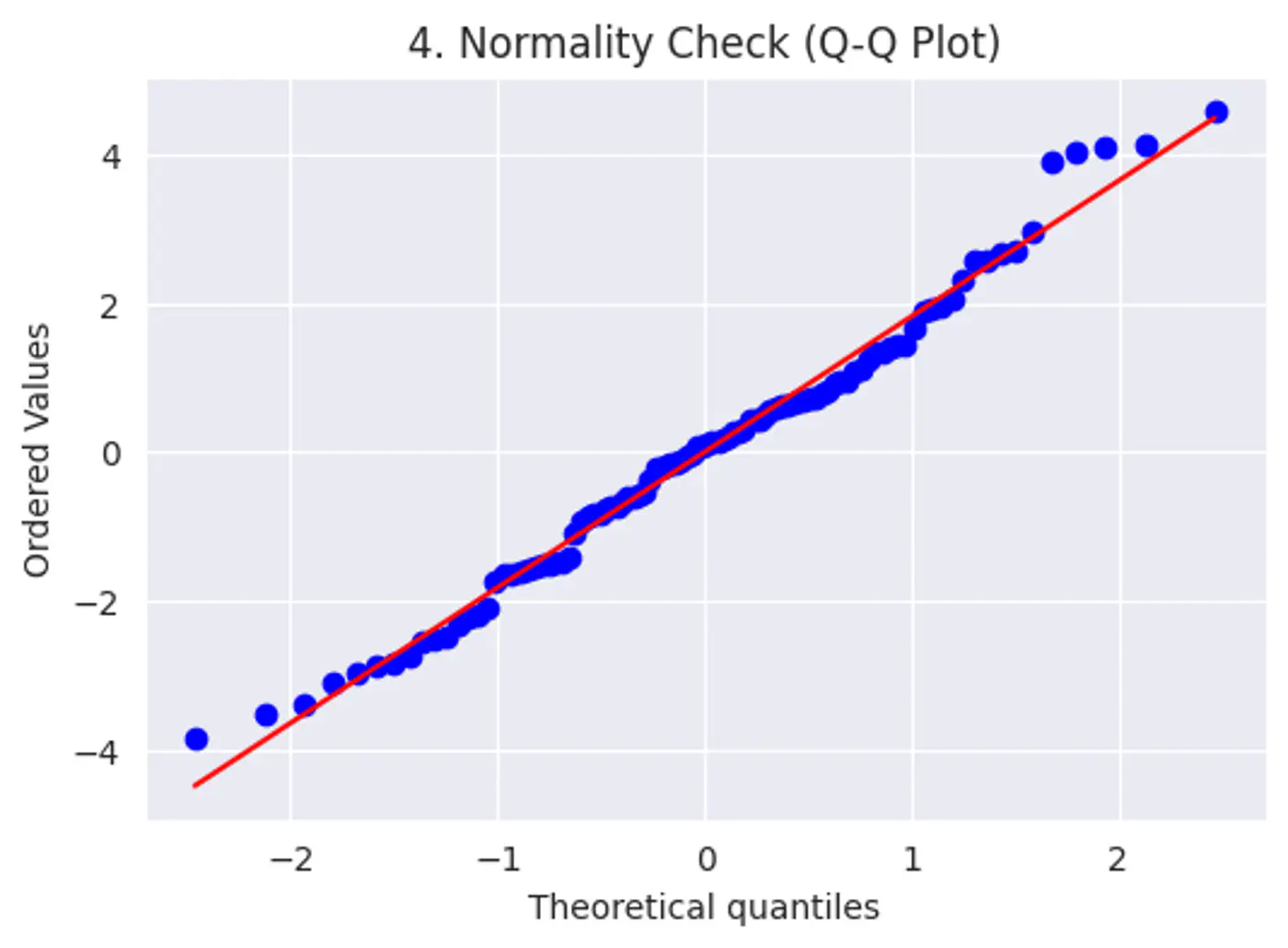

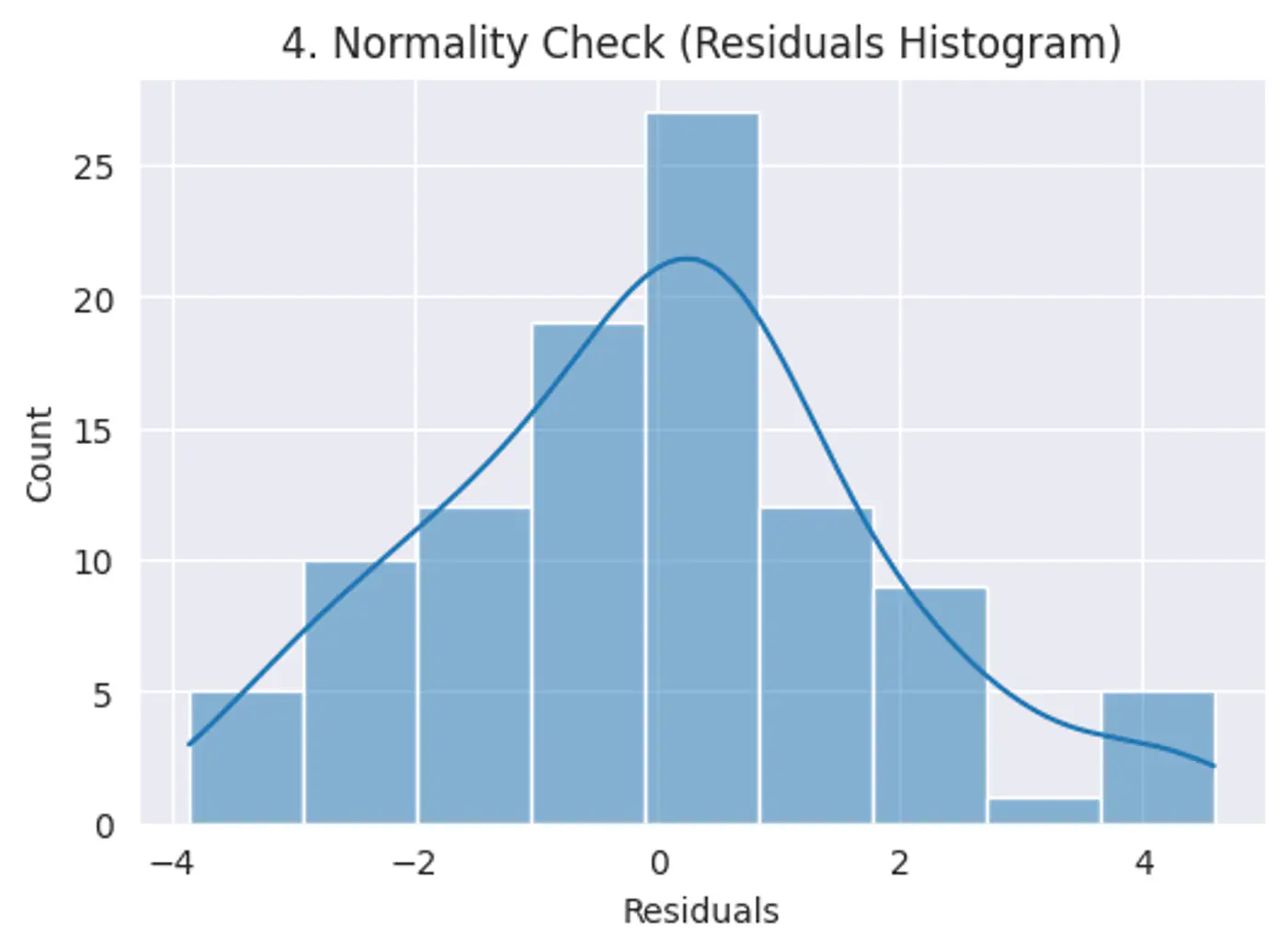

Normality of Errors

Error terms should follow a normal distribution; (Required for small datasets.)

Note: Because of Central Limit Theorem, with a large enough sample size, this becomes less critical for estimation.

Risk: Hypothesis testing (calculating p-values and confidence intervals), we assume the error terms follow a normal distribution.

Test:

Q-Q plot

Shapiro-Wilk Test

No Multicollinearity

Features should not be highly correlated with each other.

Risk:

High correlation makes it difficult to determine the unique, individual impact of each feature. This leads to high variance in model parameter estimates, small changes in data cause large swings in parameters.

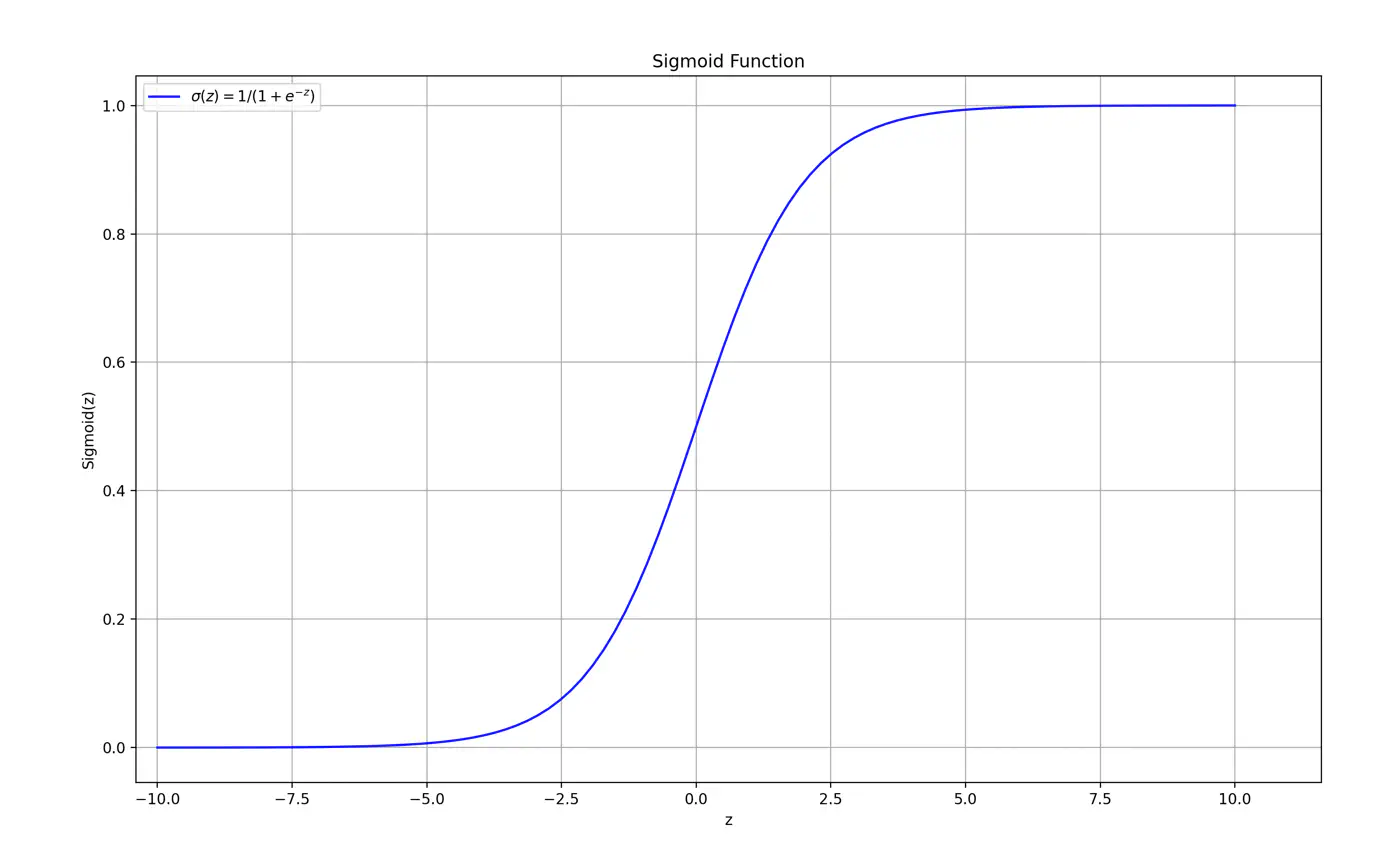

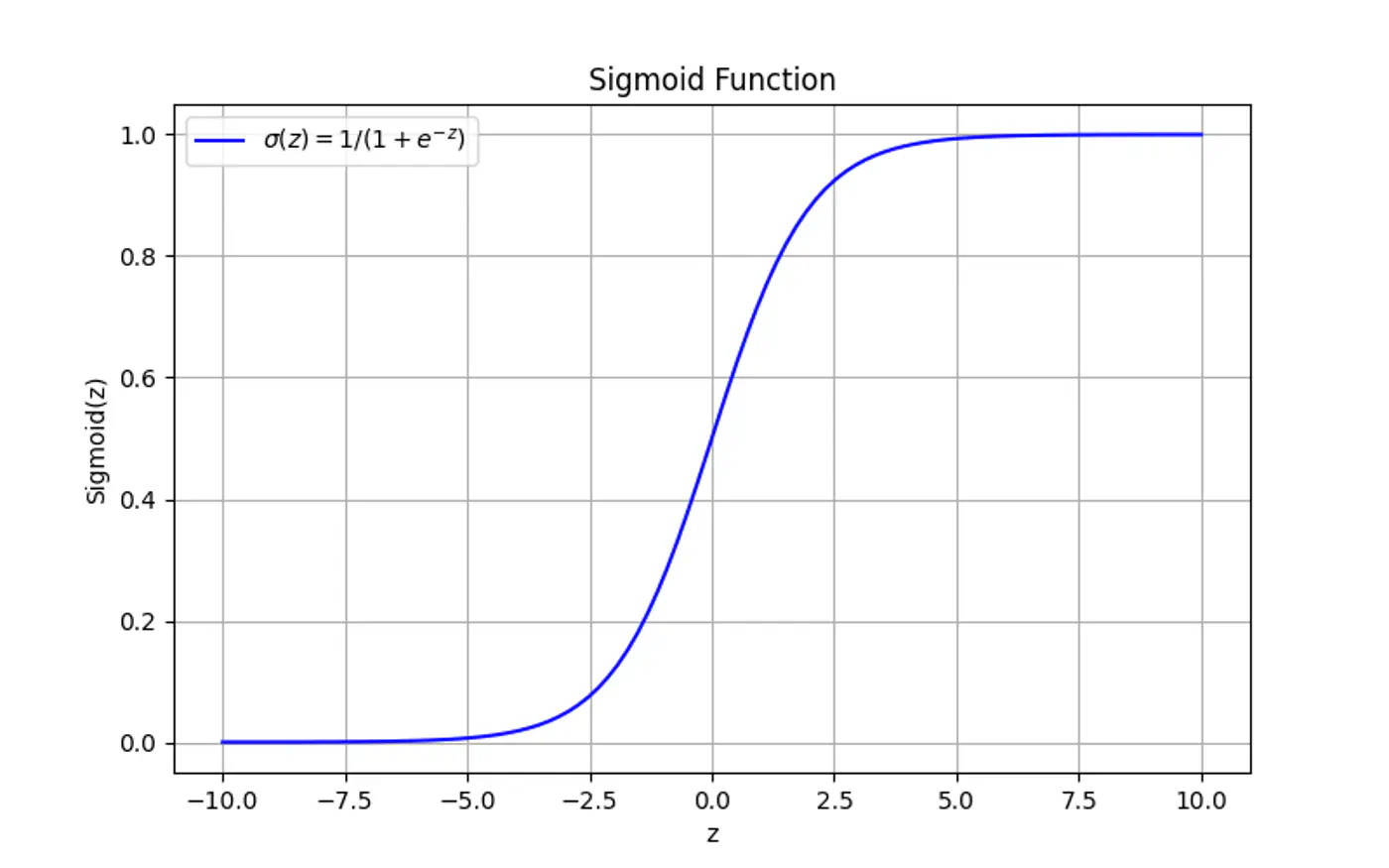

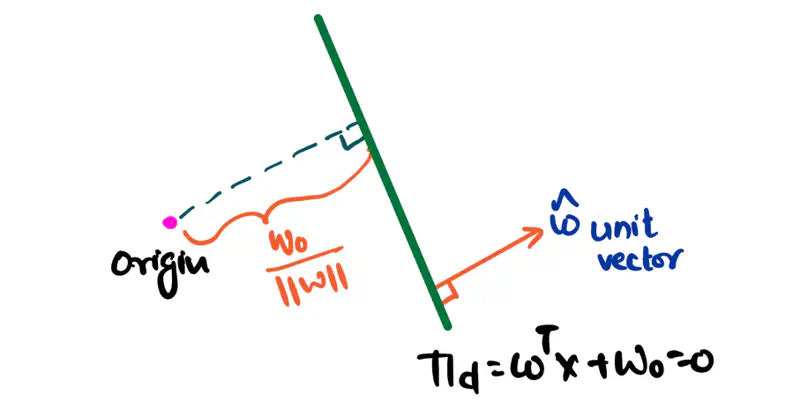

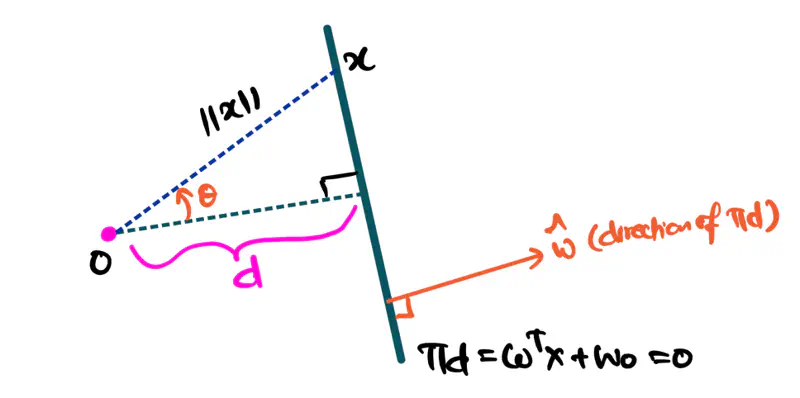

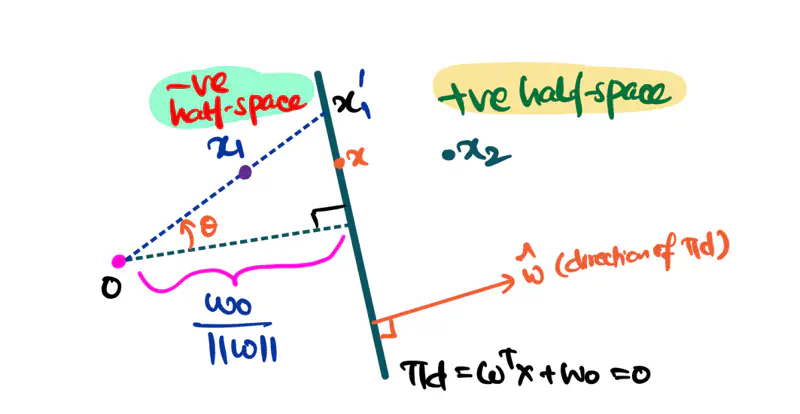

The distance of a point from the hyperplane can range from \(-\infty\) to \(+ \infty\). So we need a link 🔗 to transform the geometric distance to probability.

Sigmoid Function (a.k.a Logistic Function)

Maps the output of a linear equation to a value between 0 and 1, allowing the result to be interpreted as a probability.

\[\hat{y} = \sigma(z) = \frac{1}{1 + e^{-z}}\]

If the distance ‘z’ is large and positive, \(\hat{y} \approx 1\) (High confidence).

If the distance ‘z’ is 0, \(\hat{y} = 0.5\) (Maximum uncertainty).

Why is it called Logistic Regression ?

Because, we use the logistic (sigmoid) function as the ‘link function’🔗 to map 🗺️ the continuous output of the regression into a probability space.

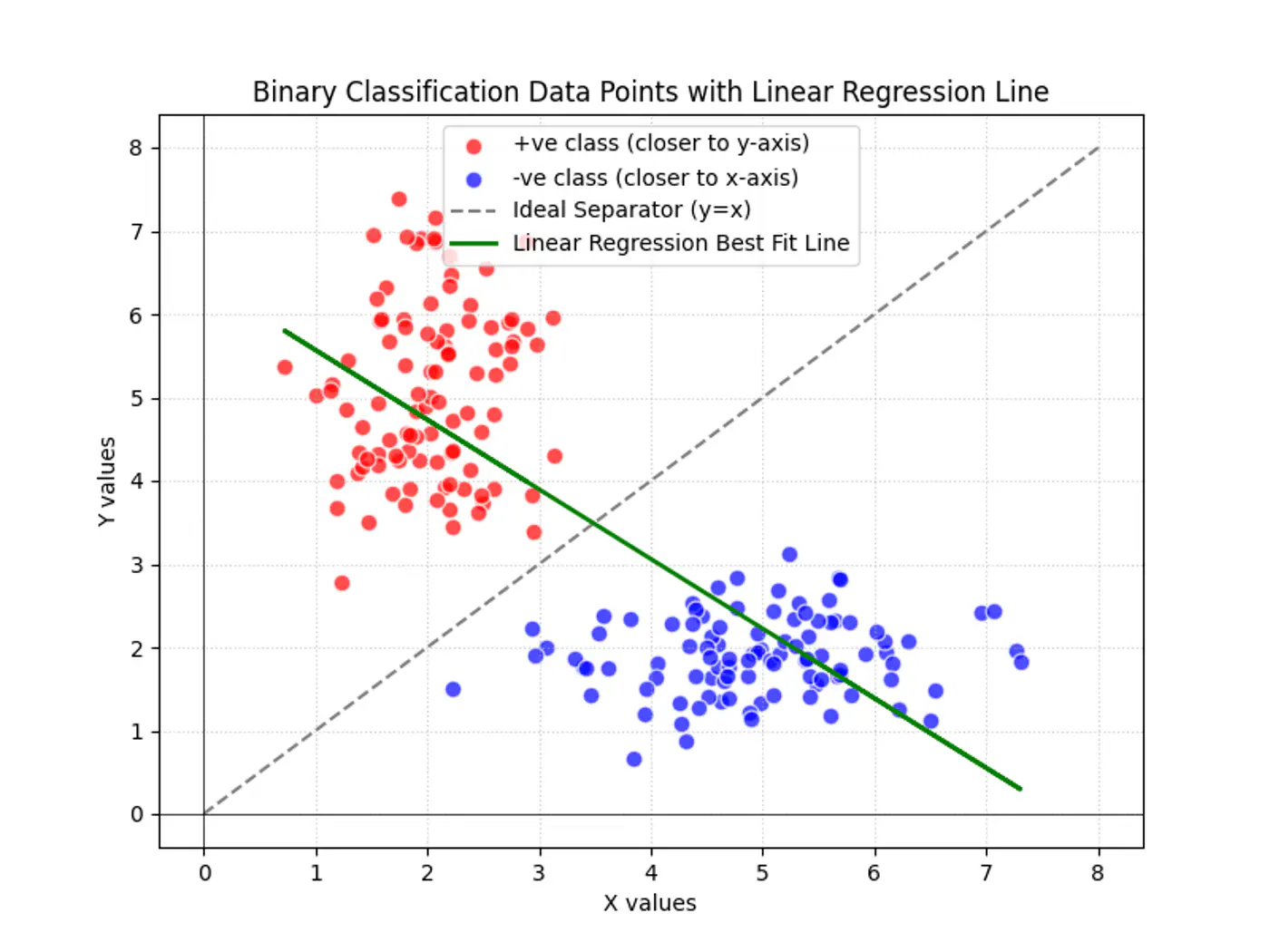

What happens to the weights of Logistic Regression if the data is perfectly linearly separable?

The weights 🏋️♀️ will tend towards infinity, preventing a stable solution.

The model tries to make probabilities exactly 0 or 1, but the sigmoid function never reaches these limits,

leading to extreme weights 🏋️♀️ to push probabilities near the extremes.

Rely on assumption that relationships between data points are linear.

For polynomial regression we need to find the degree of polynomial.

Training:

We need to train 🏃♂️the model for prediction.

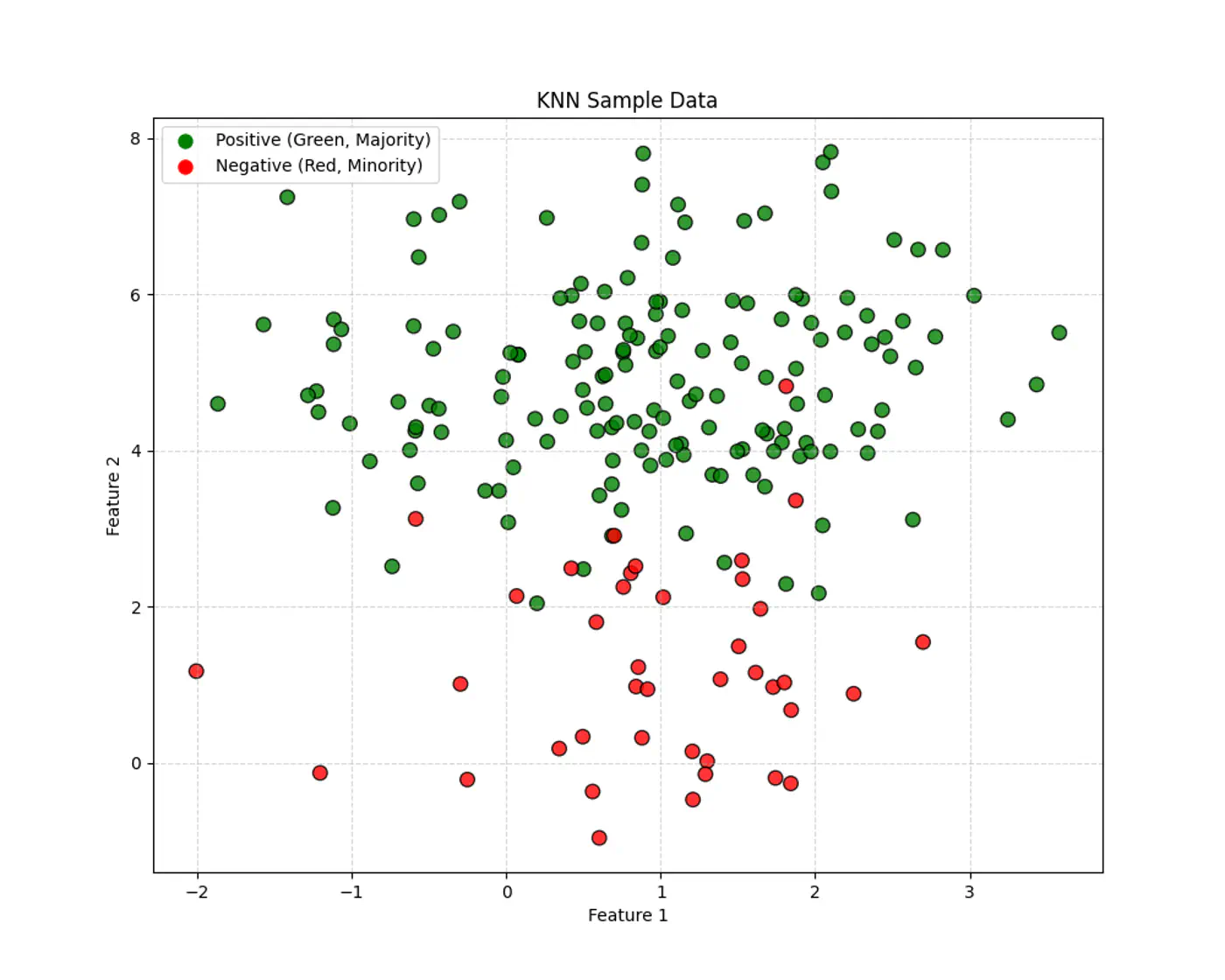

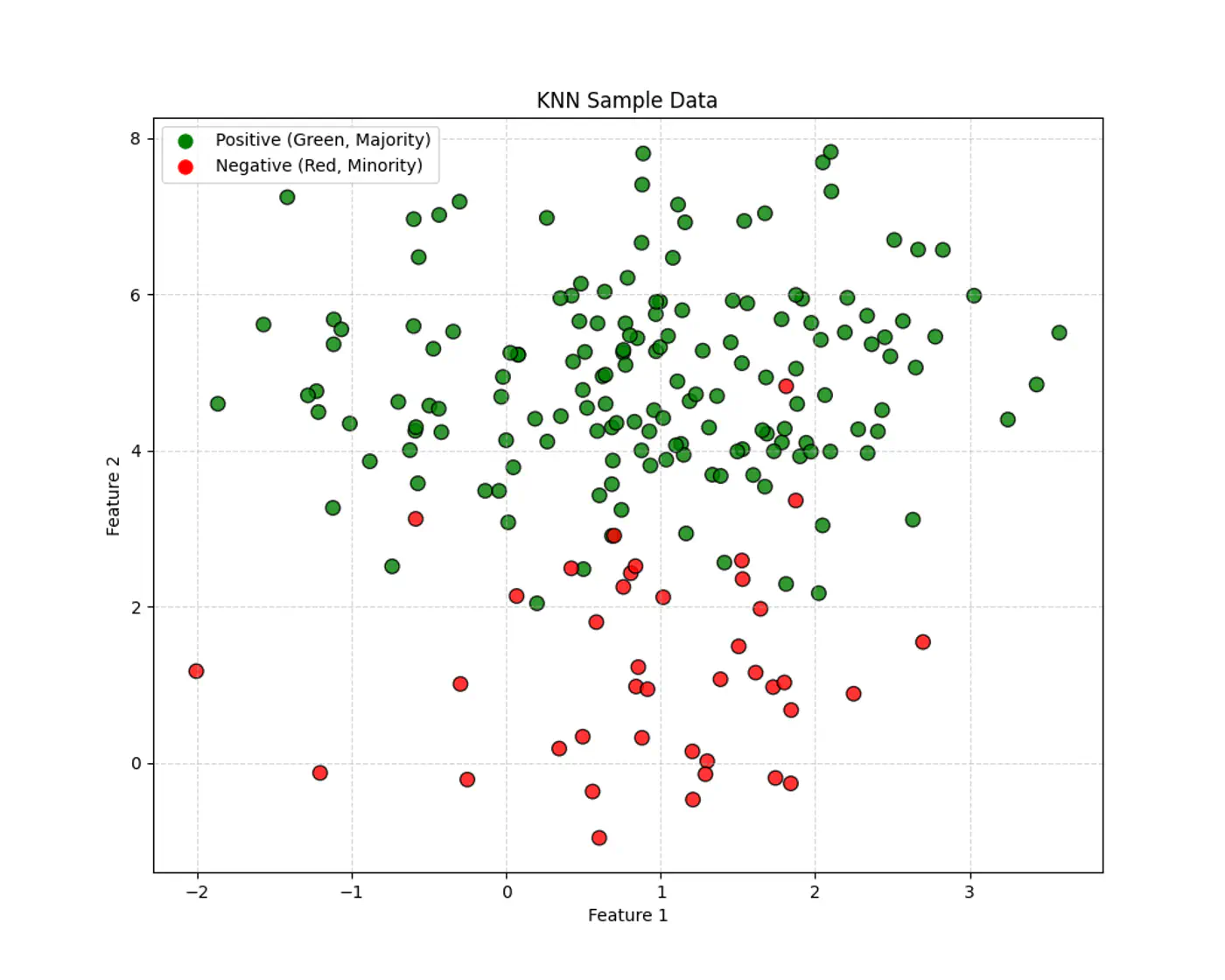

K Nearest Neighbors

Simple: Intuitive way to classify data or predict values by finding similar existing data points (neighbors).

Non-Parametric: Makes no assumptions about the underlying data distribution.

No Training Required: KNN is a ‘lazy learner’, it does not require a formal training 🏃♂️ phase.

KNN Algorithm

Given a query point \(x_q\) and a dataset, D = {\((x_i,y_i)_{i=1}^n, \quad x_i,y_i \in \mathbb{R}^d\)},

the algorithm finds a set of ‘k’ nearest neighbors \(\mathcal{N}_k(x_q) \subseteq D\).

Inference:

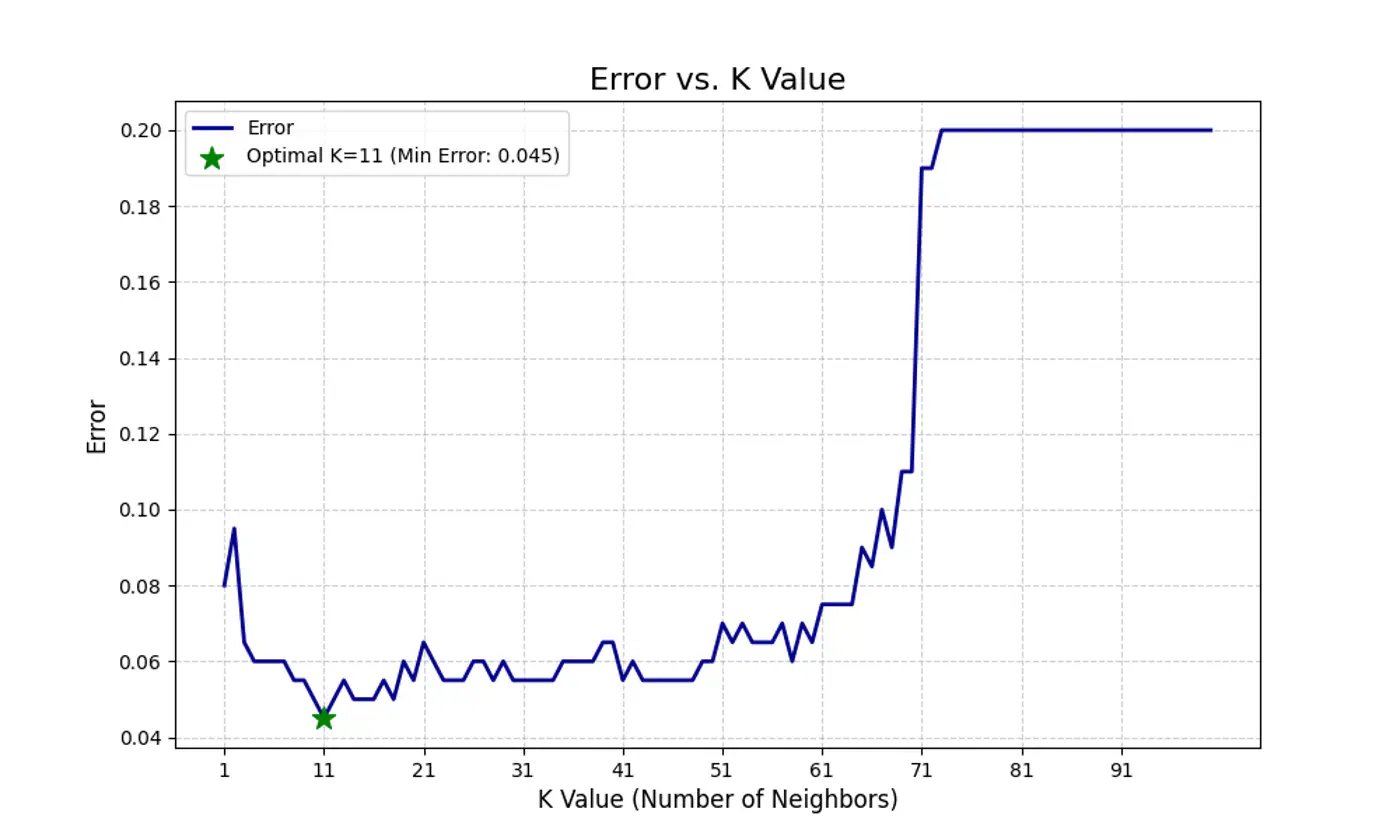

Choose a value of ‘k’ (hyper-parameter); odd number.

Calculate distance (Euclidean, Cosine etc.) between and every point in dataset and store in a distance list.

Sort the distance list in ascending order; choose top ‘k’ data points.

Make prediction:

Classification: Take majority vote of ‘k’ nearest neighbors and assign label.

Regression: Take the mean/median of ‘k’ nearest neighbors.

Note: Store entire dataset.

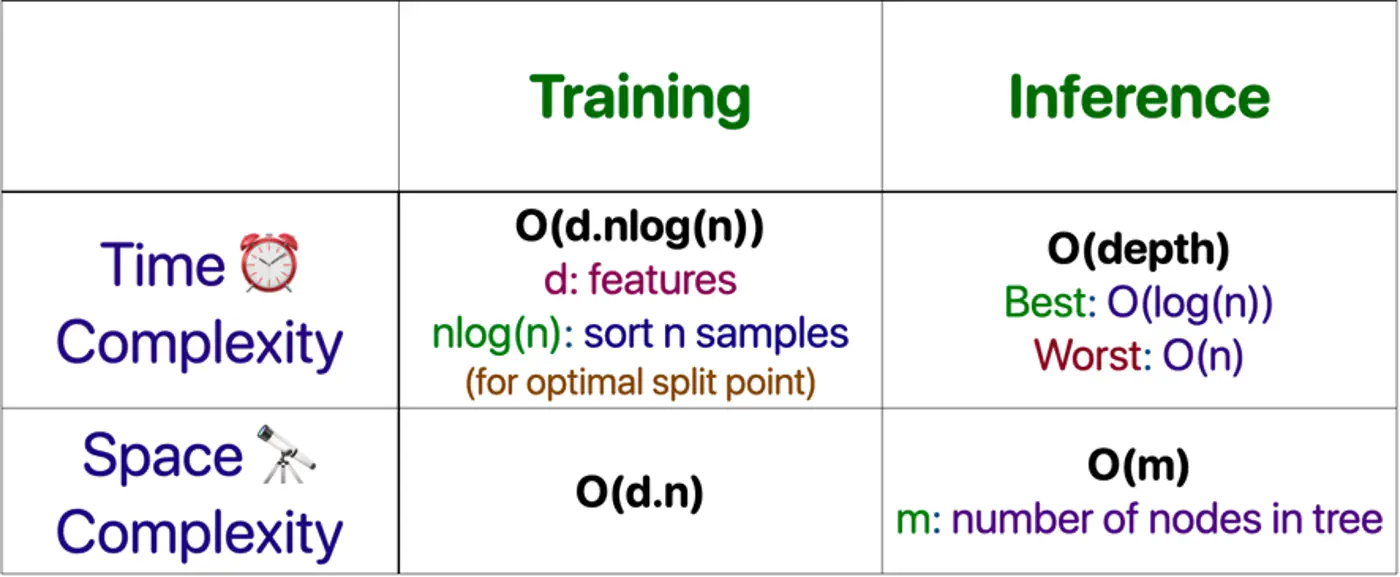

Time & Space Complexity

Storing Data: Space Complexity: O(nd)

Inference: Time Complexity ⏰: O(nd + nlogn)

Explanation:

Distance to all ’n’ points in ‘d’ dimensions: O(nd)

Sorting all ’n’ data points : O(nlogn)

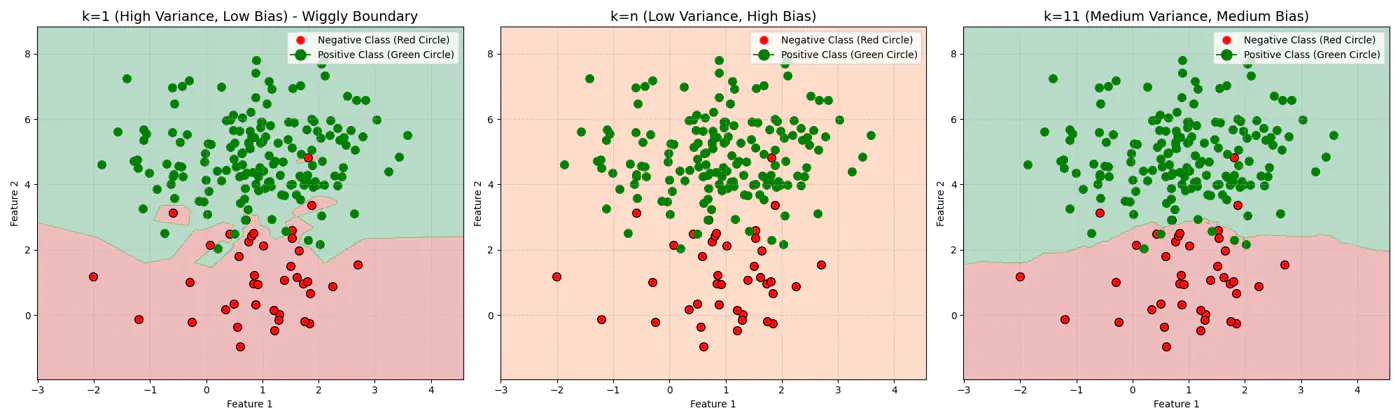

Note: Brute force 🔨 KNN is unacceptable when ’n’ is very large, say billions.

Naive KNN needs some improvements to fix some of its drawbacks.

Standardization

Distance-Weighted KNN

Mahalanobis Distance

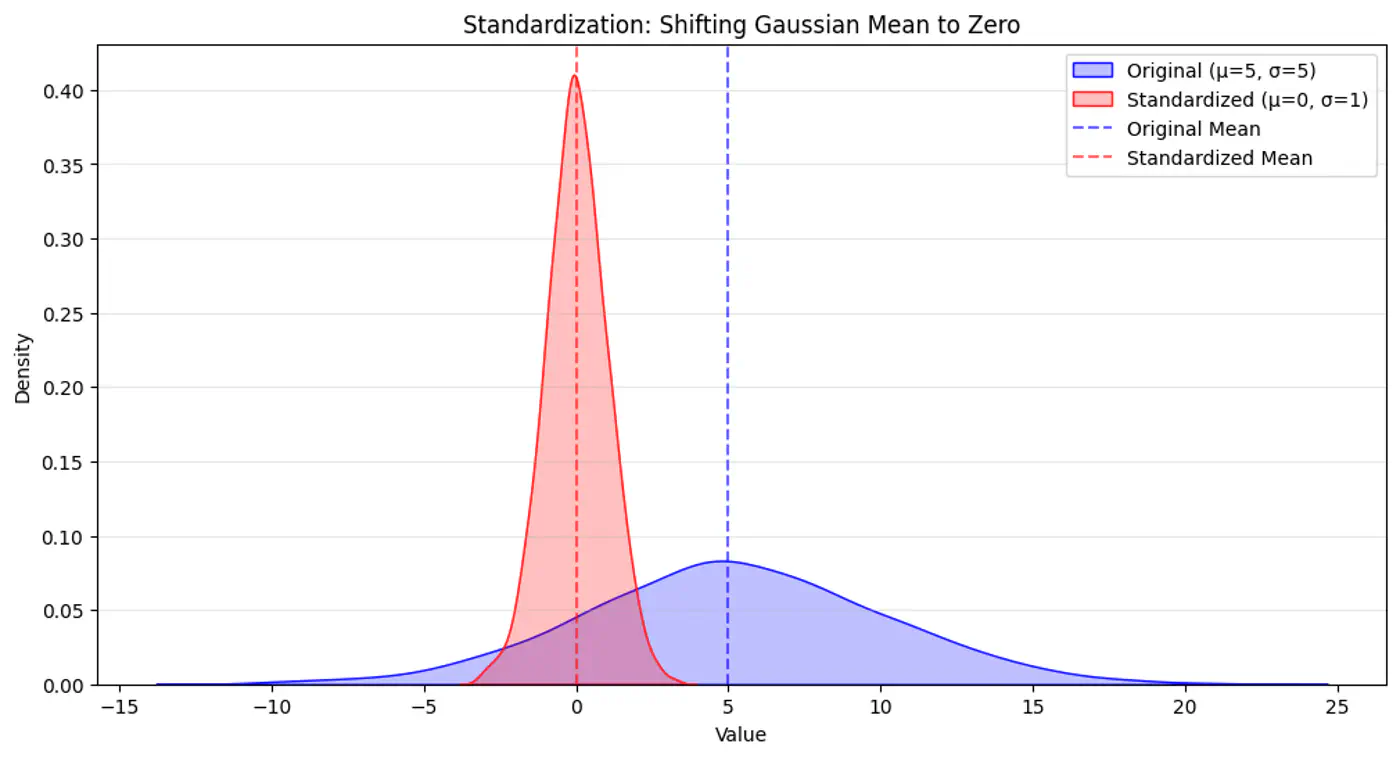

Standardization

⭐️Say one feature is ‘Annual Income’ (0-1M), and another feature is ‘Years of Experience’ (0-40).

👉The Euclidean distance will be almost entirely dominated by income 💵.

💡So, we do standardization of each feature, such that it has a mean, \(\mu\)=0 and variance,\(\sigma\)=1.

\[z=\frac{x-\mu}{\sigma}\]

Distance-Weighted KNN

⭐️Vanilla KNN treats the 1st nearest neighbor and the k-th nearest neighbor as equal.

💡A neighbor that is 0.1units away should have more influence than a neighbor that is 10 units away.

👉We assign weight 🏋️♀️ to each neighbor; most common strategy is inverse of squared distance.

\[w_i = \frac{1}{d(x_q, x_i)^2 + \epsilon}\]

Improvements:

Noise/Outlier: Reduces the impact of ‘noise’ or ‘outlier’ (distant neighbors).

Imbalanced Data: Closer points dominate, mitigating impact of imbalanced data.

e.g: If you have a query point surrounded by 2 very close ‘Class A’ points and 3 distant ‘Class B’ points, weighted 🏋️♀️ KNN will correctly pick ‘Class A'.

Mahalanobis Distance

⭐️Euclidean distance makes assumption that all the features are independent and provide unique information.

💡‘Height’ and ‘Weight’ are highly correlated.

👉If we use Euclidean distance, we are effectively ‘double-counting’ the size of the person.

🏇Mahalanobis distance measures distance in terms of standard deviations from the mean, accounting for the covariance between features.

While Euclidean distance(L norm) is the most frequently discussed, ‘Curse of Dimensionality’ impacts all Minkowski norms (\(L_p\))

\[L_p = (\sum |x_i|^p)^{\frac{1}{p}} \]

Note: ‘Curse of Dimensionality’ is largely a function of the exponent (p) in the distance calculation.

Issues with High Dimensional Data

Coined 🪙 by mathematician John Bellman in the 1960s while studying dynamic programming.

High dimensional data created following challenges:

Distance Concentration

Data Sparsity

Exponential Sample Requirement

Distance Concentration

💡Consider a hypercube in d-dimensions of side length = 1; Volume = \(1^d\) = 1 🧊 A smaller inner cube with side length = 1 - \(\epsilon\) ; Volume = \((1 -\epsilon)^d\)

🧐 This implies that almost all the volume of the high-dimensional cube lies near the ‘crust’. 👉e.g: if \(\epsilon\)= 0.01, d = 500; Volume of inner cube = \((1 -0.01)^{500}\) = \(0.99^{500}\) = 0.006 = 0.6% 🤔Consequently, all points become nearly equidistant, and the concept of ‘nearest’ or ‘neighborhood’ loses

its meaning.

Data Sparsity

⭐️The volume of the feature space increases exponentially with each added dimension.

👉To maintain the same data density found in a 1D space with 10 points, we would need \(10^{10}\)(10 billion) points in 10D space.

💡Because real-world datasets are rarely this large, the data becomes “sparse,” making it difficult to find truly similar neighbors.

Exponential Sample Requirement

⭐️To maintain a reliable result, the amount of training data needed must grow exponentially with the number of dimensions.

👉Without this growth, the model is highly prone to overfitting, where it learns from noise in the ‘sparse’ data

rather than actual underlying patterns.

Note: For modern embeddings (often 768 or 1536 dimensions), it is mathematically impossible to collect enough data

to ‘fill’ the space.

Solution

Cosine Similarity

Normalization

Cosine Similarity

Cosine similarity measures the cosine of the angle between 2 vectors.

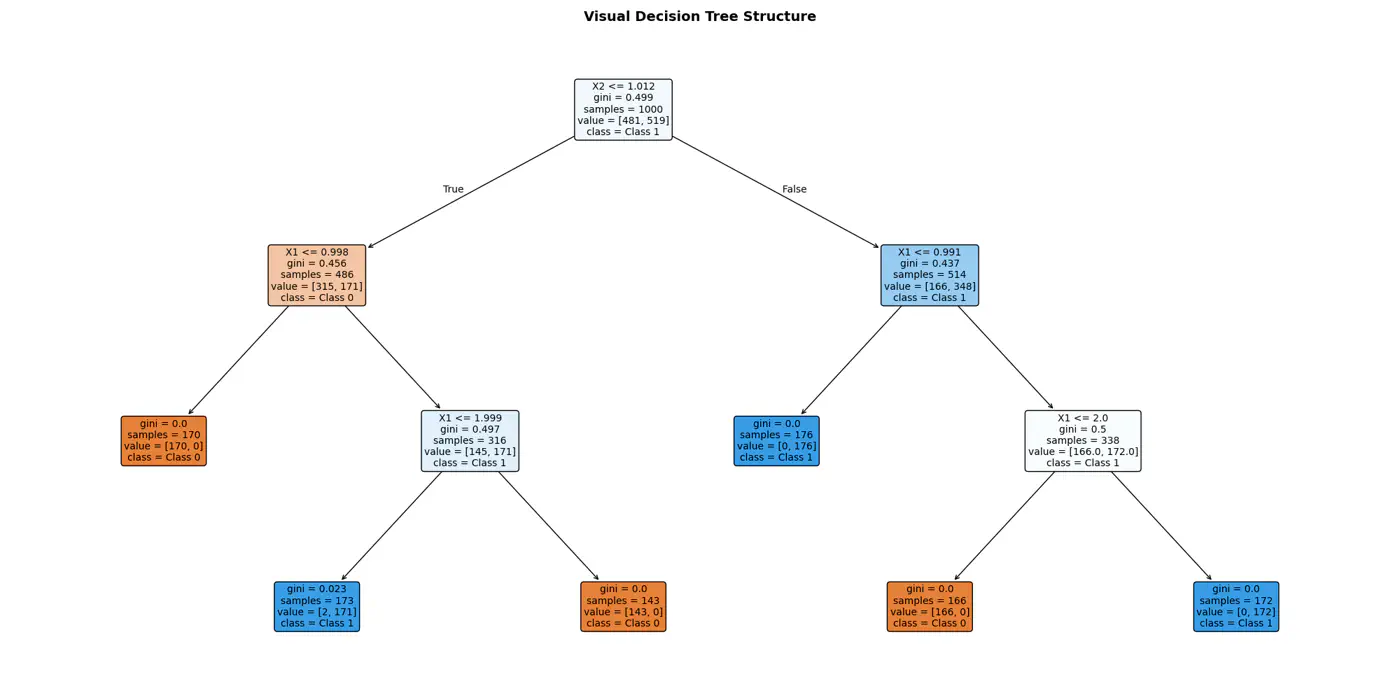

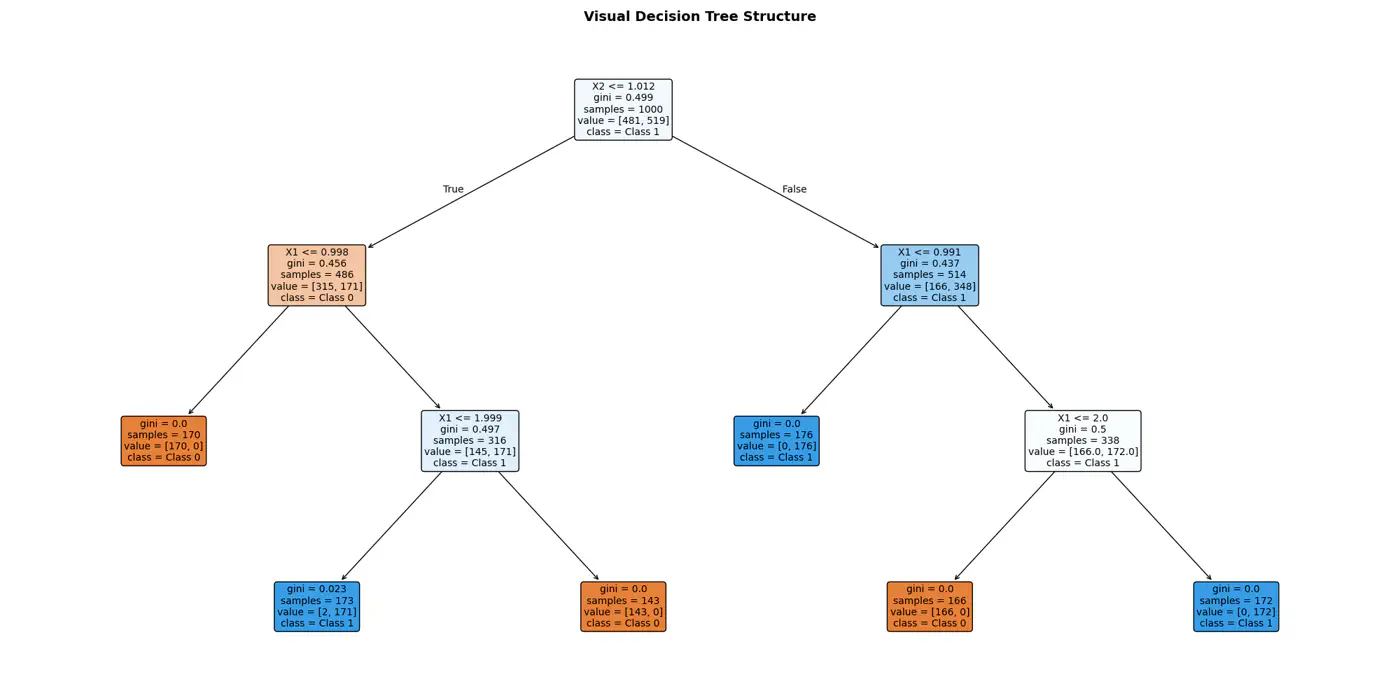

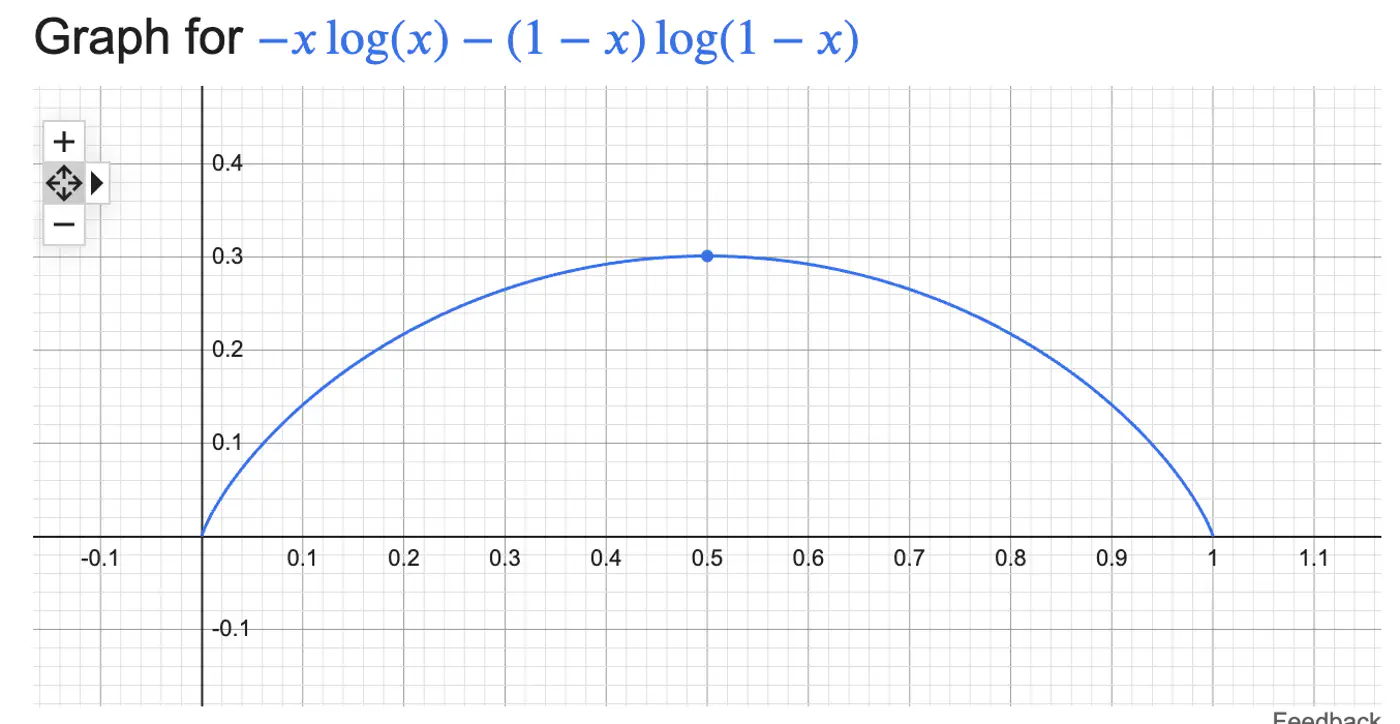

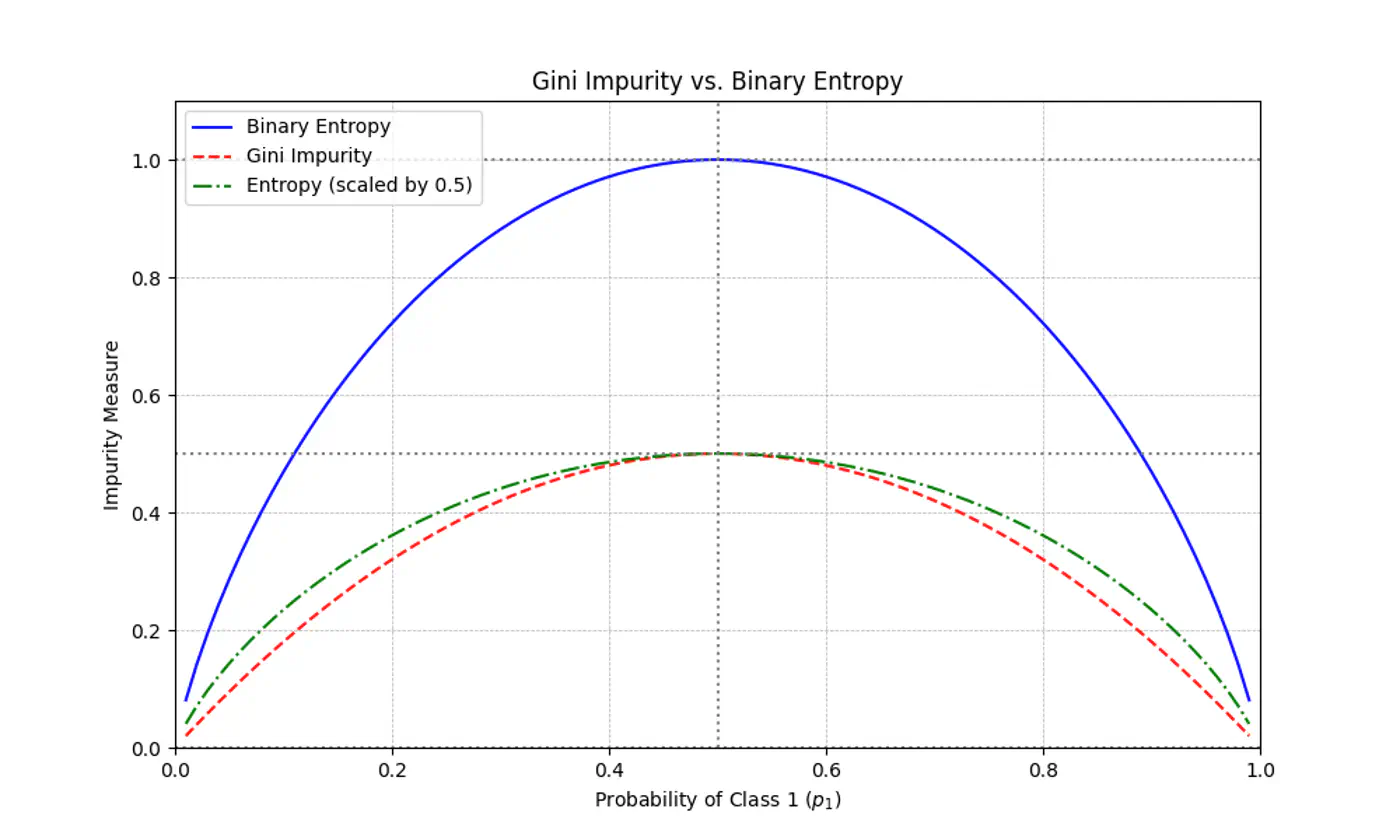

Note: The goal of a decision tree algorithm is to find the split that maximizes information gain, meaning it removes the most uncertainty from the data.

Gini 🧞♂️Impurity

⭐️ Measures the probability of an element being incorrectly classified if it were randomly labeled according to the distribution of labels in a node.

\[Gini(S)=1-\sum_{i=1}^{n}(p_{i})^{2}\]

Range: 0 (Pure) - 0.5 (Maximum impurity)

Note: Gini is used in libraries like Scikit-Learn (as the default), because it avoids the computationally expensive 💰 log function.

Gini Impurity Vs Entropy

Gini Impurity is a first-order approximation of Entropy.

For most of the real-world cases, choosing one over the other results in the exact same tree structure or negligible differences in accuracy.

When we plot the two functions, they follow nearly identical shapes.

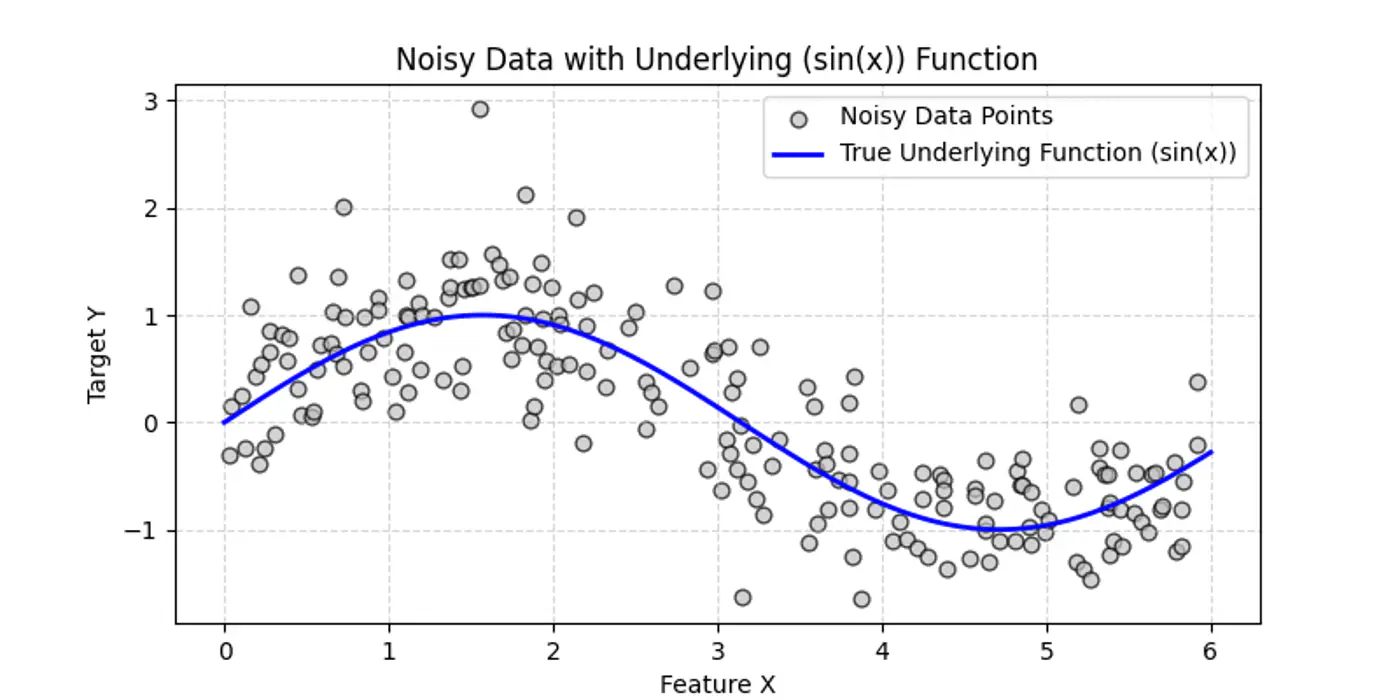

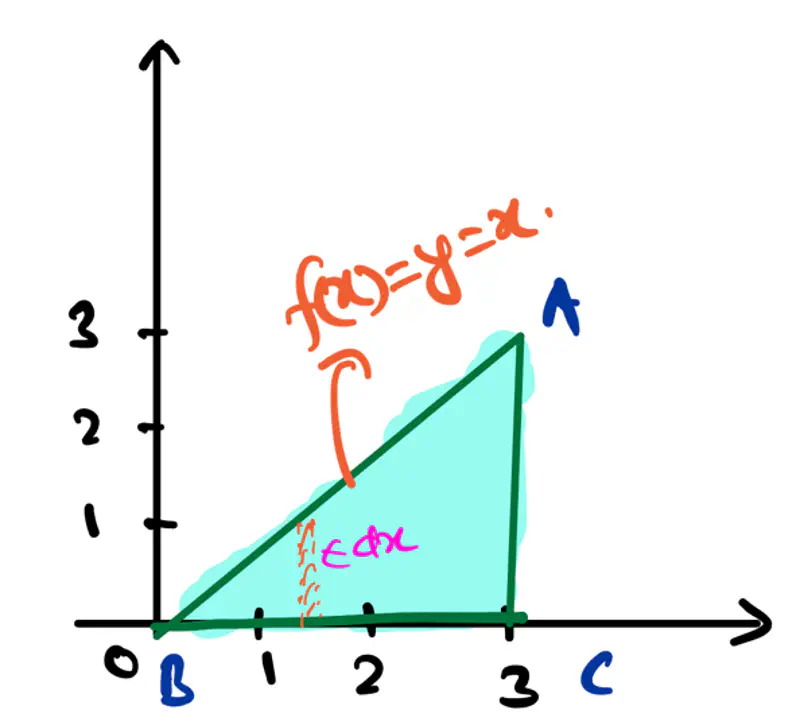

Decision Trees can also be used for Regression tasks but using a different metrics.

⭐️Metric:

Mean Squared Error (MSE)

Mean Absolute Error (MAE)

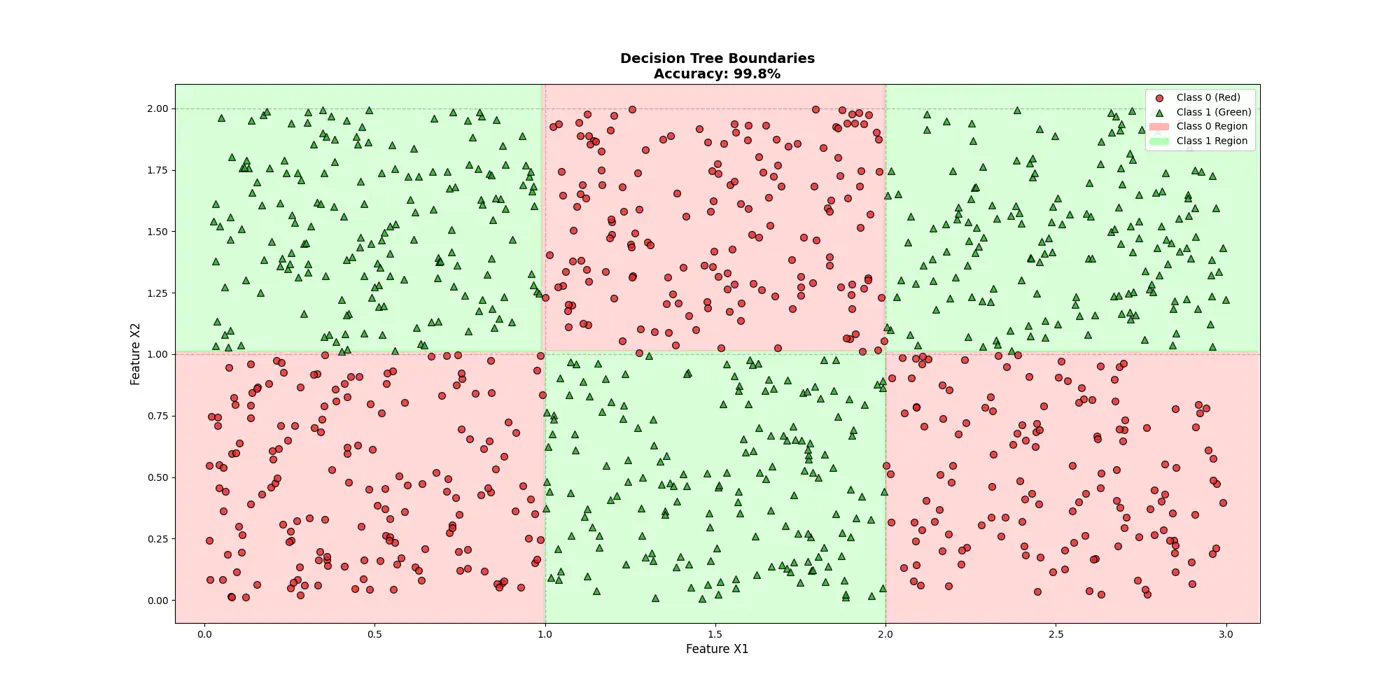

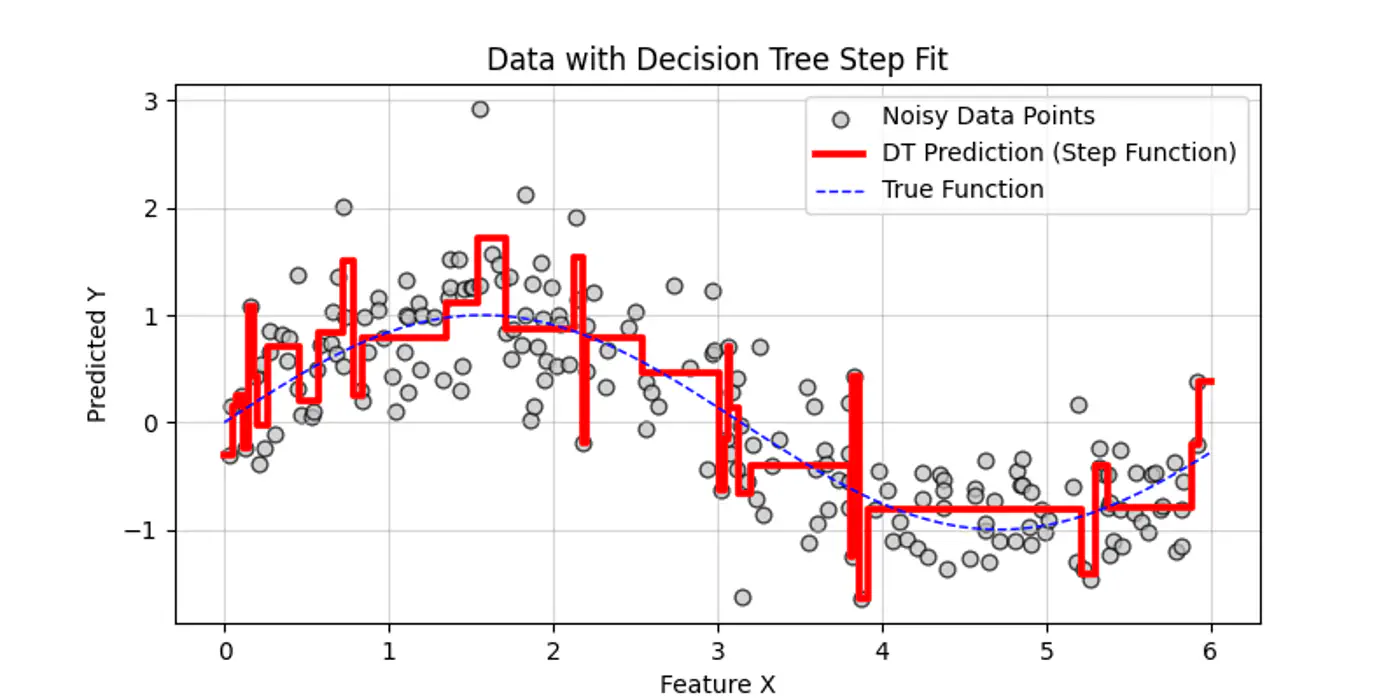

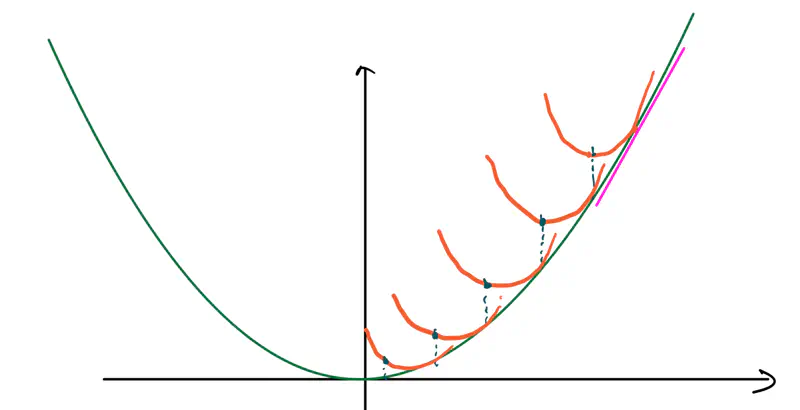

👉Say we have a following dataset, that we need to fit using decision trees:

👉Decision trees try to find the decision splits, building step functions that approximate the actual curve,

as shown below:

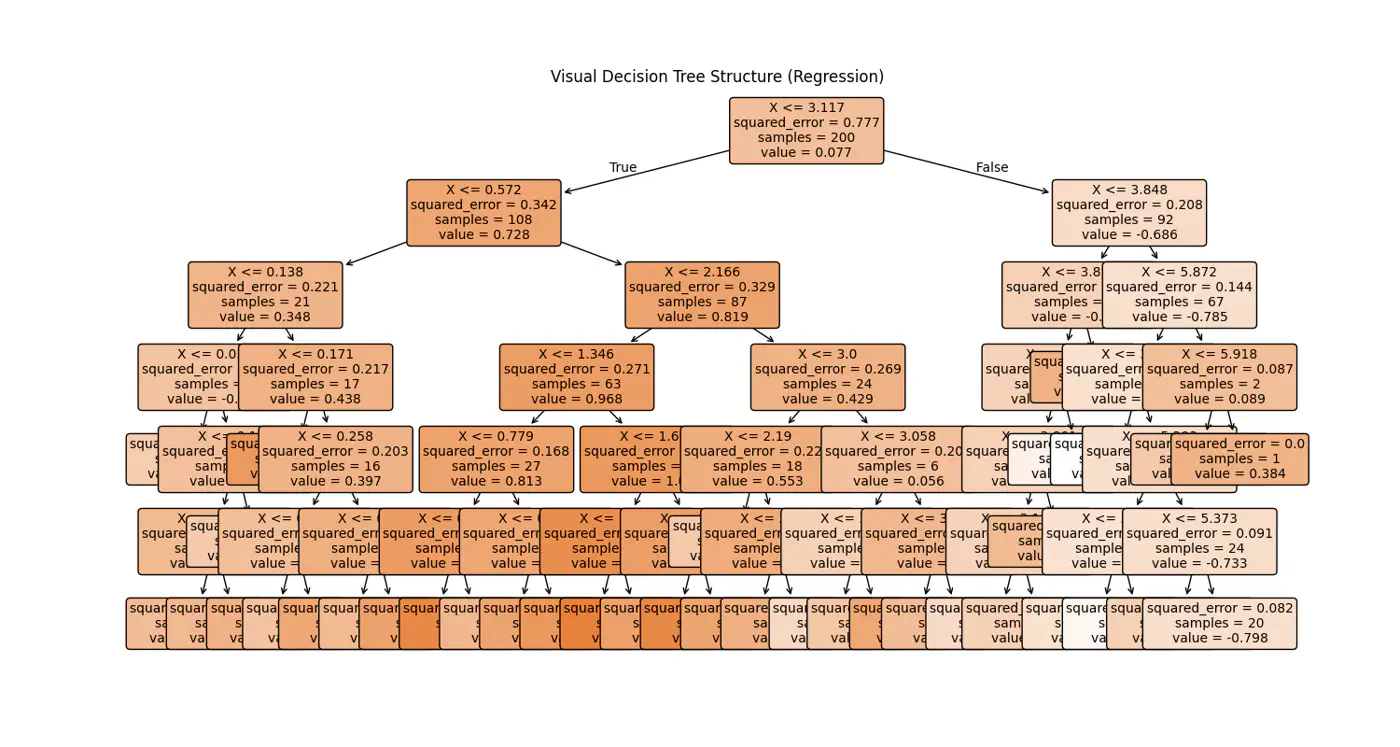

👉Internally the decision tree (if else ladder) looks like below:

Can we use decision trees for all kinds of regression?

Or is there any limitation ?

Decision trees cannot predict values outside the range of the training data, i.e, extrapolation.

Let’s understand the interpolation and extrapolation cases one by one.

Interpolation ✅

⭐️Predicting values within the range of features and targets observed during training 🏃♂️.

Trees capture discontinuities perfectly, because they are piece-wise constant.

They do not try to force a smooth line where a ‘jump’ exists in reality.

e.g: Predicting a house 🏡 price 💰 for a 3-BHK home when you have seen 2-BHK and 4-BHK homes in that same neighborhood.

Extrapolation ❌

⭐️Predicting values outside the range of training 🏃♂️data.

Problem: Because a tree outputs the mean of training 🏃♂️ samples in a leaf, it cannot predict a value higher than the

highest ‘y’ it saw during training 🏃♂️.

Flat-Line: Once a feature ‘X’ goes beyond the training boundaries, the tree falls into the same ‘last’ leaf forever.

e.g: Predicting the price 💰 of a house 🏡 in 2026 based on data from 2010 to 2025.

⭐️Because trees🌲 are non-parametric and ‘greedy’💰, they will naturally try to grow 📈 until every leaf 🍃 is pure,

effectively memorizing noise and outliers rather than learning generalizable patterns.

Tree 🌲 Size

👉As the tree 🌲 grows, the amount of data in each subtree decreases 📉, leading to splits based on statistically insignificant samples.

max_depth: Limits how many levels of ‘if else’ the tree can have; most common.

min_samples_split: A node will only split, if it has at least ‘N’ samples; smooths the model (especially in regression), by ensuring predictions are based on an average of multiple points.

max_leaf_nodes: Limiting the number of leaves reduces the overall complexity of the tree, making it simpler and less likely to memorize the training data’s noise.

min_impurity_decrease: A split is only made if it reduces the impurity (Gini/MSE) by at least a certain threshold.

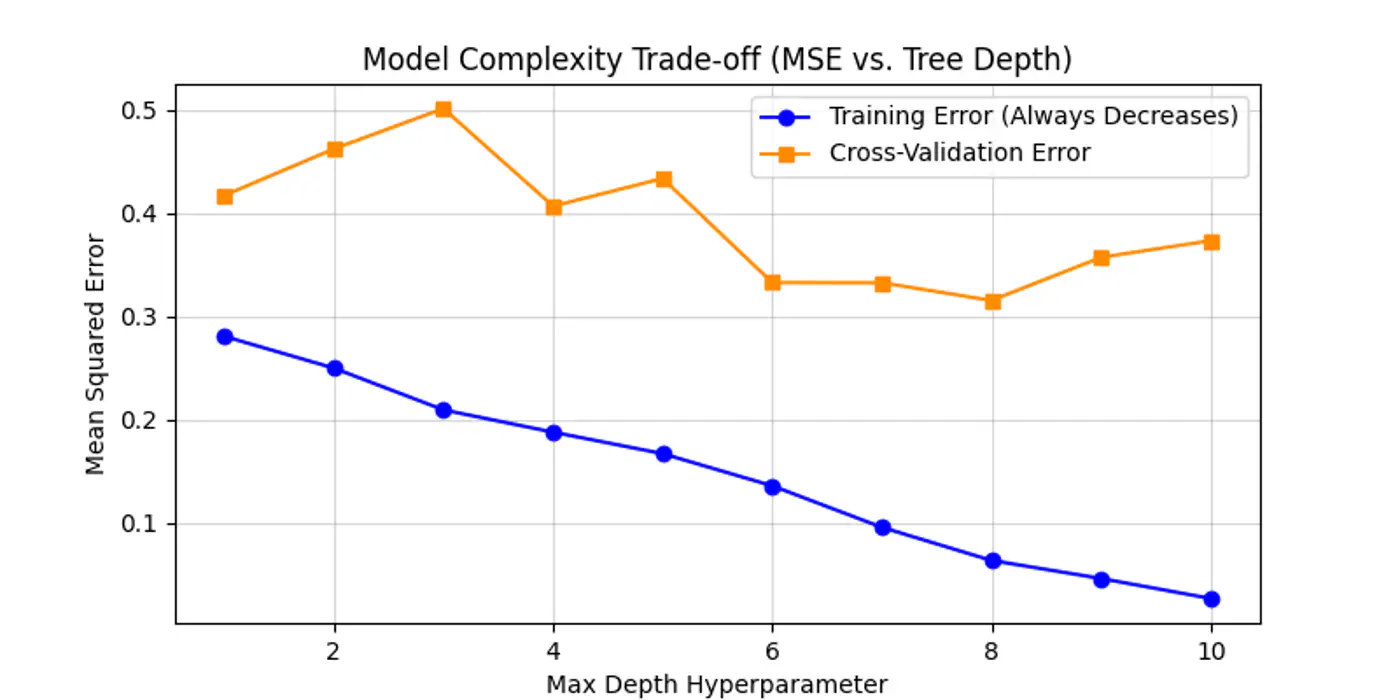

Max Depth Hyper Parameter Tuning

Below is an example for one of the hyper-parameter’s max_depth tuning.

As we can see below the cross-validation error decreases till depth=6 and after that

reduction in error is not so significant.

Post-Pruning ✂️

Let the tree🌲 grow to its full depth (overfit) and then ‘collapse’ nodes that provide little predictive value.

Most common algorithm:

Minimal Cost Complexity Pruning

Minimal Cost Complexity Pruning ✂️

💡Define a cost-complexity 💰 measure that penalizes the tree 🌲 for having too many leaves 🍃.

\[R_\alpha(T) = R(T) + \alpha |T|\]

R(T): total misclassification rate (or MSE) of the tree

|T|: number of terminal nodes (leaves)

\(\alpha\): complexity parameter (the ‘tax’ 💰 on complexity)

Logic:

If \(\alpha\)=0, the tree is the original overfit tree.

As \(\alpha\) increases 📈, the penalty for having many leaves grows 📈.

To minimize the total cost 💰, the model is forced to prune branches that do not significantly reduce R(T).

Use cross-validation to find the ‘sweet spot’ \(\alpha\) that minimizes validation error.

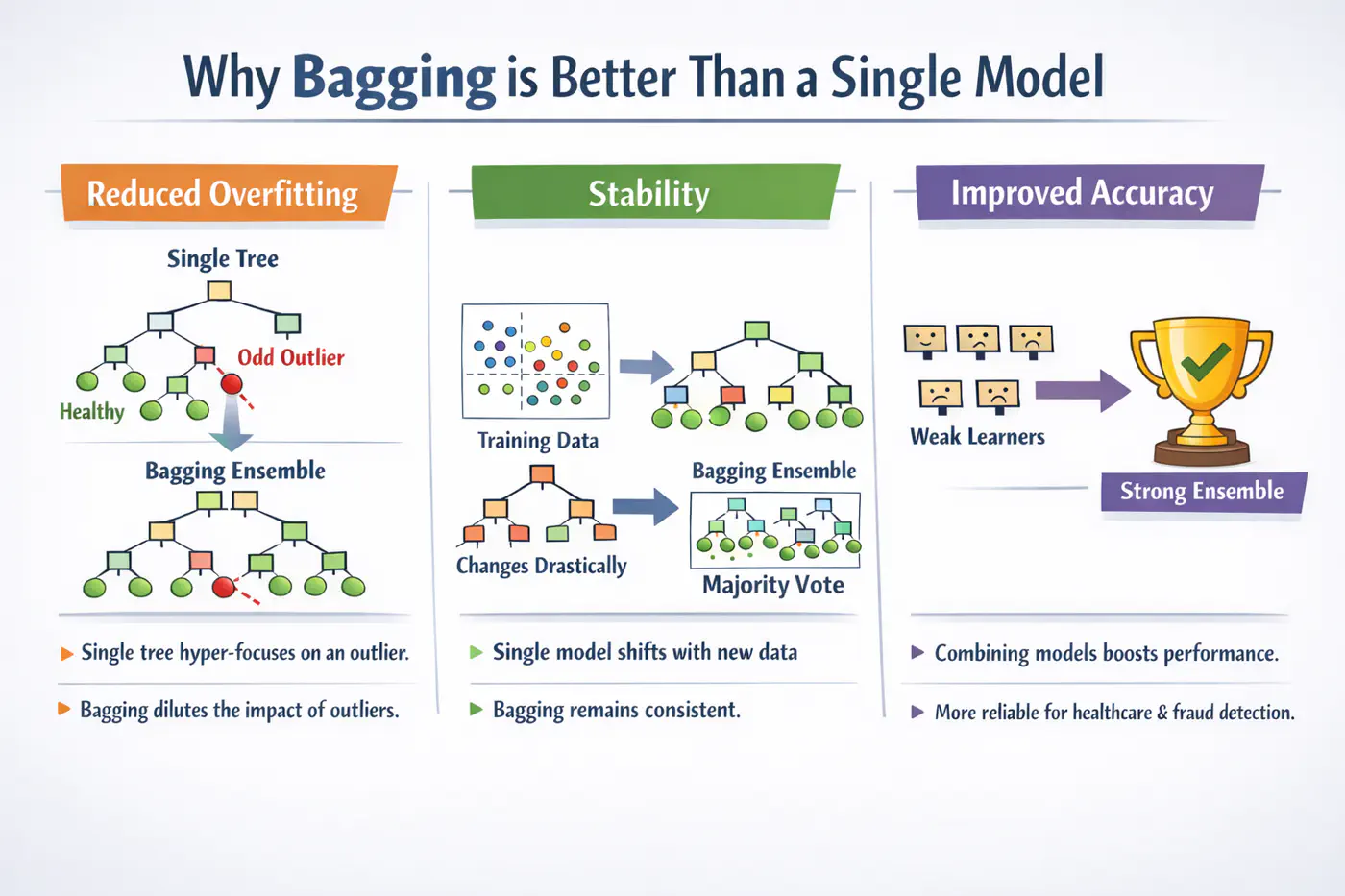

A single decision tree is highly sensitive to the specific training dataset. Small changes, such as, a few different rows or the presence of an outlier, can lead to a completely different tree structure.

Unpruned decision trees often grow until they perfectly classify the training set, essentially ‘memorizing’

noise and outliers, i.e, high variance, rather than finding general patterns.

What does Bagging mean 🤔?

Bagging = ‘Bootstrapped Aggregation’

Bagging 🎒is a parallel ensemble technique that reduces variance (without significantly increasing the bias)

by training multiple versions of the same model on different random subsets of data and then combining their results.

Note: Bagging uses deep trees (overfit) and combines them to reduce variance.

Bootstrapping

Bootstrapping = ‘Without external help’

Given a training 🏃♂️set D of size ’n’, we create B new training sets D by sampling ’n’ observations from D ‘with replacement'.

Bootstrapped Samples

💡Since, we are sampling ‘with replacement’, so, some data points may be picked multiple times,

while others may not be picked at all.

The probability that a specific observation is not selected in a bootstrap sample of size ’n’ is:

\[\lim_{n \to \infty} \left(1 - \frac{1}{n}\right)^n = \frac{1}{e} \approx 0.368\]

🧐This means each tree is trained on roughly 63.2% of the unique data, while the

remaining 36.8% (the Out-of-Bag or OOB set) can be used for cross validation.

Aggregation

⭐️Say we train ‘B’ models (base-learners), each with variance \(\sigma^2\) .

👉Average variance of ‘B’ models (trees) if all are independent:

\[Var(X)=\frac{\sigma^{2}}{B}\]

👉Since, bootstrap samples are derived from the same dataset, the trees are correlated with some

correlation coefficient ‘\(\rho\)'.

💡Choose a randomsubset of ‘m’ features from the total ‘d’ features, reducing the correlation ‘\(\rho\)’ between trees.

👉By forcing trees to split on ‘sub-optimal’ features, we intentionally increase the variance of individual trees;

also the bias is slightly increased (simpler trees).

Standard heuristics:

Classification: \(m = \sqrt{d}\)

Regression: \(m = \frac{d}{3}\)

Math of De-Correlation

💡Because ‘\(\rho\)’ is the dominant factor in the variance of the ensemble when B is large,

the overall ensemble variance Var(\(f_{rf}\)) drops significantly lower than standard Bagging.

💡In a standard Decision Tree or Random Forest, the algorithm searches for the optimal split point (the threshold ’s’)

that maximizes Information Gain or minimizes MSE.

👉This search is:

computationally expensive (sort + mid-point) and

tends to follow the noise in the training 🏃♂️data.

Adding Randomness

Adding randomness (right kind) in ensemble averaging reduces correlation/variance.

Random Thresholds: Instead of searching for the best split point (computationally expensive 💰) for a feature,

it picks a threshold at random from a uniform distribution between the feature’s local minimum and maximum.

Entire Dataset: Uses entire training dataset (default) for every tree; no bootstrapping.

Random Feature Subsets: Random subset of m<n features is used in each decision tree.

Structural correlation between trees becomes extremely low.

Individual trees are ‘weaker’ and have higher bias than a standard optimized tree.

👉The massive drop in ‘\(\rho\)’ often outweighs the slight increase in bias, leading to an overall ensemble that is

smoother and more robust to noise than a standard Random Forest.

Note: Extra Trees are almost always grown to full depth, as they may need extra splits to find the same decision boundary.

When to use Extra Trees ?

Performance: Significantly faster to train, as it does not sort data to find optimal split. Note: If we are working with billions of rows or thousands of features, ET can be 3x to 5x faster than a Random Forest(RF).

Robustness to Noise: By picking thresholds randomly, tends to ‘handle’ the noise more effectively than RF.

Feature Importance: Because ET is so randomized, it often provides more ‘stable’ feature importance scores.

Note: It is less likely to favor a high-cardinality feature (e.g. zip-code) just because it has more potential split points.

⭐️In Bagging 🎒we trained multiple strong(over-fit, high variance) models (in parallel) and then averaged them out to reduce variance.

💡Similarly, we can train many weak(under-fit, high bias) models sequentially, such that, each new model corrects the errors of the previous ones to reduce bias.

Boosting

⚔️ An ensemble learning approach where multiple ‘weak learners’ (typically simple models like shallow decision trees 🌲 or ‘stumps’)

are sequentially combined to create a single strong predictive model.

⭐️The core principle is that each subsequent model focuses 🎧 on correcting the errors made by its predecessors.

Why is Boosting Better ?

👉Boosting generally achieves better predictive performance because it actively reduces bias by learning 📖from ‘past mistakes’, making it ideal for achieving state-of-the-art 🖼️ results.

💡Works by increasing 📈 the weight 🏋️♀️ of misclassified data points after each iteration, forcing the next weak learner to

‘pay more attention’🚨 to the difficult cases.

⭐️ Commonly used for classification.

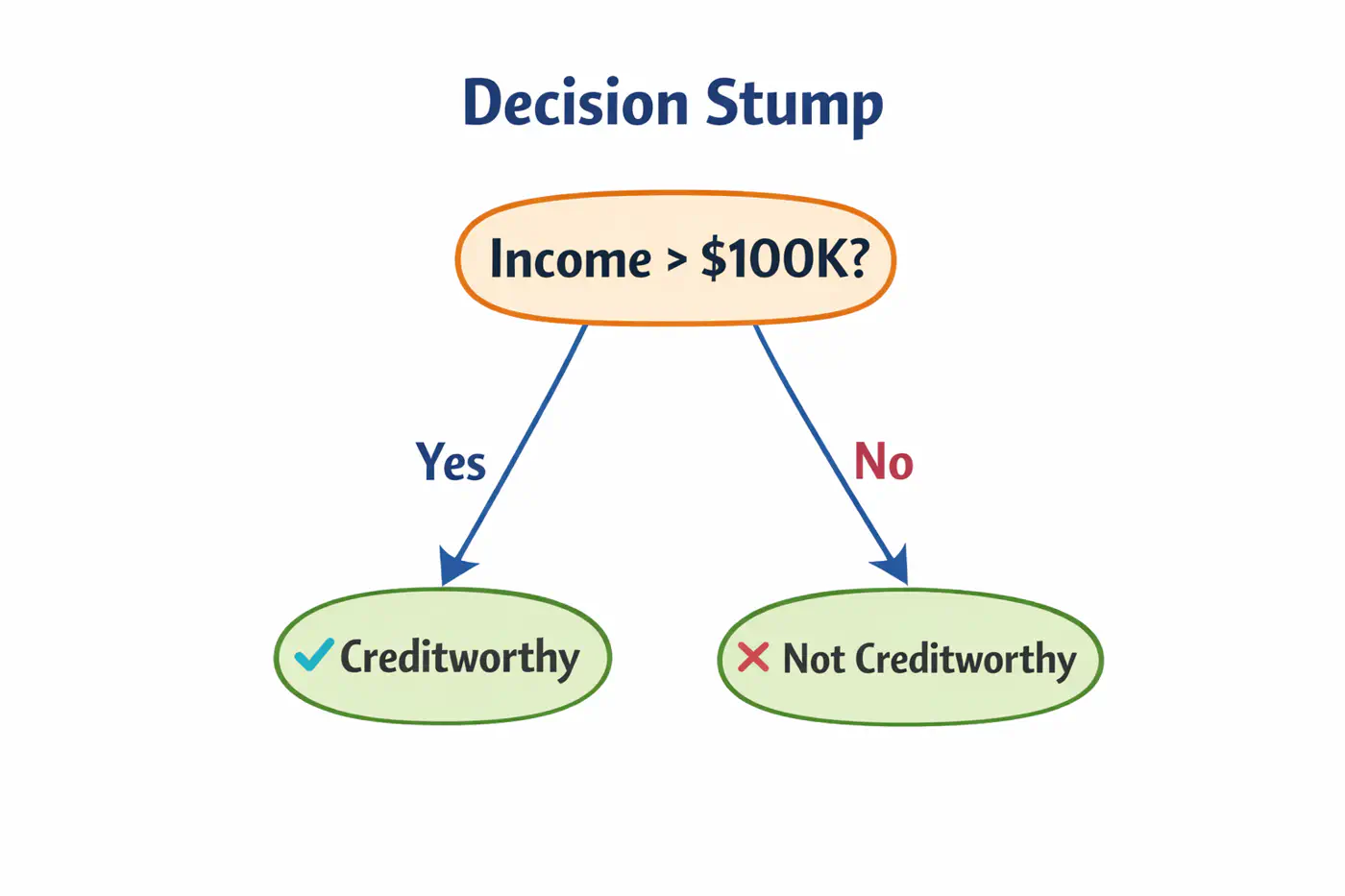

Decision Stumps

👉Weak learners are typically ‘Decision Stumps’, i.e, decision trees🌲with a depth of only one (1 split, 2 leaves 🍃).

Algorithm

Assign an equal weight 🏋️♀️to every data point; \(w_i = 1/n\), where ’n’=number of samples.

Build a decision stump that minimizes the weighted classification error.

Calculate total error; \(E_m = \Sigma w_i\).

Determine ‘amount of say’, i.e, the weight 🏋️♀️ of each stump in final decision.

\[\alpha_m = \frac{1}{2}ln\left( \frac{1-E_m}{E_m} \right)\]

Low error results in a high positive \(\alpha\) (high influence).

50% error (random guessing) results in an \(\alpha = 0\) (no influence).

Update sample weights 🏋️♀️.

Misclassified samples: Weight 🏋️♀️ increases by \(e^{\alpha_m}\).

Correctly classified samples: Weight 🏋️♀️ decreases by \(e^{-\alpha_m}\).

Normalization: All new weights 🏋️♀️ are divided by their total sum so they add up back to 1.

Iterate for a specified number of estimators (n_estimators).

Final Prediction 🎯

👉 To classify a new data point, every stump makes a prediction (+1 or -1).

These are multiplied by their respective ‘amount of say’ \(\alpha_m\) and summed.

\[H(x)=sign\sum_{m=1}^{M}\alpha_{m}⋅h_{m}(x)\]

👉 If the total weighted 🏋️♀️ sum is positive, the final class is +1; otherwise -1.

Note: Sensitive to outliers; Because AdaBoost aggressively increases weights 🏋️♀️ on misclassified points, it may ‘over-focus’ on noisy outliers, hurting performance.

Note: We can keep adding more trees with every iteration; ideally, learning rate \(\nu\) is small, say 0.1, so that we do not overshoot and converge slowly.

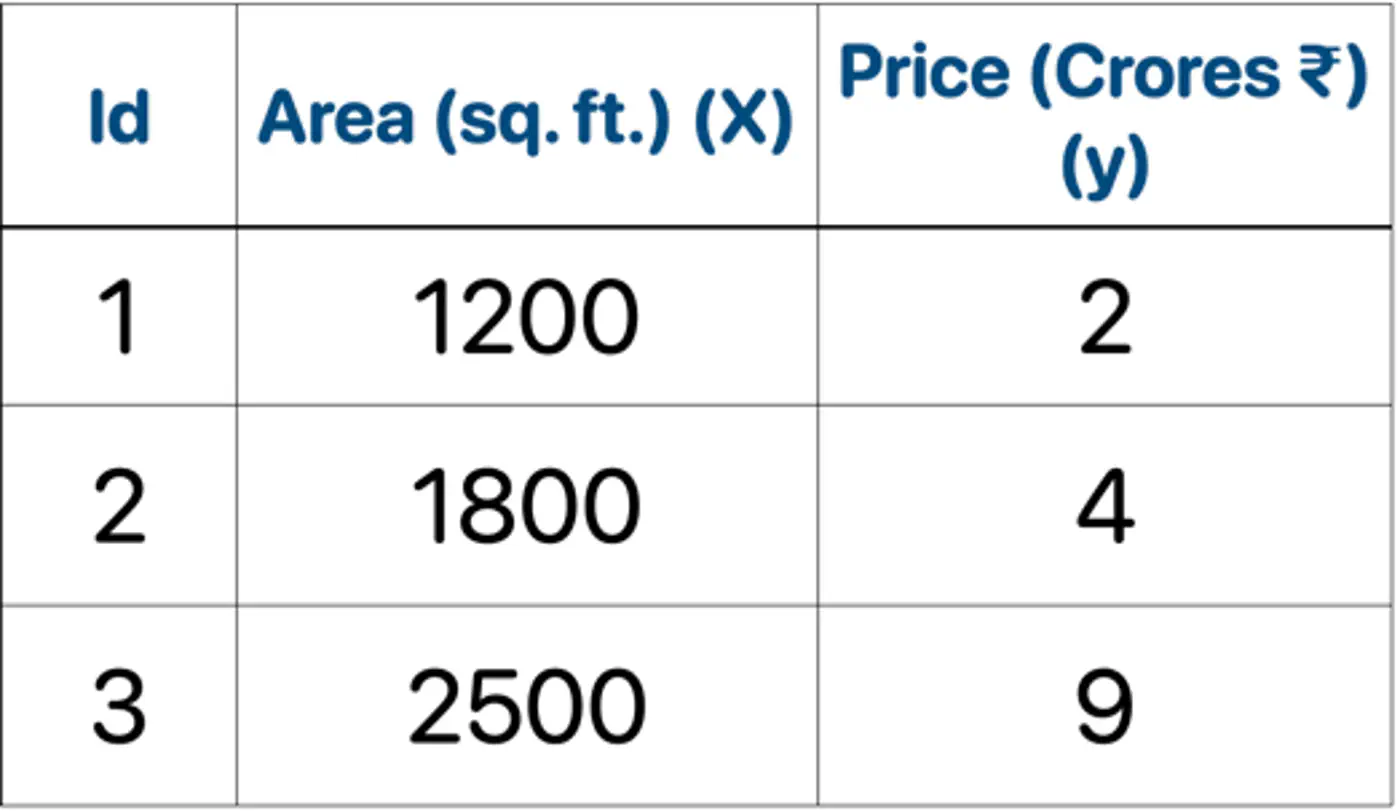

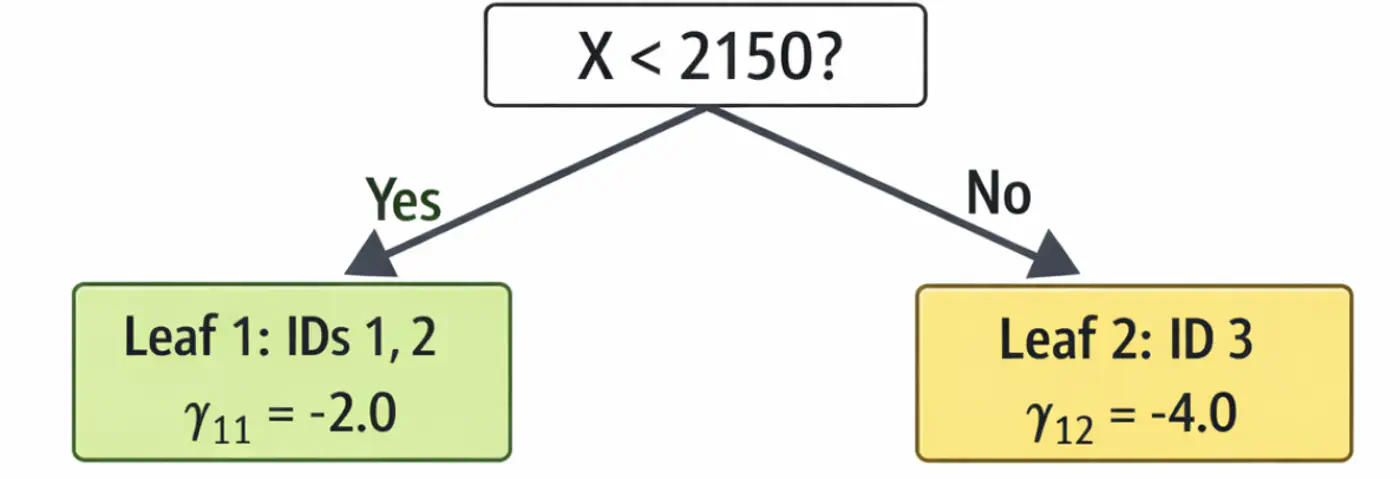

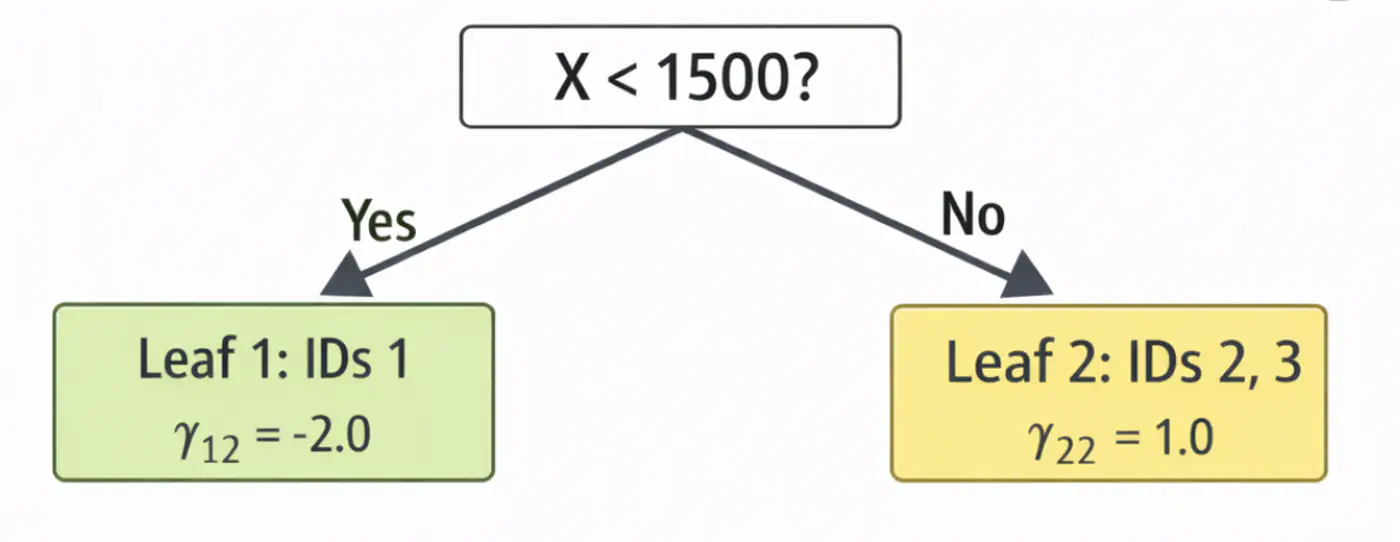

Let’s predict the price of a house with area = 2000 sq. ft.

\(F_{0}=5.0\)

Pass though tree 1 (\(h_1\)): is 2000 < 2150 ? Yes, \(\gamma_{11}\)= -2.0

Contribution (\(h_1\)) = 0.5 x (-2.0) = -1.0

Pass though tree 2 (\(h_2\)): is 2000 < 1500 ? No, \(\gamma_{22}\) = 1.0

Contribution(\(h_2\)) = 0.5 x (1.0) = 0.5

Final prediction = 5.0 - 1.0 + 0.5 = 4.5

Therefore, the price of a house with area = 2000 sq. ft is Rs 4.5 crores, which is very close. In just 2 iterations, although with higher learning rate (\(\nu=0.5\)), we were able to get a fairly good estimate.

⭐️An optimized and highly efficient implementation of gradient boosting.

👉 Widely used in competitive data science (like Kaggle) due to its speed and performance.

Note: Research project developed by Tianqi Chen during his doctoral studies at the University of Washington.

LightGBM (Light Gradient Boosting Machine)

⭐️Developed by Microsoft, this framework is designed for high speed and efficiency with large datasets.

👉It grows trees leaf-wise rather than level-wise and uses Gradient-based One-Side Sampling (GOSS) to speed 🐇 up the finding of optimal split points.

CatBoost (Categorical Boosting)

⭐️Developed by Yandex, this algorithm is specifically optimized for handling ‘categorical’ features without requiring extensive preprocessing (such as, one-hot encoding).

⭐️An optimized and highly efficient implementation of gradient boosting.

👉 Widely used in competitive data science (like Kaggle) due to its speed and performance.

Note: Research project developed by Tianqi Chen during his doctoral studies at the University of Washington.

Algorithmic Optimizations

🔵 Second order Derivative 🔵 Regularization 🔵 Sparsity-Aware Split Finding

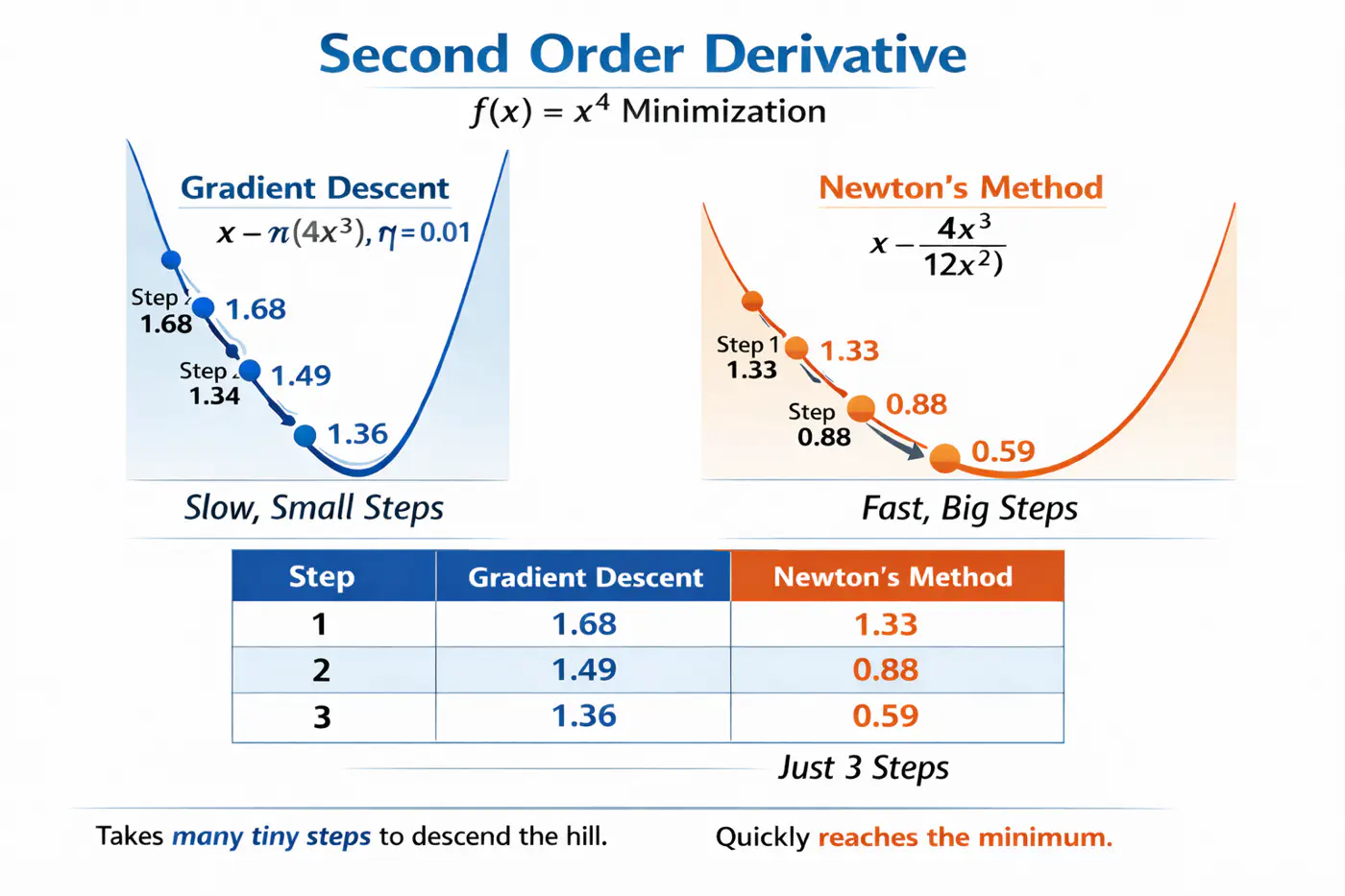

Second order Derivative

⭐️Uses second derivative (Hessian), i.e, curvature, in addition to first derivative (gradient) to optimize the objective function more quickly and accurately than GBDT.

Let’s understand this with the problem to minimize \(f(x) = x^4\), using:

Gradient descent (uses only 1st order derivative, \(f'(x) = 4x^3\))

Newton’s method (uses both 1st and 2nd order derivatives \(f''(x) = 12x^2\))

Regularization

Adds explicit regularization terms (L1/L2 on leaf weights and tree complexity) into the boosting objective, helping reduce over-fitting.

\[

\text{Objective} = \underbrace{\sum_{i=1}^{n} L(y_i, \hat{y}_i)}_{\text{Training Loss}} + \underbrace{\gamma T + \frac{1}{2}\lambda \sum_{j=1}^{T} w_j^2 + \alpha \sum_{j=1}^{T} |w_j|}_{\text{Regularization (The Tax)}}

\]

Sparsity-Aware Split Finding

💡Real-world data often contains many missing values or zero-entries (sparse data).

👉 XGBoost introduces a ‘default direction’ for each node.

➡️During training, it learns the best direction (left or right) for missing values to go, making it significantly faster and more robust when dealing with sparse or missing data.

⭐️Developed by Microsoft, this framework is designed for high speed and efficiency with large datasets.

👉It grows trees leaf-wise rather than level-wise and uses Gradient-based One-Side Sampling (GOSS) to speed 🐇 up the finding of optimal split points.

Algorithmic Optimizations

🔵 Gradient-based One Side Sampling (GOSS) 🔵 Exclusive Feature Bundling (EFB) 🔵 Leaf-wise Tree Growth Strategy

Gradient-based One Side Sampling (GOSS)

❌ Traditional GBDT uses all data instances for gradient calculation, which is inefficient.

✅ GOSS focuses 🔬on instances with larger gradients (those that are less well-learned or have higher error).

🐛 Keeps all instances with large gradients but randomly samples from those with small gradients.

🦩This way, it prioritizes the most informative examples for training, significantly reducing the data used and speeding up 🐇 the process while maintaining accuracy.

Exclusive Feature Bundling (EFB)

🦀 High-dimensional data often contains many sparse, mutually exclusive features (features that never take a non-zero value simultaneously, such as, One Hot Encoding (OHE)).

💡 EFB bundles the non-overlapping features into a single, dense feature, reducing the number of features, without losing much information, saving computation.

Leaf-wise Tree Growth Strategy

❌ Traditional gradient boosting machines (like XGBoost), the trees are built level-wise (BFS-like), meaning all nodes at the current level are split before moving to the next level.

✅ LightGBM maintains a set of all potential leaves that can be split at any given time and selects the leaf (for splitting) that provides the maximum gain across the entire tree, regardless of its depth.

⭐️Developed by Yandex, this algorithm is specifically optimized for handling ‘categorical’ features without requiring extensive preprocessing (such as, one-hot encoding).

❌ Standard target encoding can lead to target leakage, where the model uses information from the target variable during training that would not be available during inference. 👉(model ‘cheats’ by using a row’s own label to predict itself).

✅ CatBoost calculates the target statistics (average target value) for each category based only on the

history of previous training examples in a random permutation of the data.

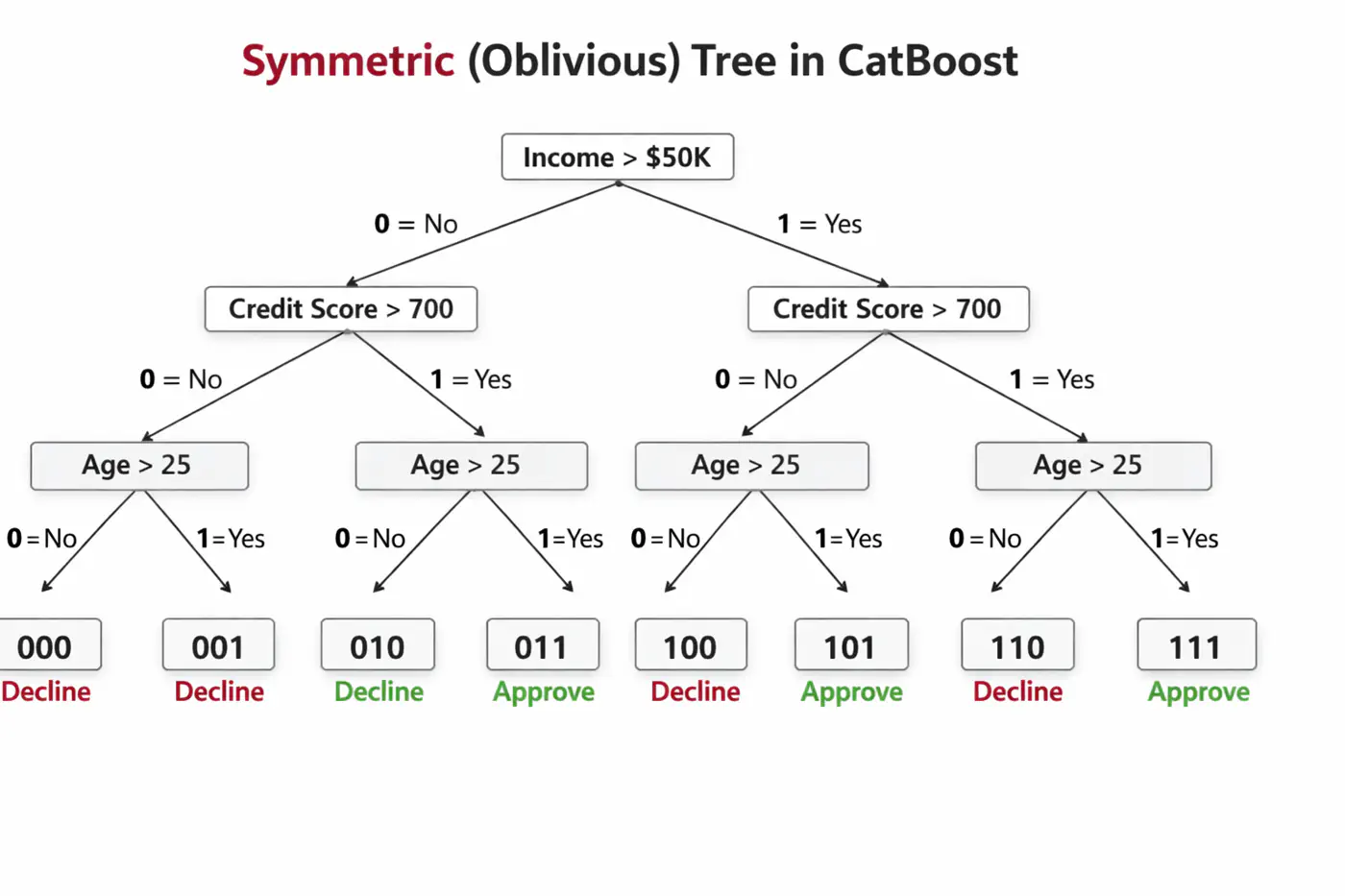

Symmetric (Oblivious) Trees

🦋 Uses symmetric decision trees by default. 👉 In symmetric trees, the same split condition is applied at each level across the entire tree structure.

🦘Does not walk down the tree using ‘if-else’ logic, instead it evaluates decision conditions to create a binary

index (e.g 101) and jumps directly to that leaf 🍃 in memory 🧠.

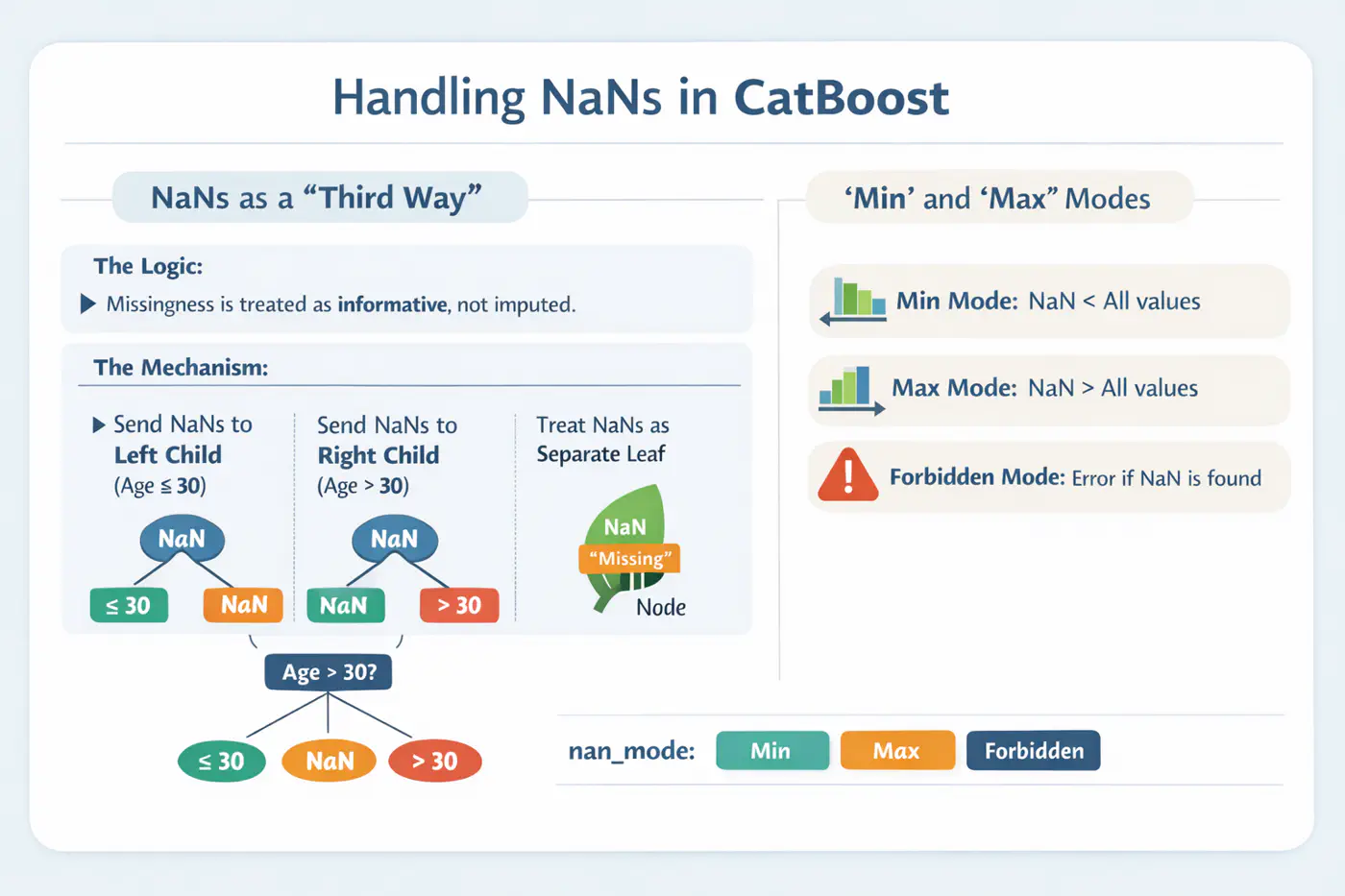

Handling Missing Values

⚙️ CatBoost offers built-in, intelligent handling of missing values and sparse features, which often require manual preprocessing in other GBDT libraries.

💡Treats ‘NaN’ as a distinct category, reducing the need for imputation.

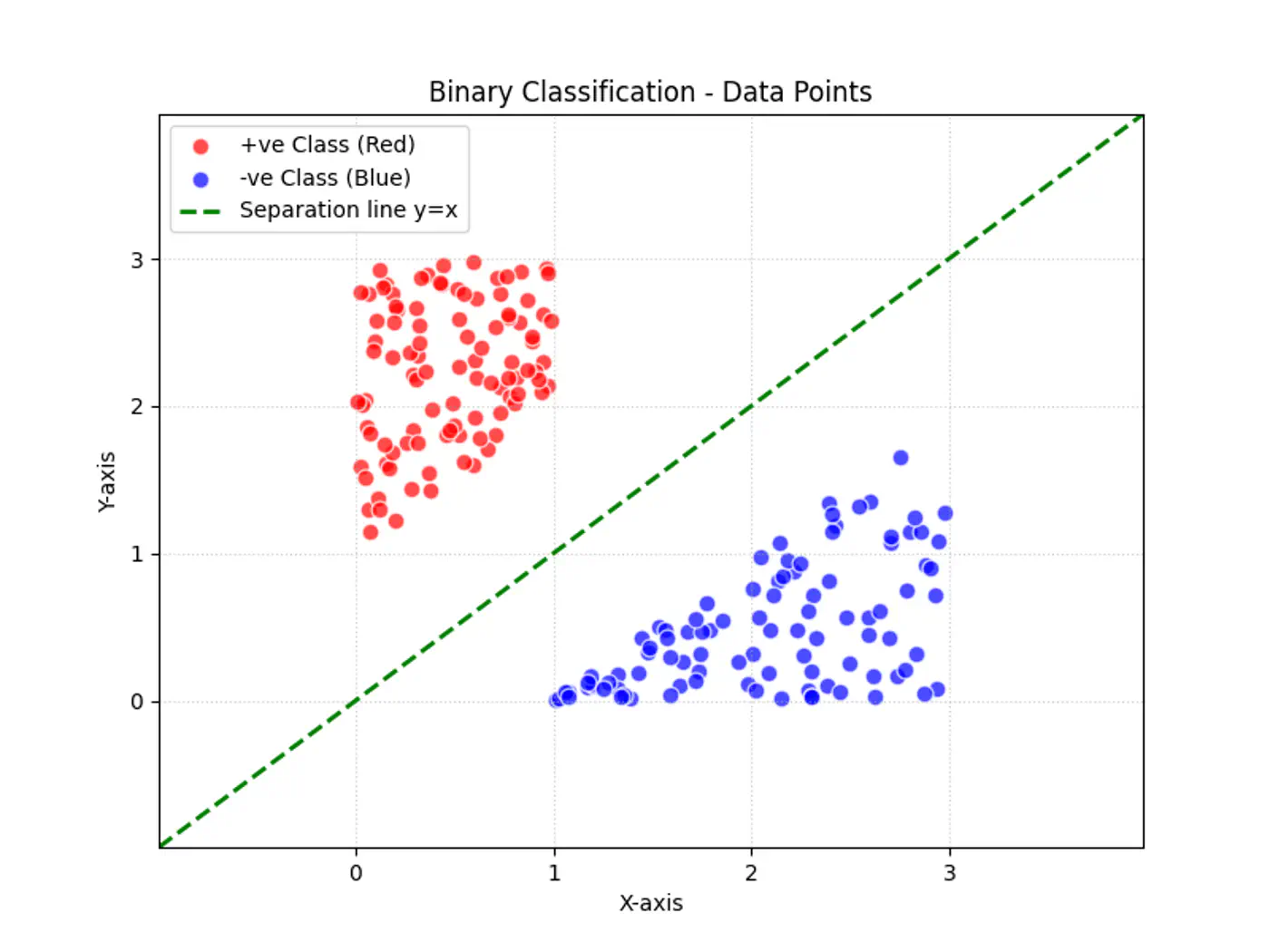

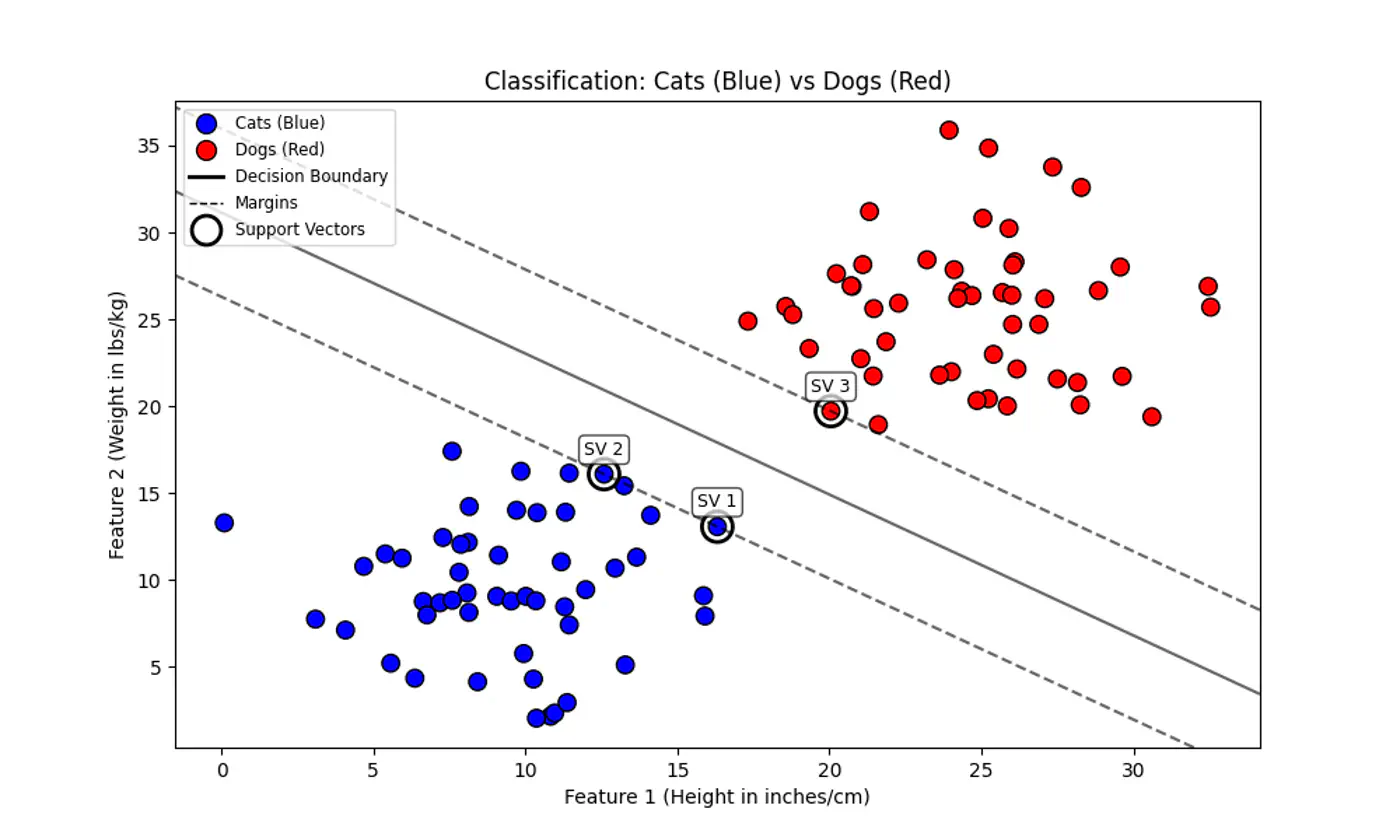

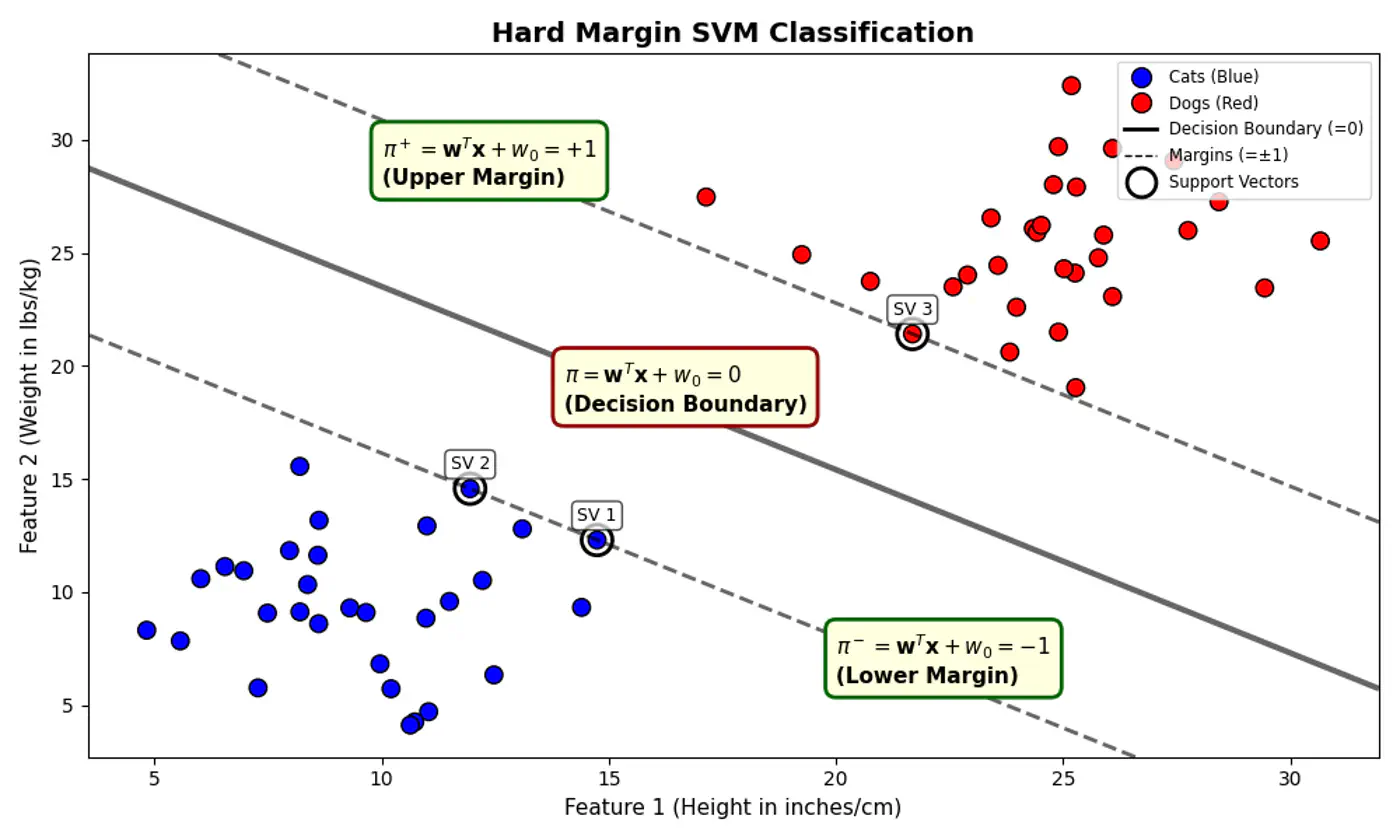

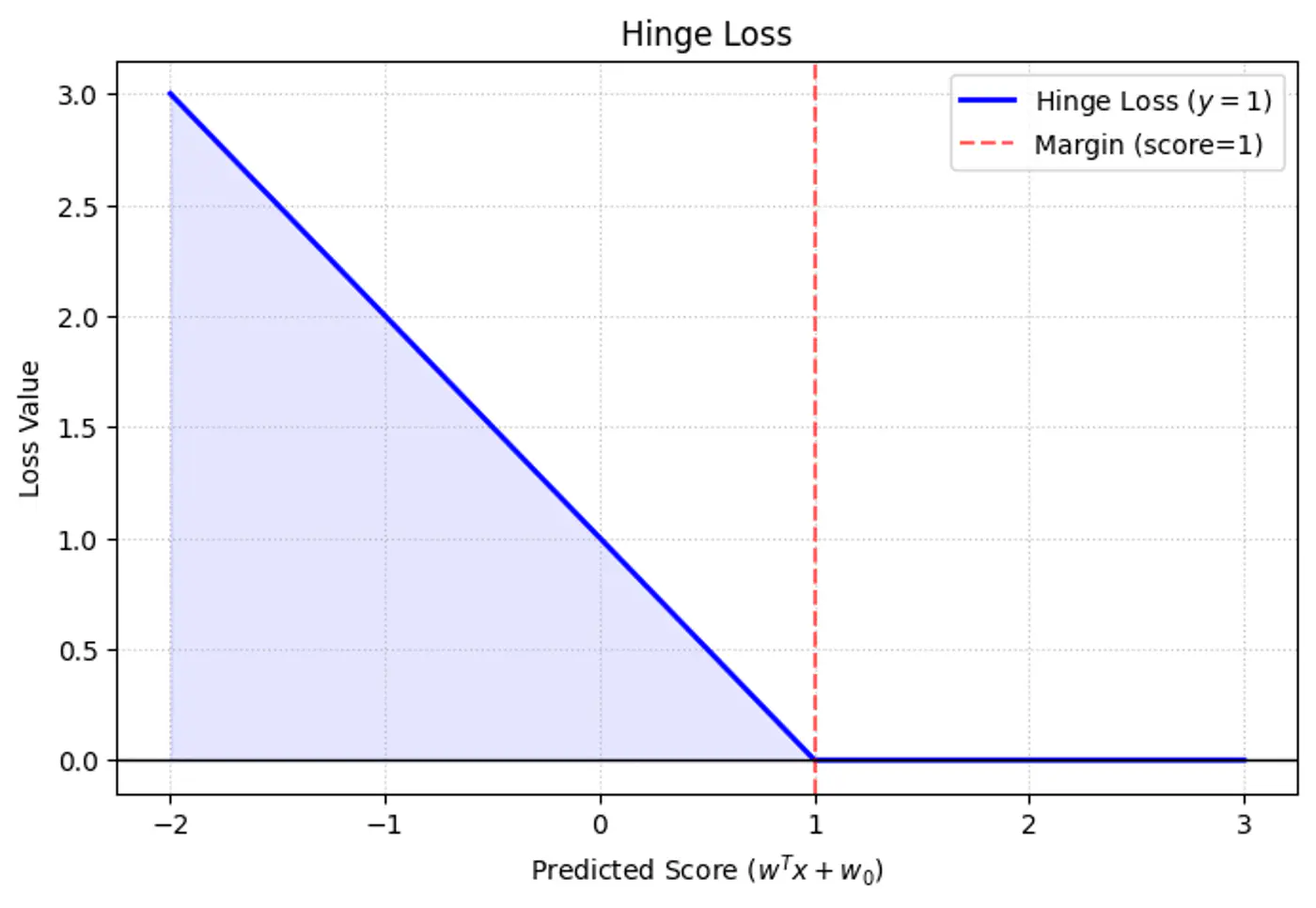

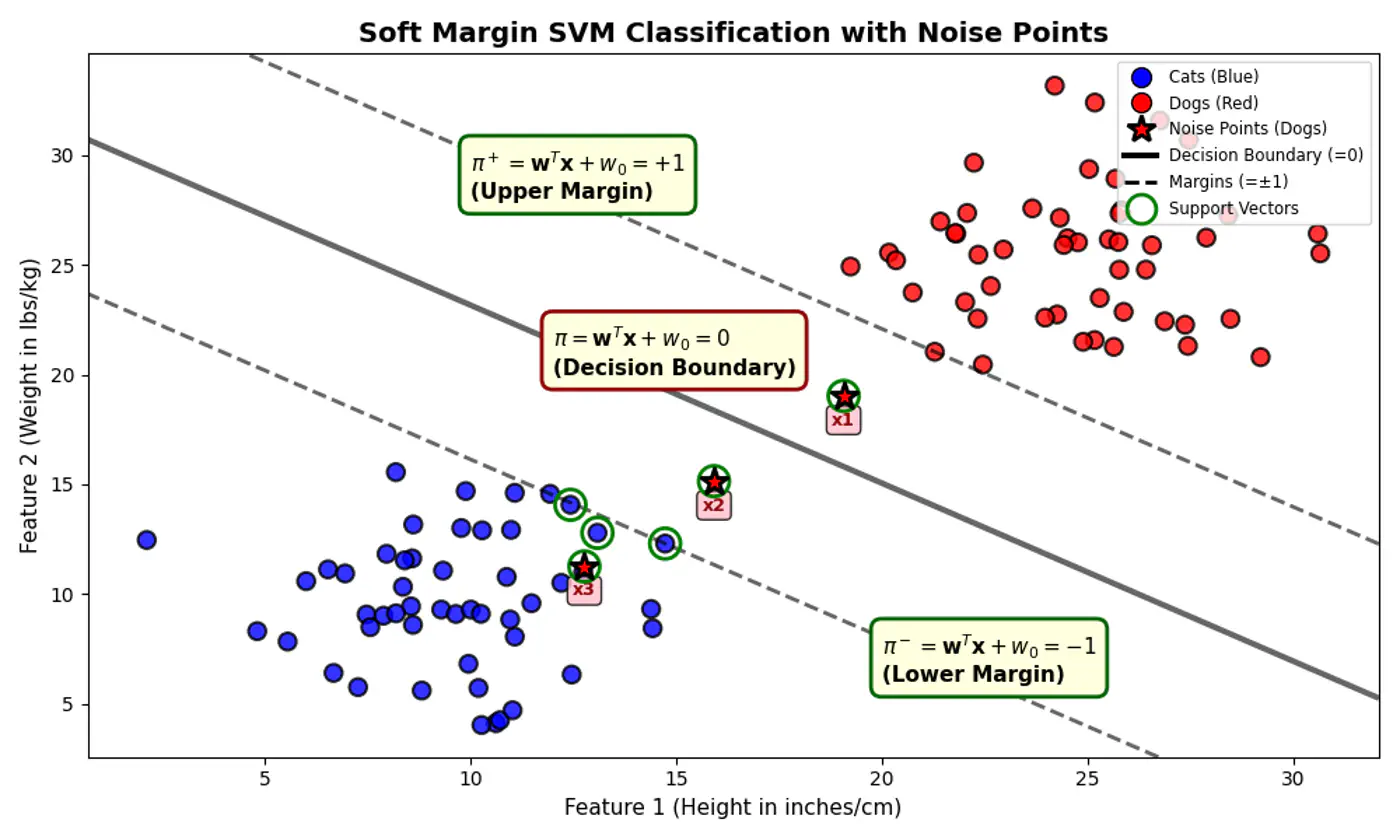

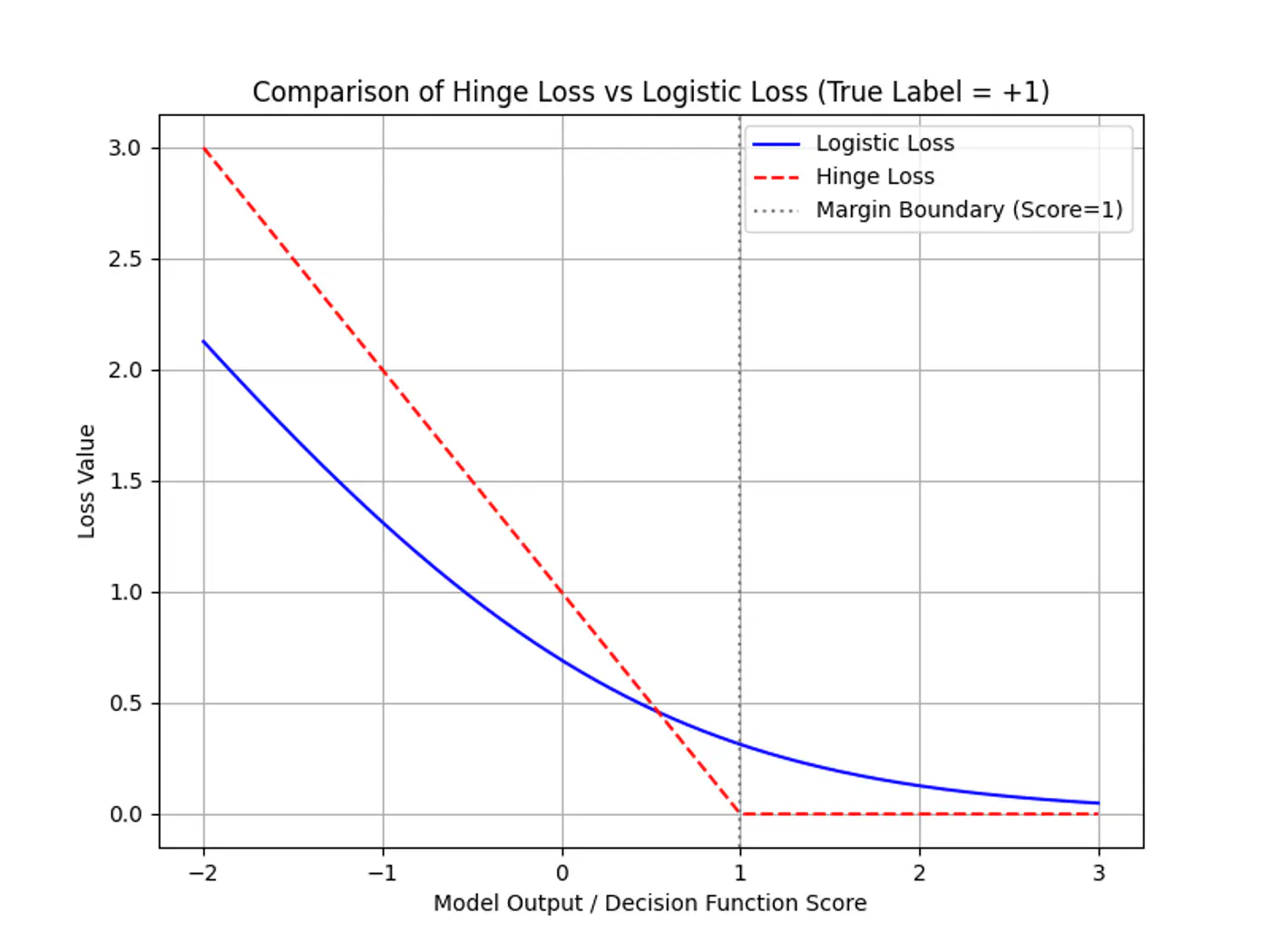

Data is perfectly linearly separable, i.e, there must exist a hyperplane that can perfectly separate the data into two distinct classes without any misclassification.

No noise or outliers that fall within the margin or on the wrong side of the decision boundary. Note: Even a single outlier can prevent the algorithm from finding a valid solution or drastically affect the boundary’s position, leading to poor generalization.

Hard Margin: fence is made of steel. Nothing can cross it.

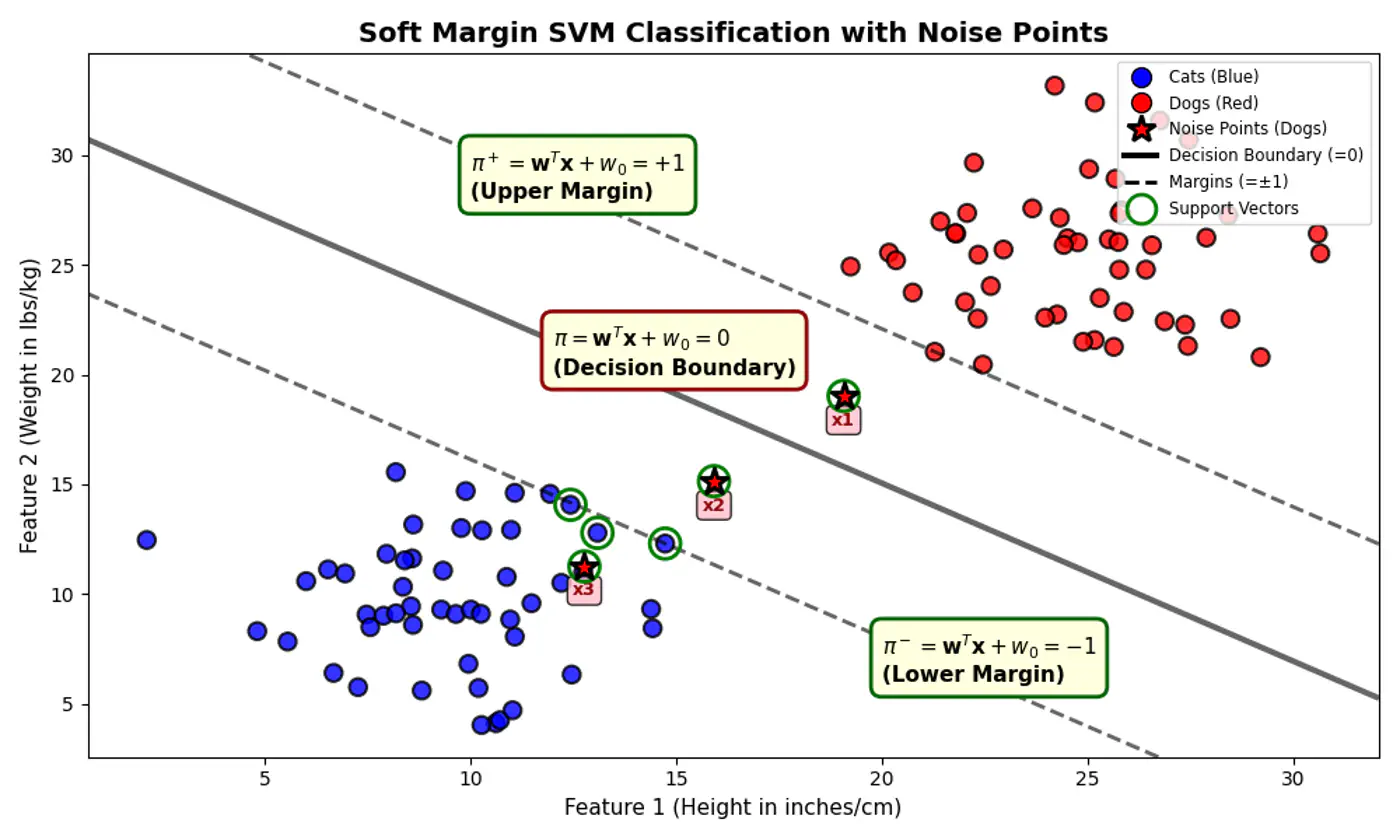

Soft Margin: fence is made of rubber(porous). Some points can ‘push’ into the margin or even cross over to the wrong side, but we charge them a penalty 💵 for doing so.

Issue

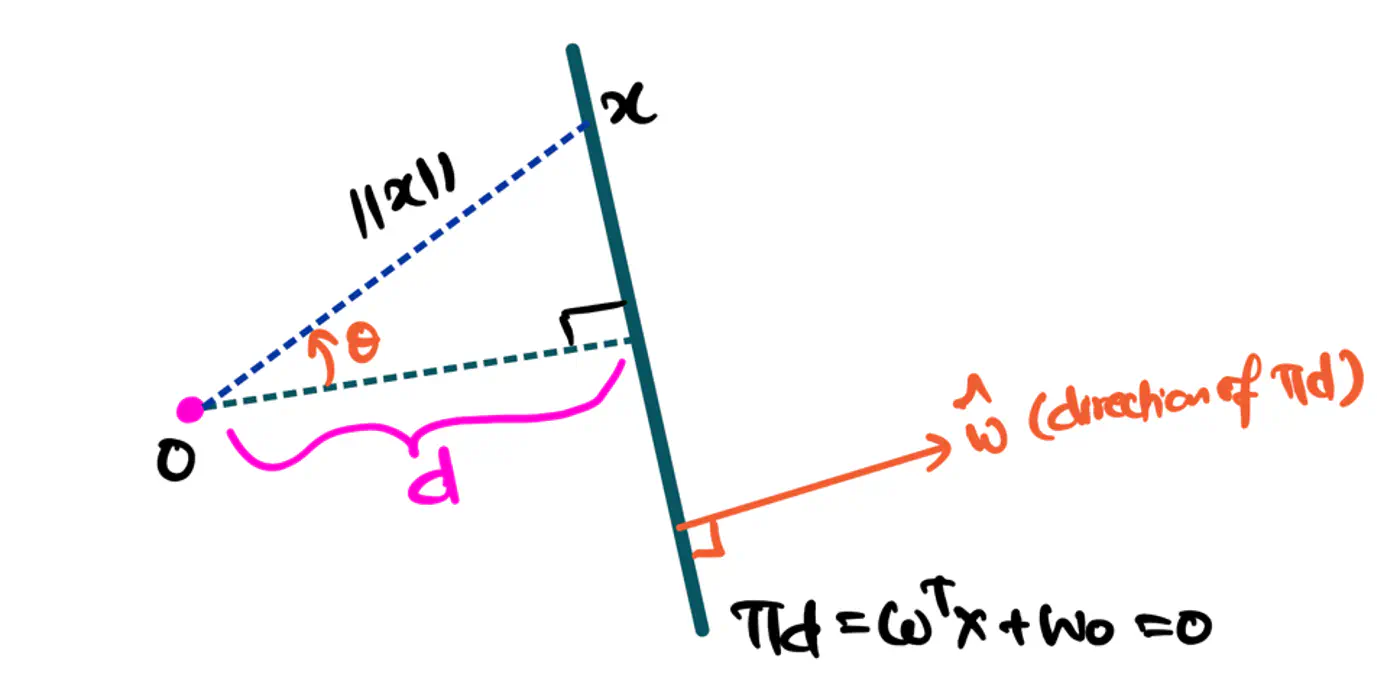

Distance from decision boundary:

Distance of positive labelled points must be \(\ge 1\)

Minimization: We want to minimize \(L(w, w_0, \xi, \alpha, \mu)\) w.r.t primal variables (\(w, w_0, \xi_i \) ) to find the hyperplane with the largest possible margin.

Maximization: We want to maximize \(L(w, w_0, \xi, \alpha, \mu)\) w.r.t dual variables (\(\alpha_i, \mu_i\) ) to ensure all training constraints are satisfied.

Note: A point that is simultaneously a minimum for one set of variables and a maximum for another is, by definition,

a saddle point.

Karush–Kuhn–Tucker (KKT) Conditions

👉To find the Dual, we find the saddle point by taking partial derivatives with respect to the primal variables \((w, w_0, \xi)\)

and equating them to 0.

Note: Even if you have 1 million training points, if only 500 are support vectors, the summation only runs for 500 terms. All other points have \(\alpha_i = 0\) and vanish.

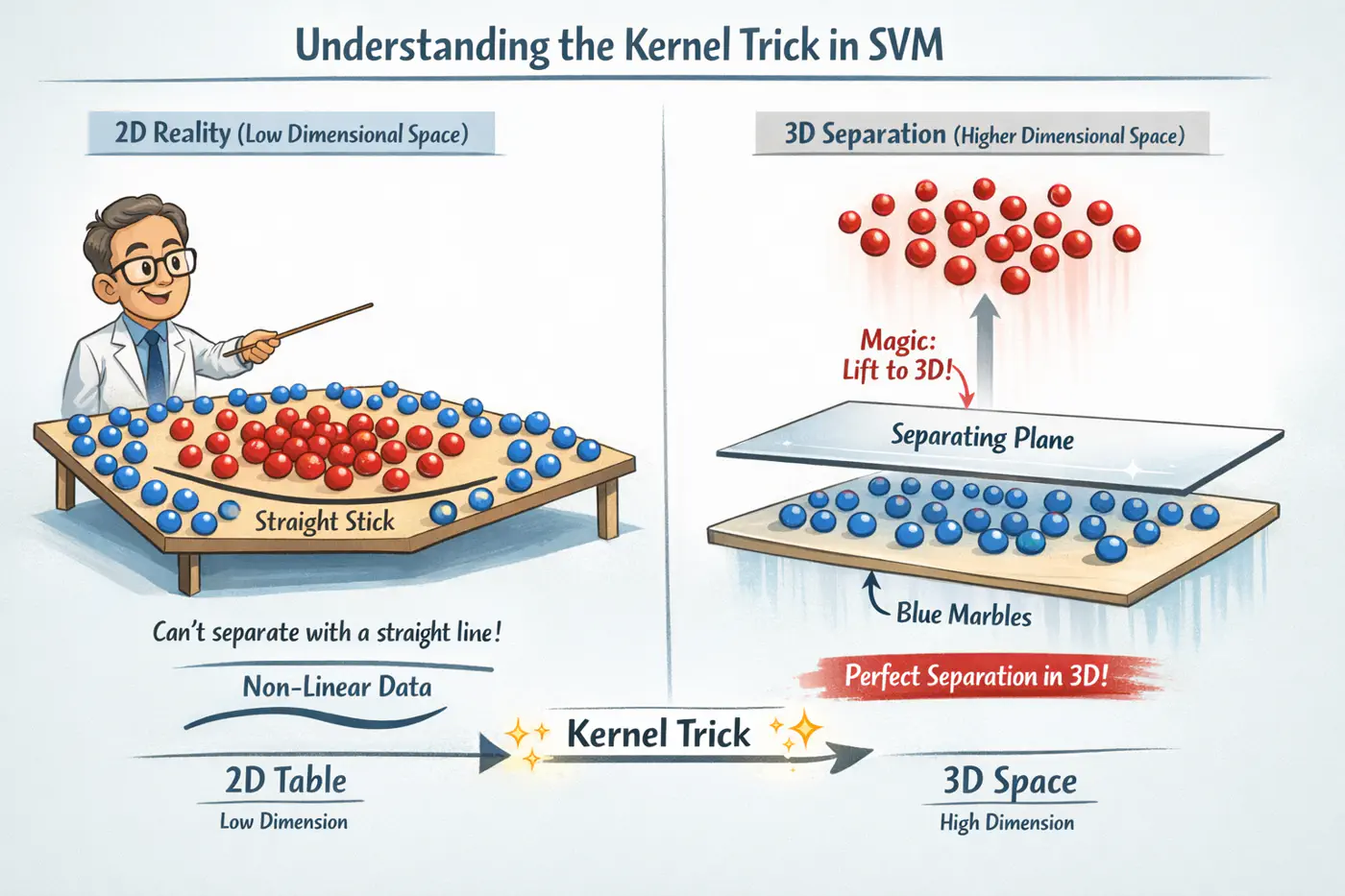

👉If our data is not linearly separable in its original space , we can map it to a higher-dimensional feature space

(where D»d) using a transformation function .

Kernel Trick 🪄

Bridge between Dual formulation and the geometry of high dimensional spaces.

It is a way to manipulate inner product spaces without the computational cost 💰 of explicit transformation.

👉The ‘shape’ of the decision boundary is entirely determined by how similar points are to one another, not by their absolute coordinates.

Non-Linear Separation

If our data is not linearly separable in its original space \(\mathbb{R}^d\), we can map it to a higher-dimensional

\(\mathbb{R}^D\) feature space (where D»d) using a transformation function \(\phi(x)\) .

Problem 🤔

If we choose a very high-dimensional mapping (e.g. \(D = 10^6\) or \(D = \infty\) ), calculating and then performing

the dot product \(\phi(x_i)^T \phi(x_j)\) becomes computationally impossible or extremely slow.

Kernel Trick 👻

So we define a function called ‘Kernel Function’.

The ‘Kernel Trick’ 🪄 is an optimization that replaces the dot product of a high-dimensional mapping with

a function of the dot product in the original space.

Instead of mapping (to higher dimension) \(x_i \rightarrow \phi(x_i)\), \(x_j \rightarrow \phi(x_j)\),

and calculating the dot product. We simply compute \(K(x_i, x_j)\) directly in the original input space.

👉The ‘Kernel Function’ gives the similar mathematical equivalent of mapping it to a higher dimensions and taking the dot product.

Note: For \(K(x_i, x_j)\) to be a valid kernel, it must satisfy Mercer’s Condition.

Polynomial (Quadratic) Kernel

Below is an example for a quadratic Kernel function in 2D that is equivalent to mapping the vectors

to 3D and taking a dot product in 3D.

Important: The tensor product \(x\otimes x\) creates a vector (or matrix) containing all combinations of the features.

e.g. if \(x=[x_{1},x_{2}]\), then \(x\otimes x=[x_{1}^{2},x_{1}x_{2},x_{2}x_{1},x_{2}^{2}]\)

Note: Because the Taylor series has an infinite number of terms, feature map has an infinite number of dimensions.

Bias-Variance Trade-Off ⚔️

High Gamma(low \(\sigma\)): Over-Fitting

Makes the kernel so ‘peaky’ that each support vector only influences its immediate neighborhood.

Decision boundary becomes highly irregular, ‘wrapping’ tightly around individual data points to ensure they are classified correctly.

Low Gamma(high \(\sigma\)): Under-Fitting

The Gaussian bumps are wide and flat.

Decision boundary becomes very smooth, essentially behaving more like a linear or low-degree polynomial classifier.

👉Imagine a ‘tube’ of radius \(\epsilon\) surrounding the regression line.

Points inside the tube are considered ‘correct’ and incur zero penalty.

Points outside the tube are penalized based on their distance from the tube’s boundary.

Ignore Errors

👉SVR ignores errors as long as they are within a certain distance (\(\epsilon\)) from the true value.

🎯This makes SVR inherently robust to noise and outliers, as it does not try to fit every single point perfectly,

only those that ‘matter’ to the structure of the data.

Note: Standard regression (like OLS) tries to minimize the squared error between the prediction and every data point.

➡️ For computing the joint distribution of say d=1000 words, we need to learn from possible \(2^{1000}\) combinations.

\(2^{1000}\) > the atoms in the observable 🔭 universe 🌌.

We will never have enough training data to see every possible combination of words even once.

Most combinations would have a count of zero.

🦉So, how do we solve this ?

Naive Assumption

💡The ‘Naive’ assumption is a ‘Conditional Independence’ assumption, i.e, we assume each word appears independently of the others, given the class Spam/Not Spam.

e.g. In a spam email, the likelihood of ‘Free’ and ‘Money’ 💵 appearing are treated as independent events, even though they usually appear together.

Note: The conditional independence assumption makes the probability calculations easier, i.e, the joint probability

simply becomes the product of individual probabilities, conditional on the label.

We can generalize it for any number of class labels ‘y’:

\[\implies P(y|W) \propto \prod_{i=1}^d P(w_i|y)\times P(y) \quad \text{ where, y = class label} \]\[ P(w_i|y) = \frac{count(w_i ~in~ y)}{\text{total words in class y}} \]

Note: We compute the probabilities for both Spam/Not Spam and assign the final label to email, depending upon which probability is higher.

Note: Every point belongs to one and only one cluster.

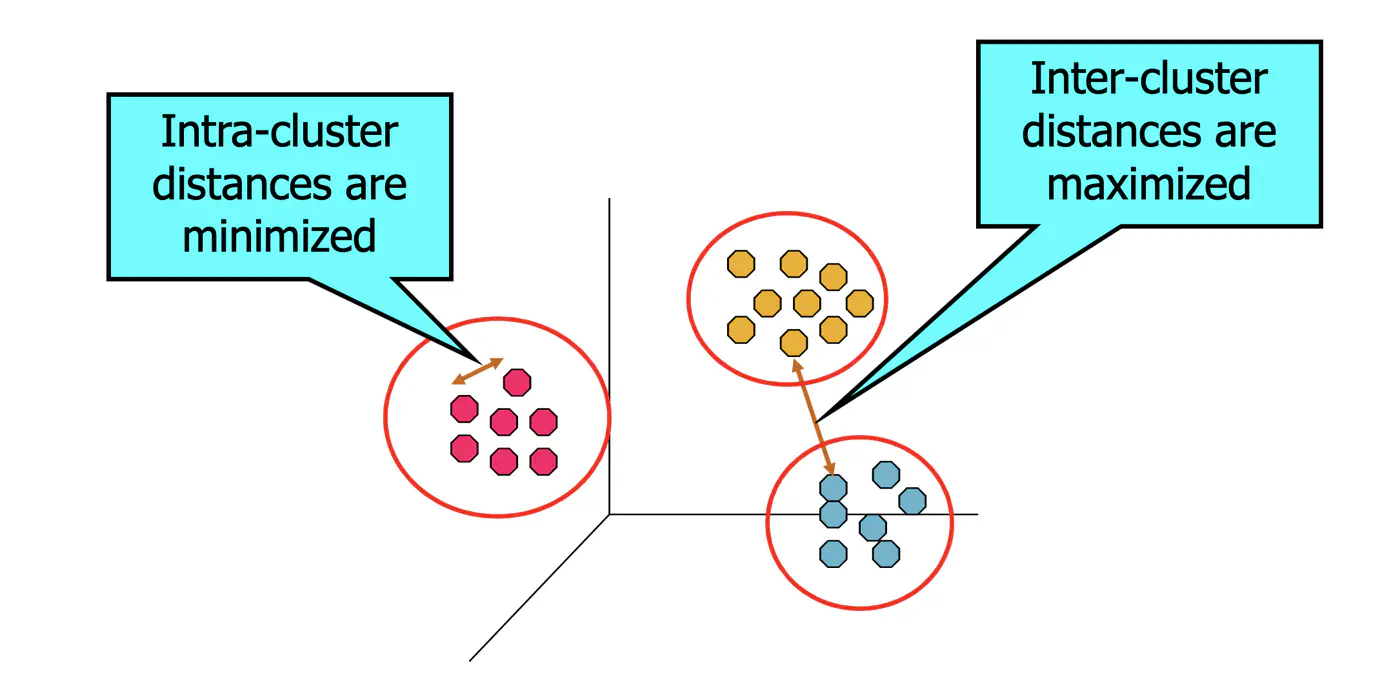

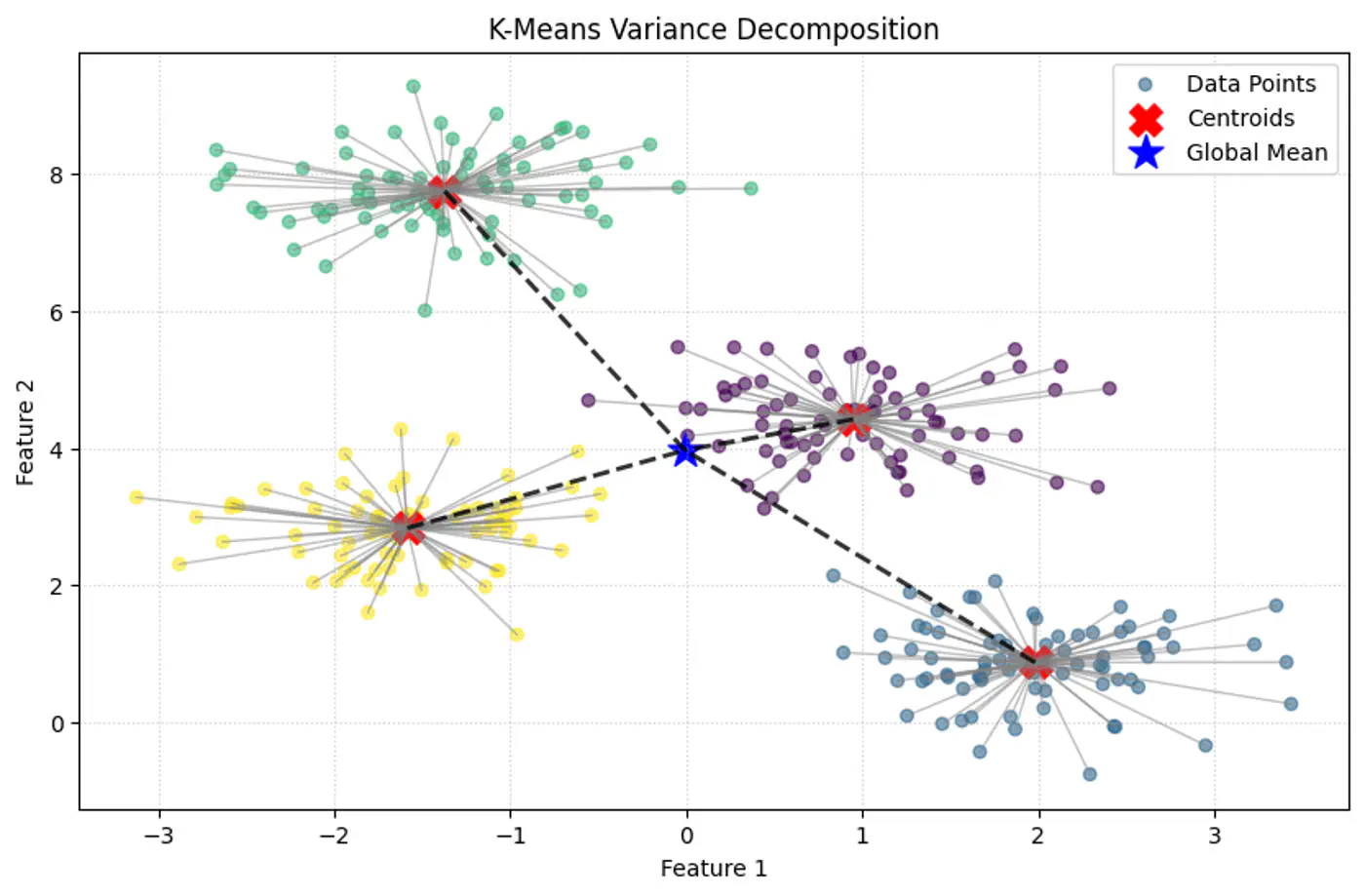

Variance Decomposition

💡Within-Cluster Sum of Squares (WCSS) is nothing but variance.

⭐️ Total Variance = Within-Cluster Variance + Between-Cluster Variance

👉K-Means minimizes within-Cluster variance, which implicitly maximizes between-cluster separation.

Geometric Interpretation:

Each point is ‘pulled’ toward its cluster center.

The objective measures total squared distance of all points to their centers.

Lower J(C, μ) means tighter, more compact clusters.

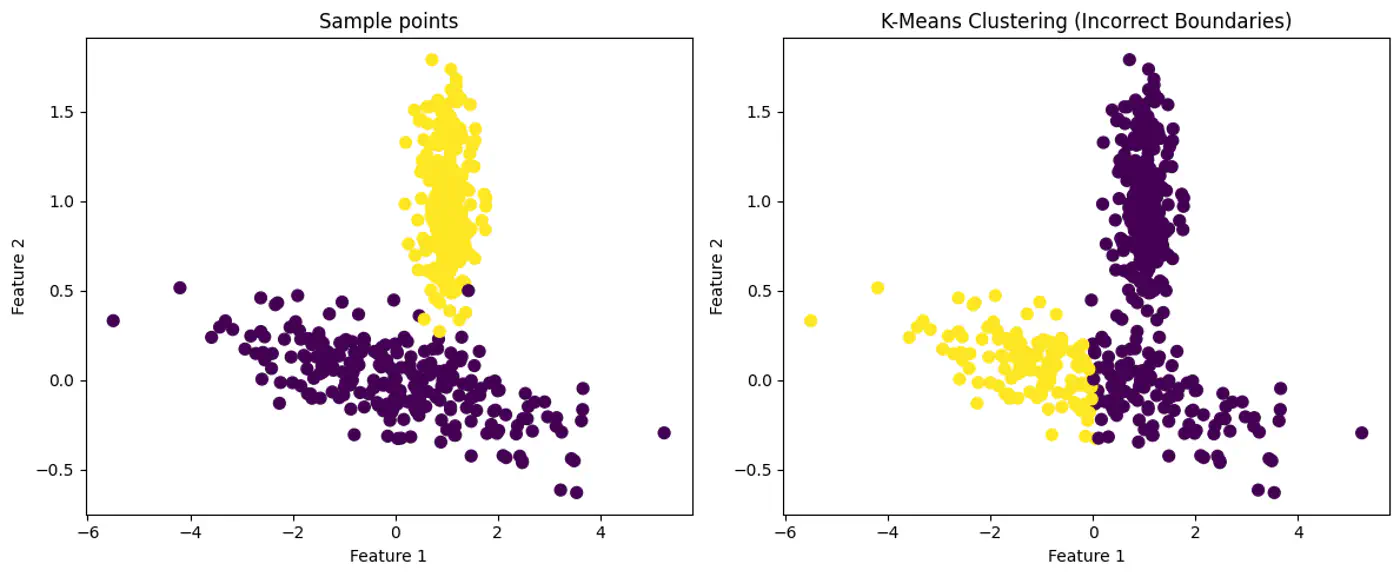

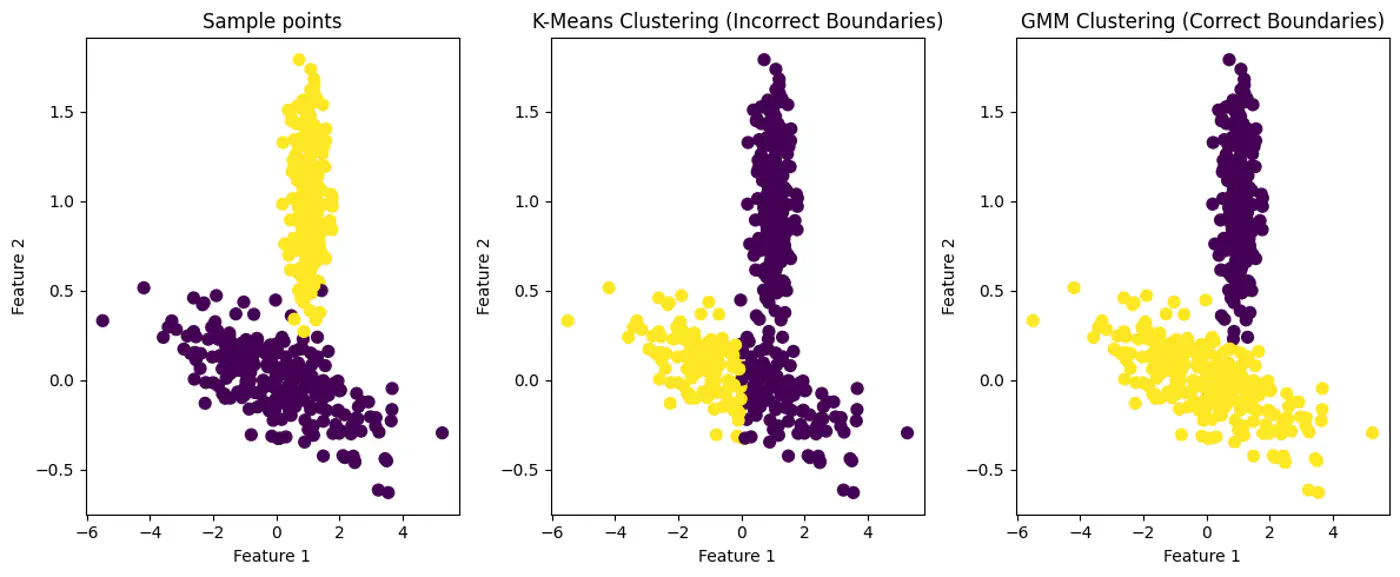

Note: K-Means works best when clusters are roughly spherical, similarly sized, and well-separated.

Combinatorial Explosion 💥

⭐️The problem requires partitioning ’n’ observations into ‘k’ distinct, non-overlapping clusters, which is given by

the Stirling number of the second kind, which grows at a rate roughly equal to \(k^n/k!\).

👉This large number of possible combinations makes the problem NP-Hard.

🦉The k-means optimization problem is NP-hard because it belongs to a class of problems for which no efficient

(polynomial-time ⏰) algorithm is known to exist.

Since, we cannot enumerate all partitions (i.e, partitioning ’n’ observations into ‘k’ distinct, non-overlapping clusters),

Lloyd’s algorithm provides a local search heuristic (approximate algorithm).

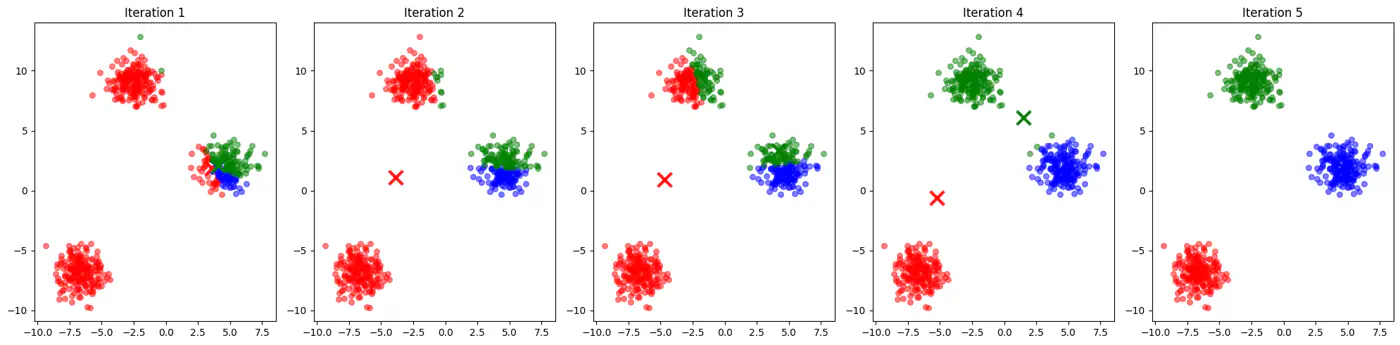

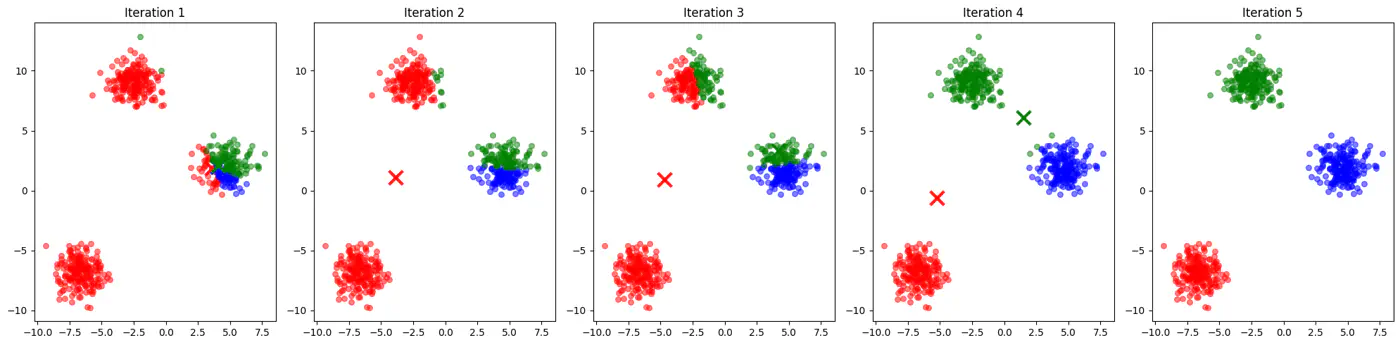

Lloyd's Algorithm ⚙️

Iterative method for partitioning ’n’ data points into ‘k’ groups by repeatedly assigning data points to the nearest centroid (mean) and then recalculating centroids until assignments stabilize, aiming to minimize within-cluster variance.

Repeat until convergence, i.e, until cluster assignments and centroids no longer change significantly.

a) Assignment: Assign each data point to the cluster whose centroid is closest (usually using Euclidean distance).

For each point xᵢ: cᵢ = argminⱼ ||xᵢ - μⱼ||²

b) Update: Recalculate the centroid (mean) of each cluster.

For each cluster j: μⱼ = (1/|Cⱼ|) Σₓᵢ∈Cⱼ xᵢ

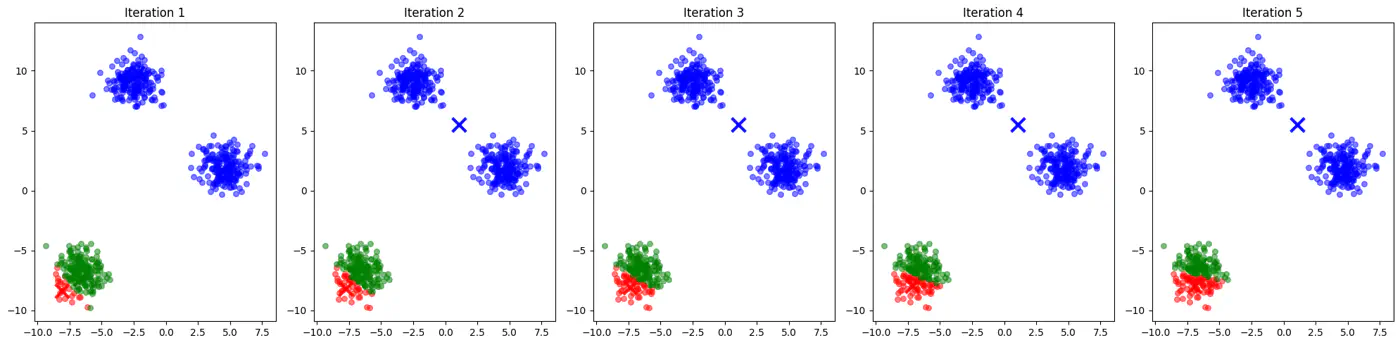

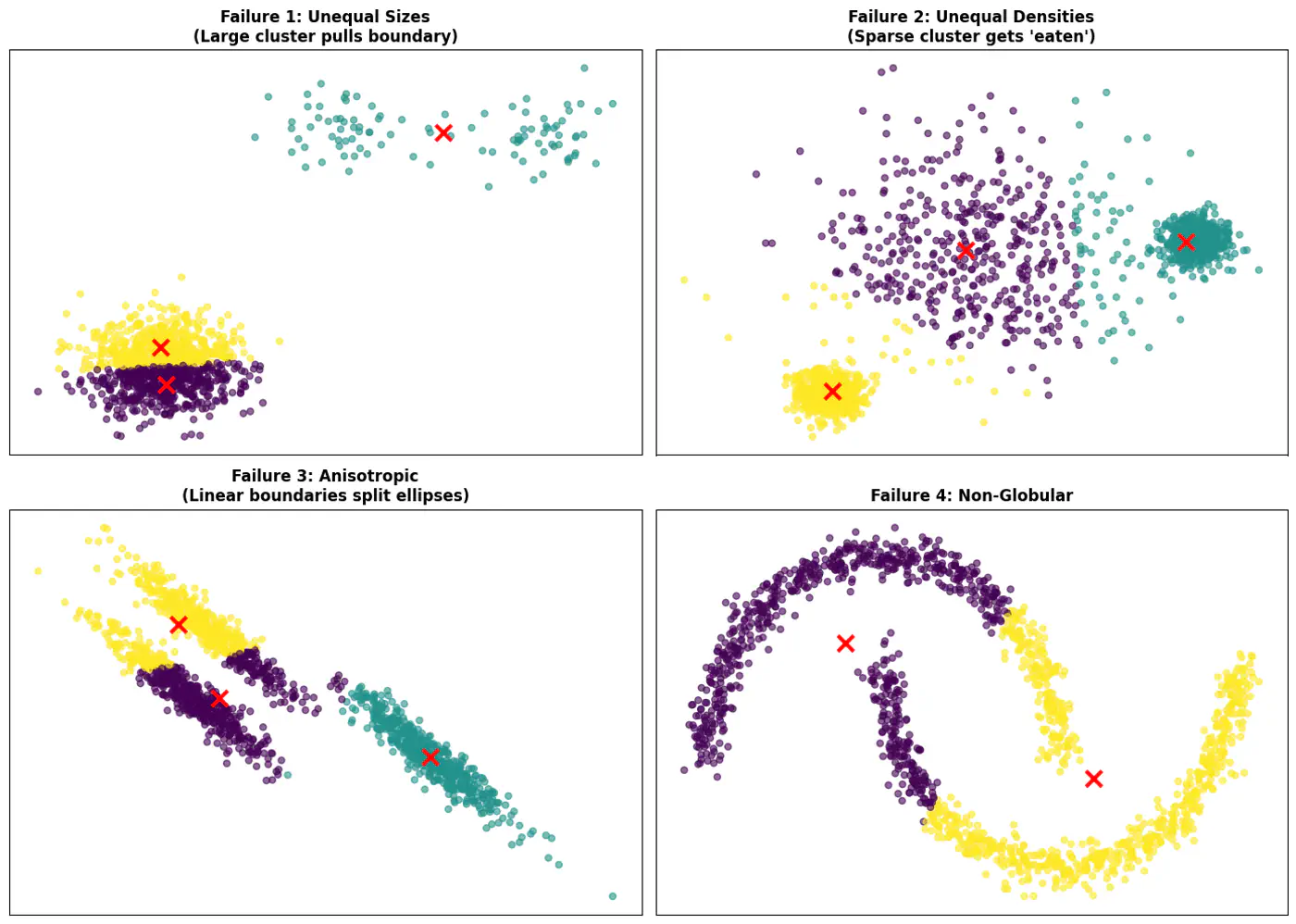

Issues🚨

Initialization sensitive, different initialization may lead to different clusters.

Tries to make each cluster of same size that may not be the case in real world.

Tries to make each cluster with same density(variance)

Does not work well with non-globular(spherical) data.

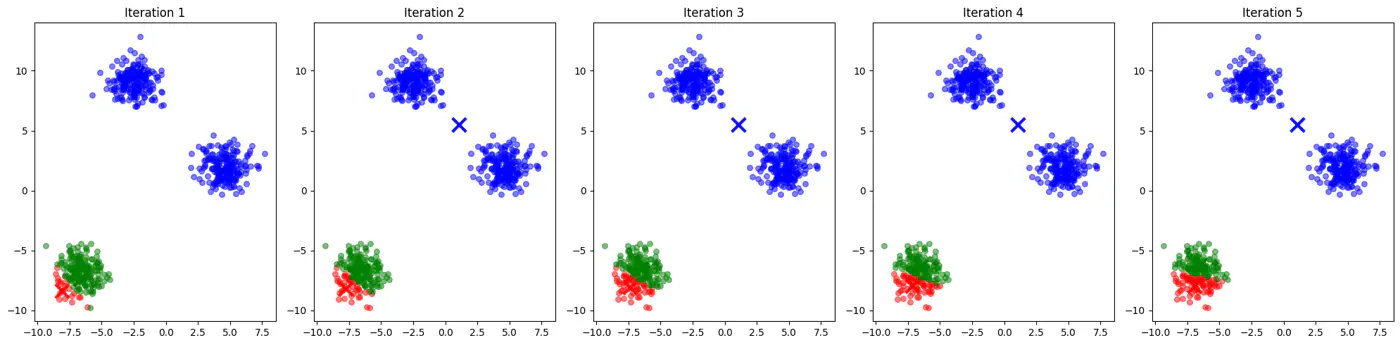

👉See how 2 different runs of K-Means algorithm gives totally different clusters.

👉Also, K-Means does not work well with non-spherical clusters, or clusters with different densities and sizes.

Solutions

✅ Do multiple runs 🏃♂️and choose the clustering with minimum error. ✅ Do not select initial points randomly, but some logic, such as, K-means++ algorithm. ✅ Use hierarchical clustering or density based clustering DBSCAN.

If two initial centroids belong to the same natural cluster, the algorithm will likely split that natural cluster in half and be forced to merge two other distinct clusters elsewhere to compensate.

Inconsistent; different runs may lead to different clusters.

Slow convergence; Centroids may need to travel much farther across the feature space, requiring more iterations.

👉Example for different K-Means algorithm runs give different clusters

K-Means++ Algorithm

💡Addresses the issue due to random initialization by aiming to spread out the initial centroids across the data points.

Steps:

Select the first centroid: Choose one data point randomly from the dataset to be the first centroid.

Calculate distances: For every data point x not yet selected as a centroid, calculate the distance, D(x), between x

and the nearest centroid chosen so far.

Select the next centroid: Choose the next centroid from the remaining data points with a probability

proportional to D(x)^2. This makes it more likely that a point far from existing centroids is selected, ensuring the initial centroids are well-dispersed.

Repeat: Repeat steps 2 and 3 until ‘k’ number of centroids are selected.

Run standard K-means: Once the initial centroids are chosen, the standard k-means algorithm proceeds with assigning

data points to the nearest centroid and iteratively updating the centroids until convergence.

Problem 🚨

🦀 If our data is extremely noisy (outliers), the probabilistic logic (\(\propto D(x)^2\)) might accidentally

pick an outlier as a cluster center.

Solution ✅

Do robust preprocessing to remove outliers or use K-Medoids algorithm.

In K-Means, the centroid is the arithmetic mean of the cluster. The mean is very sensitive to outliers.

Not interpretable; centroid is the mean of cluster data points and may not be an actual data point, hence not representative.

Medoid

⭐️Medoid is a specific data point from a dataset that acts as the ‘center’ or most representative member of its cluster.

👉It is defined as the object within a cluster whose average dissimilarity (distance) to all other members in that

same cluster is the smallest.

K-Medoids (PAM) Algorithm

💡Selects actual data points from the dataset as cluster representatives, called medoids (most centrally located).

👉a.k.a Partitioning Around Medoids(PAM).

Steps:

Initialization: Select ‘k’ data points from the dataset as the initial medoids using K-Means++ algorithm.

Assignment: Calculate the distance (e.g., Euclidean or Manhattan) from each non-medoid point to all medoids and assign each point to the cluster of its nearest medoid.

Update (Swap):

For each cluster, swap current medoid with a non-medoid point from the same cluster.

For each swap, calculate the total cost 💰(sum of distances from medoid).

Pick the medoid with minimum cost 💰.

Repeat🔁: Repeat the assignment and update steps until (convergence), i.e, medoids no longer change or

a maximum number of iterations is reached.

Note: Kind of brute-force algorithm, computationally expensive for large dataset.

Advantages

✅ Robust to Outliers: Since medoids are actual data points rather than averages, extreme values (outliers)

do not skew the center of the cluster as they do in K-Means. ✅ Flexible Distance Metrics: It can work with any dissimilarity measure (Manhattan, Cosine similarity), making it ideal

for categorical or non-Euclidean data. ✅ Interpretable Results: Cluster centers are real observations (e.g., a ‘typical’ customer profile), which makes

the output easier to explain to stakeholders.

👉 Elbow Method: Quickest to compute; good for initial EDA (Exploratory Data Analysis).

👉 Dunn Index: Focuses on the ‘gap’ between the closest clusters.

👉 Silhouette Score: Balances compactness and separation.

👉 Domain specific knowledge and system constraints.

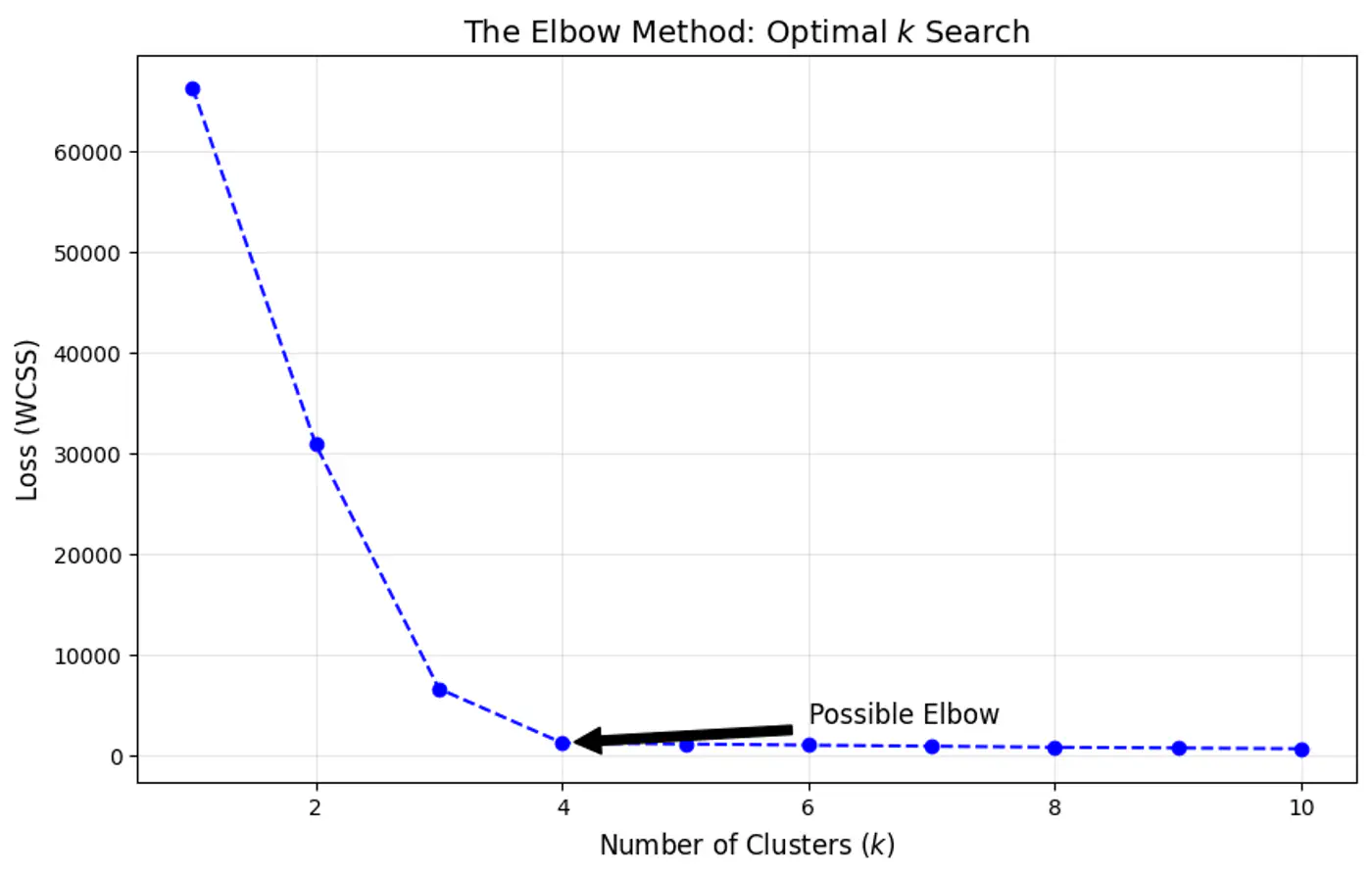

Elbow Method

⭐️Heuristic used to determine the optimal number of clusters (k) for clustering by visualizing how the

quality of clustering improves as ‘k’ increases.

🎯The goal is to find a value of ‘k’ where adding more clusters provides a diminishing return in terms of variance reduction.

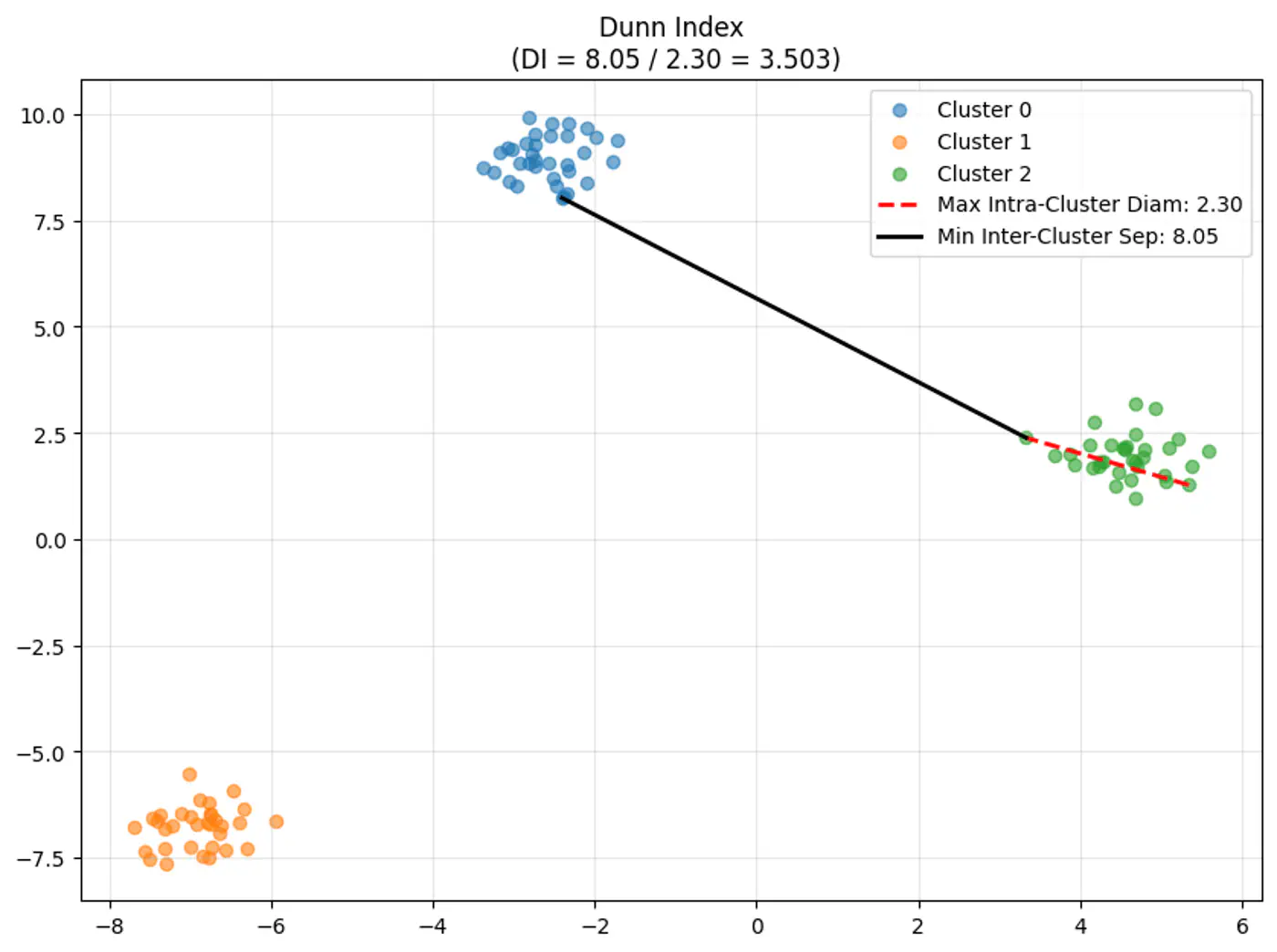

Dunn Index [0, \(\infty\))

⭐️Clustering quality evaluation metric that measures: separation (between clusters) and compactness (within clusters)

Note: A higher Dunn Index value indicates better clustering, meaning clusters are well-separated from each other and compact.

👉Dunn Index Formula:

\[DI = \frac{\text{Minimum Inter-Cluster Distance(between different clusters)}}{\text{Maximum Intra-Cluster Distance(within a cluster)}}\]\[DI = \frac{\min_{1 \le i < j \le k} \delta(C_i, C_j)}{\max_{1 \le l \le k} \Delta(C_l)}\]

👉Let’s understand the terms in the above formula:

\(\delta(C_i, C_j)\) (Inter-Cluster Distance):

Measures how ‘far apart’ the clusters are.

Distance between the two closest points of different clusters (Single-Linkage distance).

\[\delta(C_i, C_j) = \min_{x \in C_i, y \in C_j} d(x, y)\]

\(\Delta(C_l)\) (Intra-Cluster Diameter):

Measures how ‘spread out’ a cluster is.

Distance between the two furthest points within the same cluster (Complete-Linkage distance).

\[\Delta(C_l) = \max_{x, y \in C_l} d(x, y)\]

Measure of Closeness

Single Linkage (MIN): Uses the minimum distance between any two points in different clusters.

Complete Linkage (MAX): Uses the maximum distance between any two points in same cluster.

✅ Elbow Method: Quickest to compute; good for initial EDA.

✅ Dunn Index: Focuses on the ‘gap’ between the closest clusters. ——- We have seen the above 2 methods in the previous section ———-

👉 Silhouette Score: Balances compactness and separation.

👉 Domain specific knowledge and system constraints.

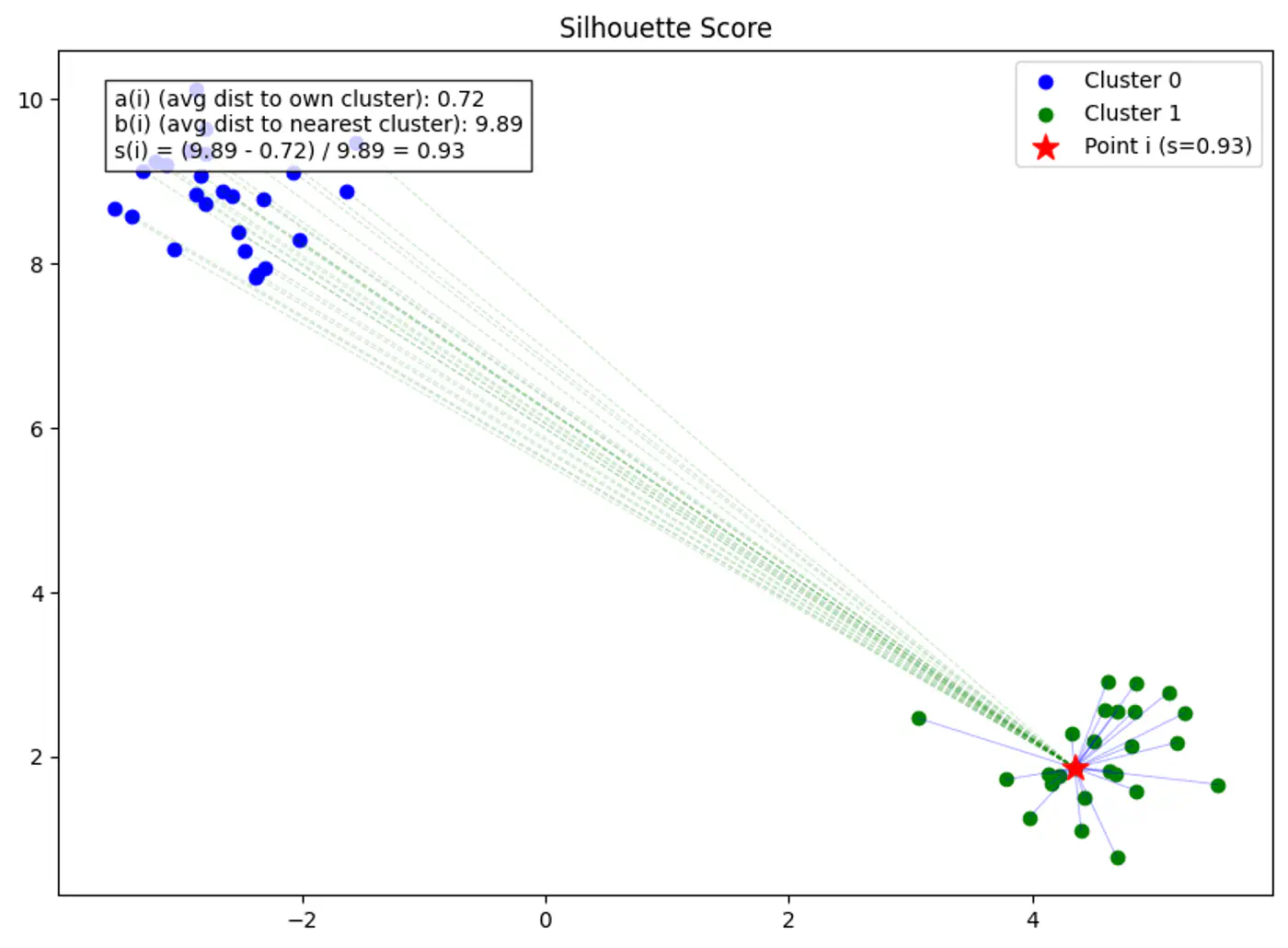

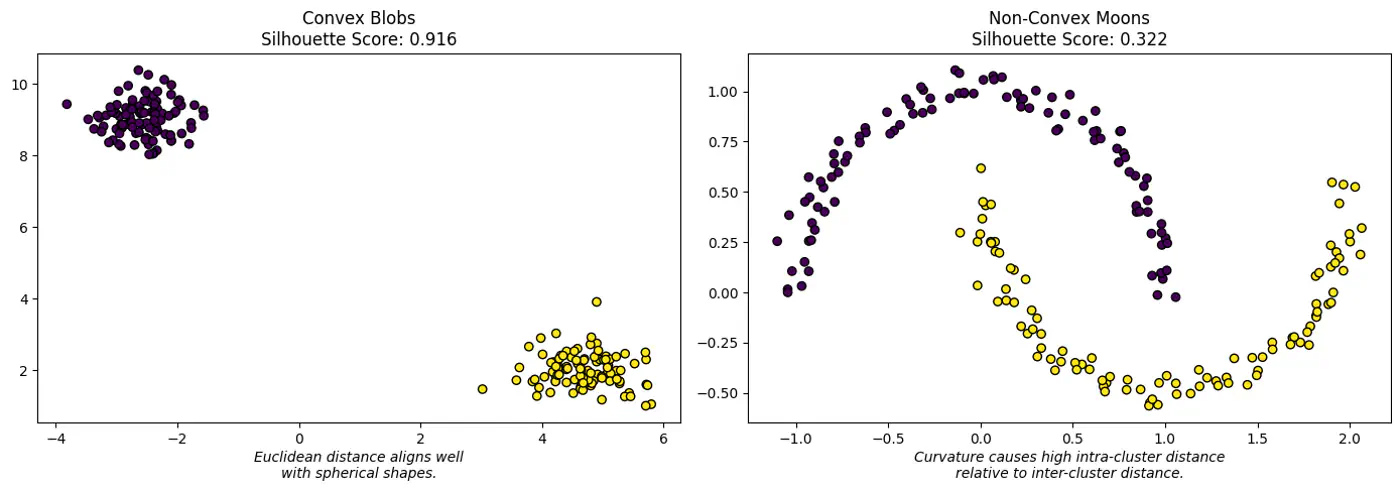

Silhouette Score [-1, 1]

⭐️Clustering quality evaluation metric that measures how similar a data point is to its own cluster (cohesion)

compared to other clusters (separation).

Note: Higher scores (closer to 1) indicate better-defined, distinct clusters, while scores near 0 suggest overlapping clusters, and negative scores mean points might be in the wrong cluster.

Silhouette Score Formula

Silhouette score for point ‘i’ is the difference between separation b(i) and cohesion a(i), normalized by the larger of the two.

\[ s(i) = \frac{b(i) - a(i)}{\max(a(i), b(i))} \]

Note: The Global Silhouette Score is simply the mean of s(i) for all points in the dataset.

👉Example for Silhouette Score:

👉Example for Silhouette Score of 0(Border Point) and negative(Wrong Cluster).

🦉Now let’s understand the terms in Silhouette Score in detail.

Cohesion a(i)

Average distance between point ‘i’ and all other points in the same cluster.

Note: Higher b(i) means the point is very far from the next closest cluster.

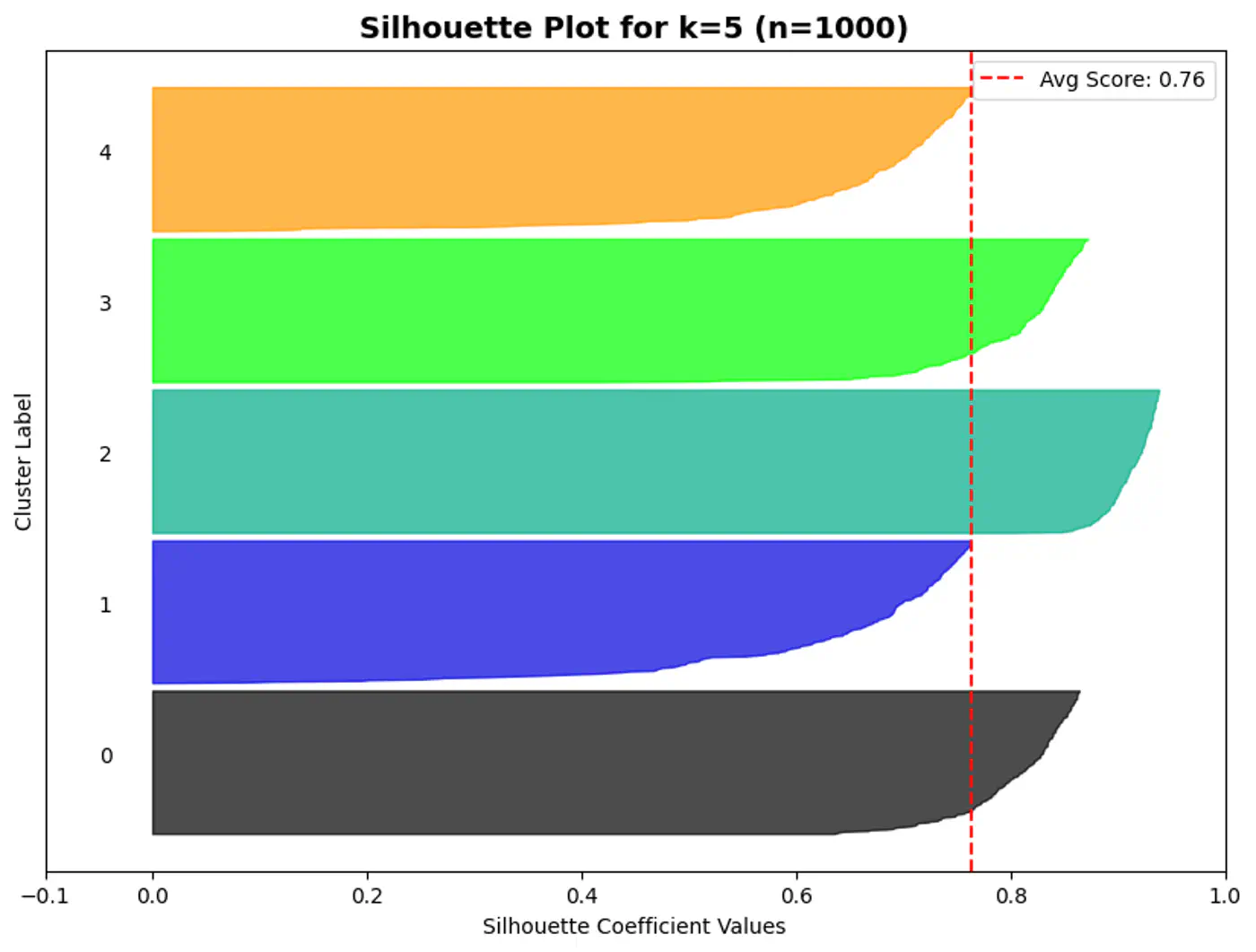

Silhouette Plot

⭐️A silhouette plot is a graphical tool used to evaluate the quality of clustering algorithms (like K-Means),

showing how well each data point fits within its cluster.

👉Each bar gives the average silhouette score of the points assigned to that cluster.

Geometric Interpretation

⛳️ Like K-Means, the Silhouette Score (when using Euclidean distance) assumes convex clusters.

🌘 If we use it on ‘Moon’ shaped clusters, it will give a low score even if the clusters are perfectly separated,

because the ‘average distance’ to a neighbor might be small due to the curvature of the manifold.

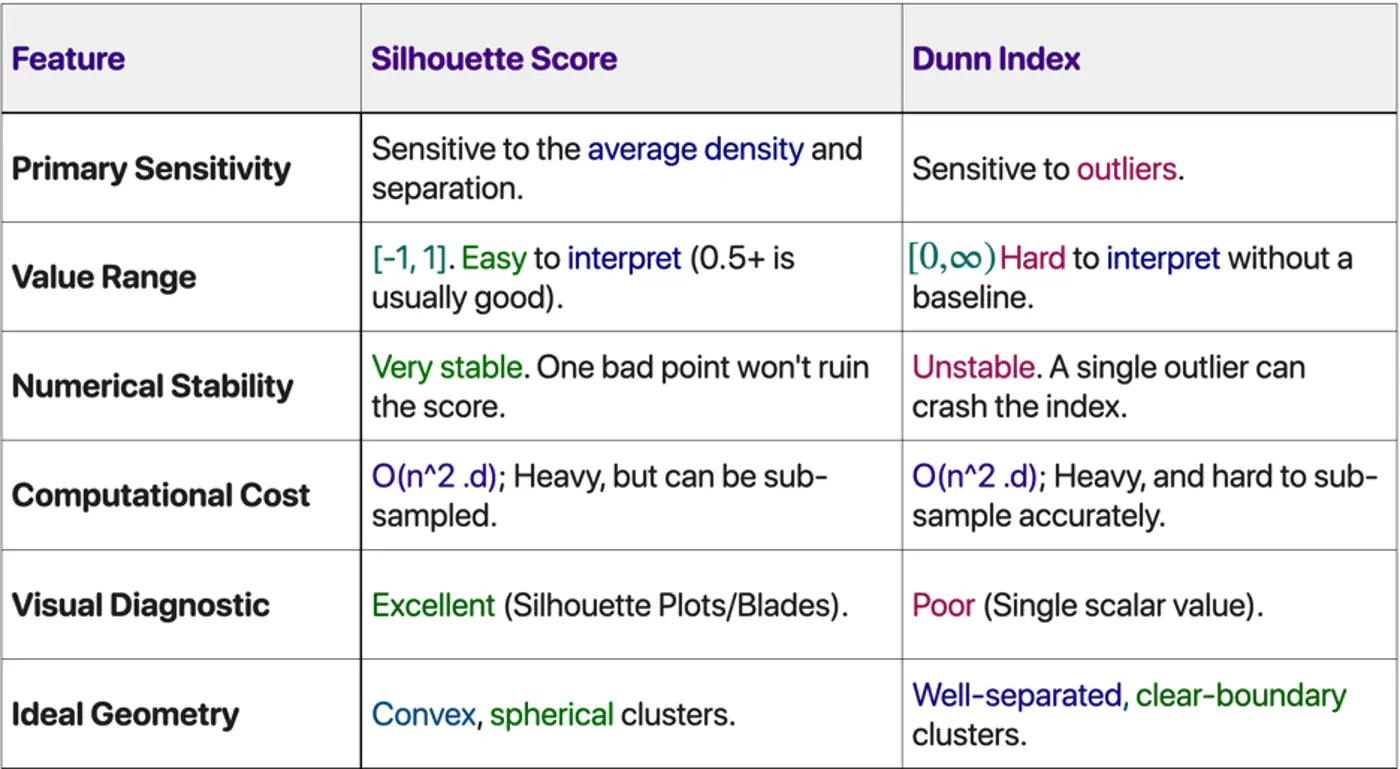

Silhouette Score Vs Dunn Index

Choose Silhouette Score if: ✅ Need a human-interpretable metric to present to stakeholders. ✅ Dealing with real-world noise and overlapping ‘fuzzy’ boundaries. ✅ Want to see which specific clusters are weak (using the plot).

Choose Dunn Index if: ✅ Performing ‘Hard Clustering’ where separation is a safety or business requirement. ✅ Data is pre-cleaned of outliers (e.g., in a curated embedding space). ✅ Need to compare different clustering algorithms (e.g., K-Means vs. DBSCAN) on a high-integrity task.

🤷 We might not know in advance the number of distinct clusters ‘k’ in the dataset.

🕸️ Also, sometimes the dataset may contain a nested structure or some inherent hierarchy, such as, file system,

organizational chart, biological lineages, etc.

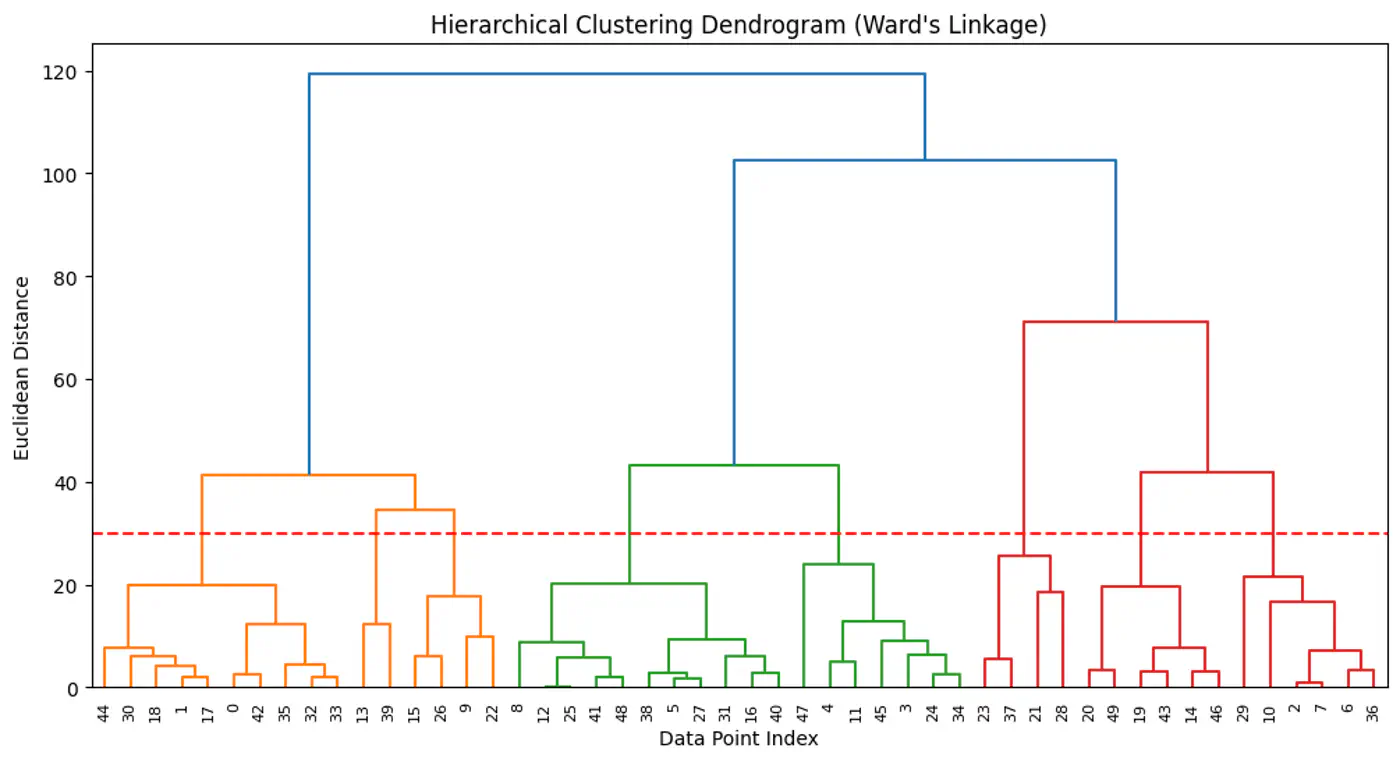

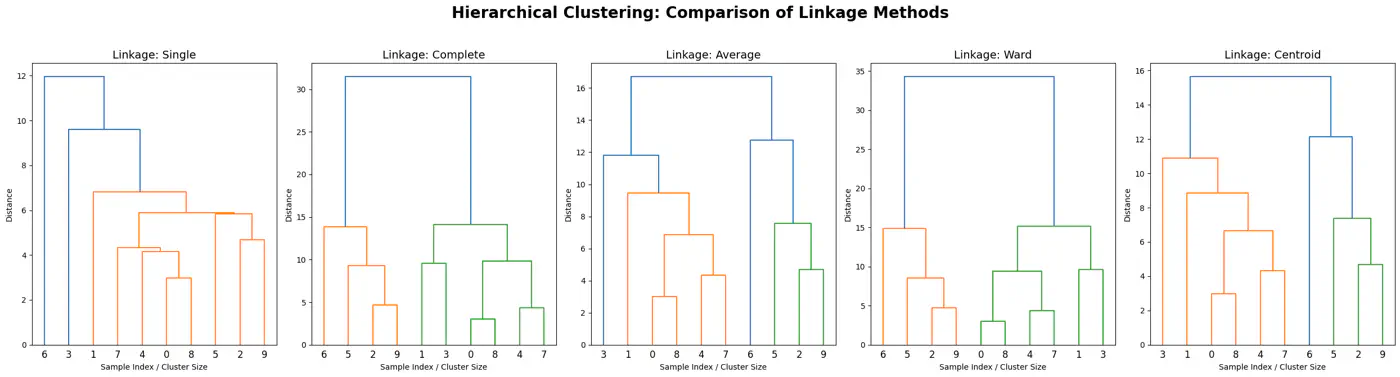

Hierarchical Clustering

⭐️ Method of cluster analysis that seeks to build a hierarchy of clusters, resulting in a tree like structure called dendrogram.

👉Hierarchical clustering allows us to explore different possibilities (of ‘k’) by cutting the dendrogram at various levels.

2 Philosophies

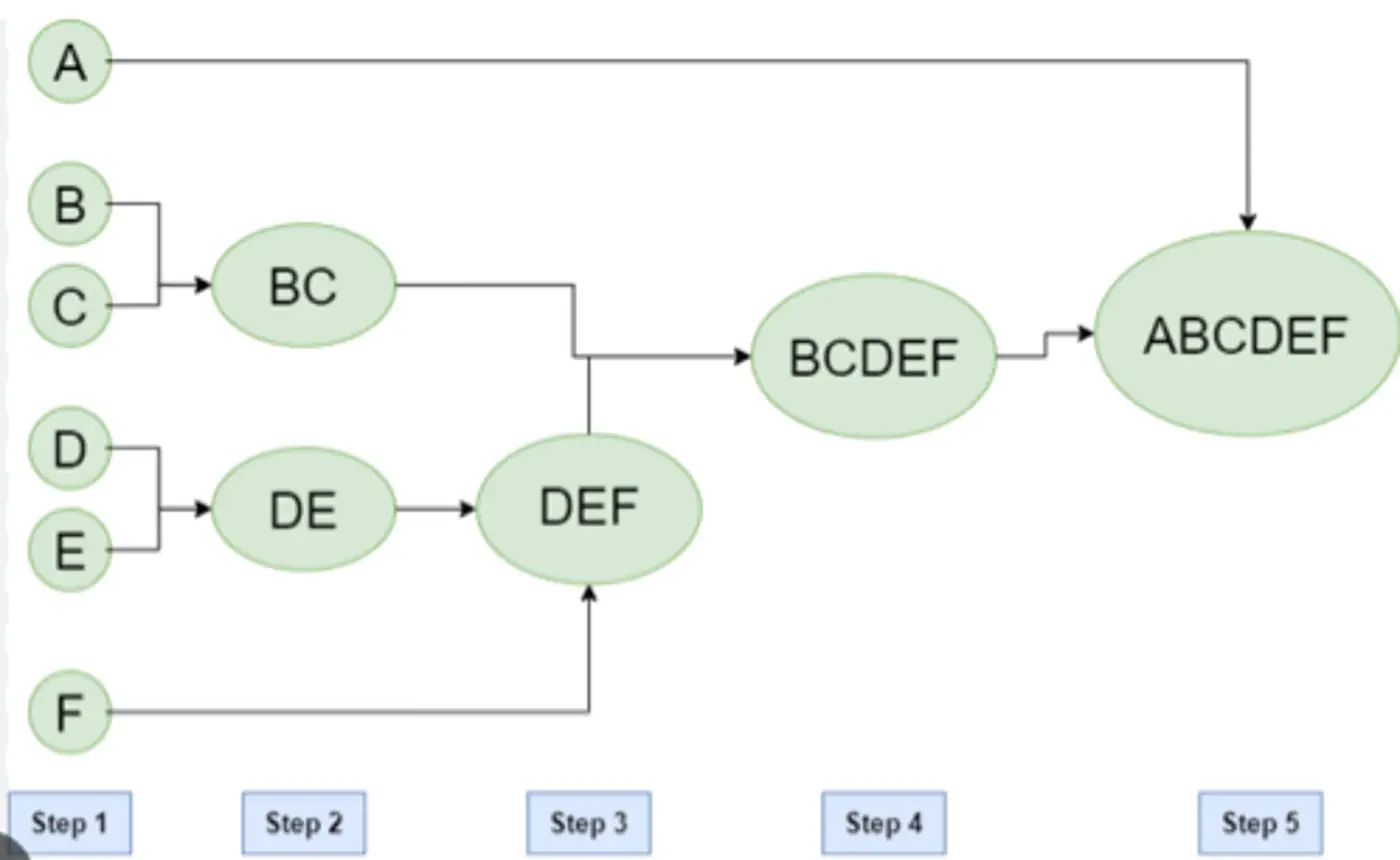

Agglomerative (Bottom-Up): Most common, also known as Agglomerative Nesting (AgNes).

Every data point starts as its own cluster.

In each step, merge the two ‘closest’ clusters.

Repeat step 2, until all points are merged in a single cluster.

Divisive (Top-Down):

All data points start in one large cluster.

In each step, divide the cluster into two halves.

Repeat step 2, until every point is its own cluster.

Agglomerative Clustering Example:

Closeness of Clusters

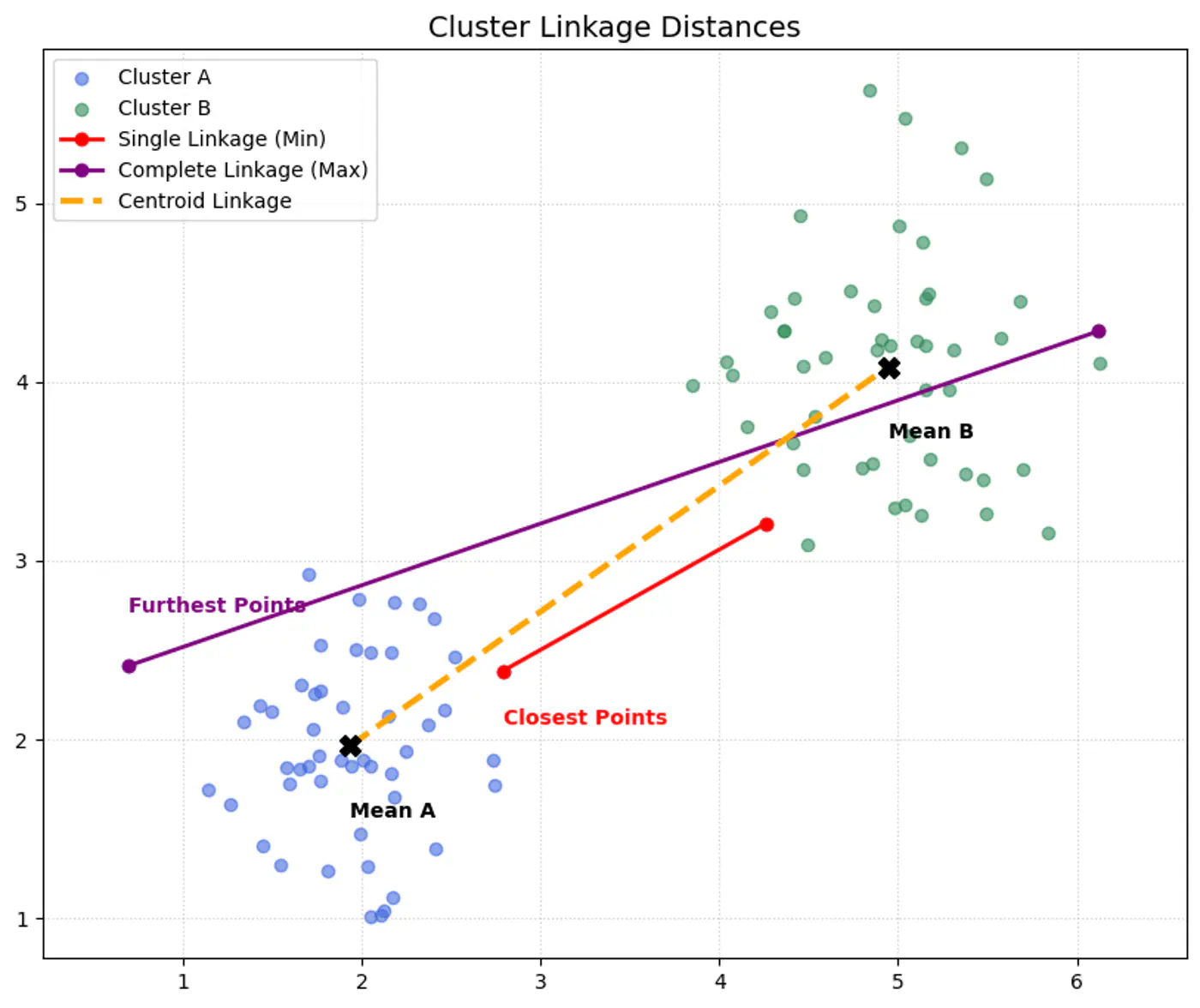

Ward’s Method:

Merges clusters to minimize the increase in the total within-cluster variance (sum of squared errors), resulting in compact, equally sized clusters.

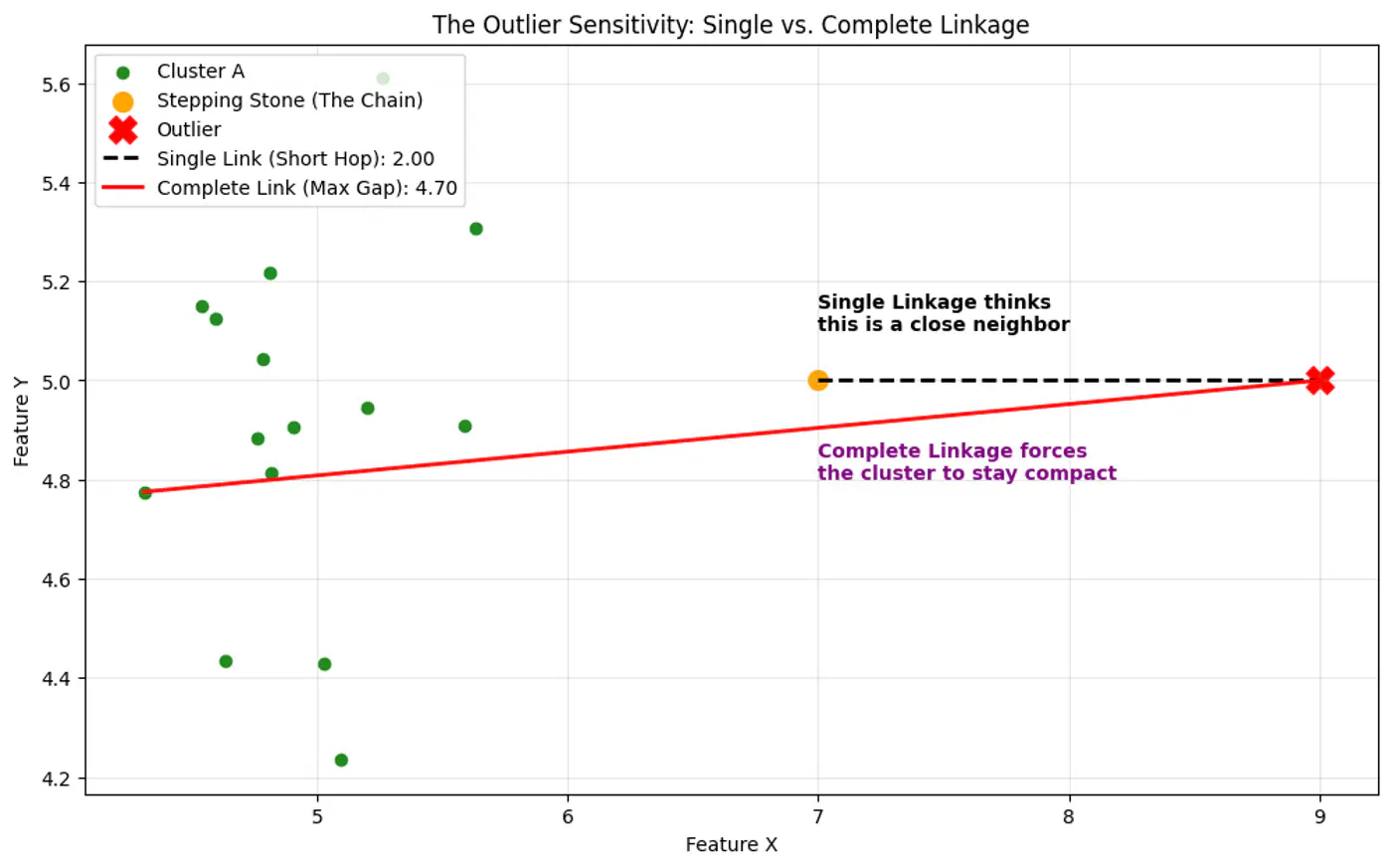

Single Linkage (MIN):

Uses the minimum distance between any two points in different clusters.

Prone to creating long, ‘chain-like’ 🔗 clusters, sensitive to outliers.

Complete Linkage (MAX):

Uses the maximum distance between any two points in different clusters.

Forms tighter, more spherical clusters, less sensitive to outliers than single linkage.

Average Linkage:

Combines clusters by the average distance between all points in two clusters, offering a compromise between single and complete linkage.

A good middle ground, often overcoming limitations of single and complete linkage.

Centroid Method:

Merges clusters based on the distance between their centroids (mean points).

👉Single Linkage is moresensitive to outlier than Complete Linkage, as Single Linkage can keep linking to the closest point

forming a bridge to outlier.

👉All cluster linkage distances.

👉We get different clustering using different linkages.

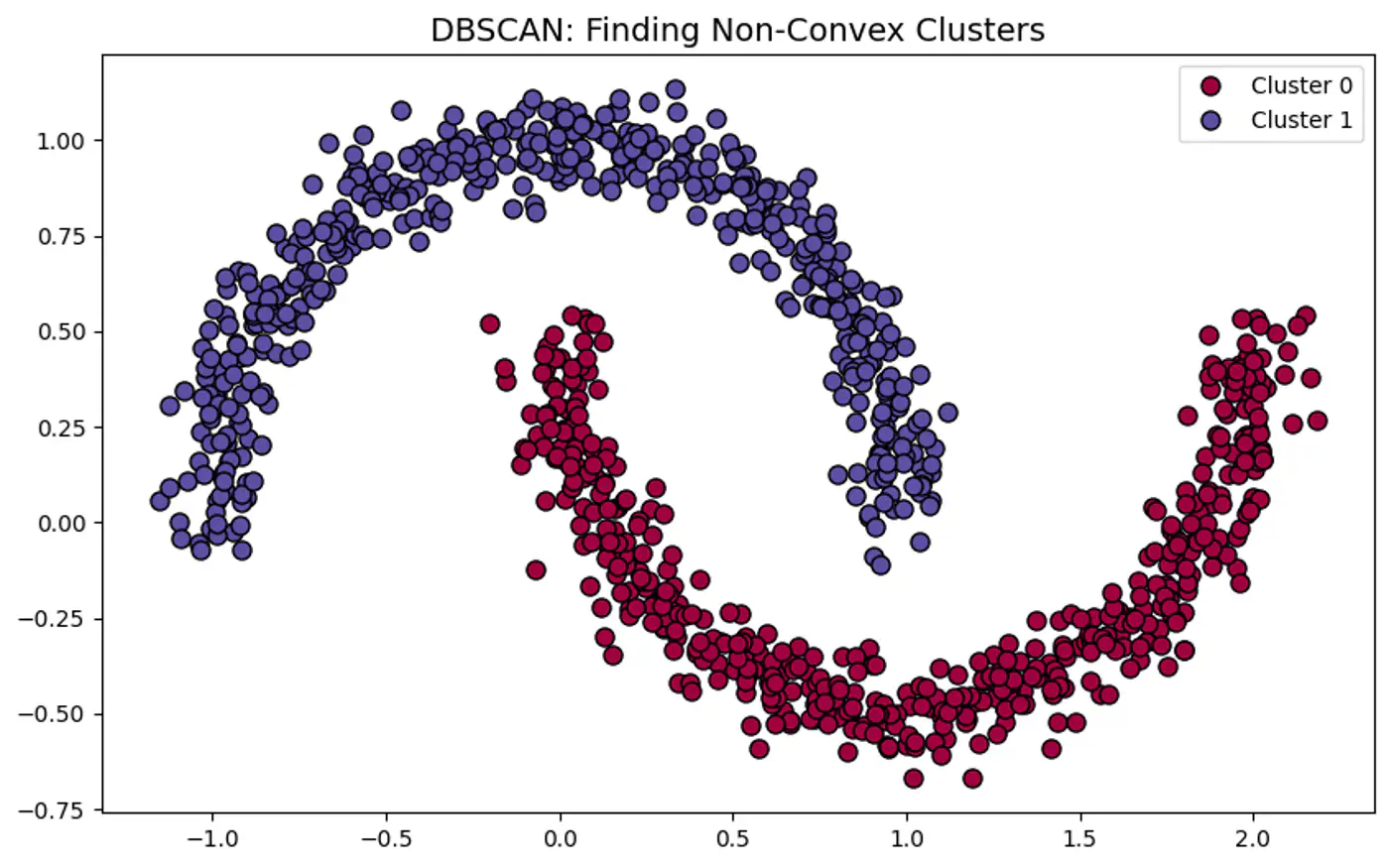

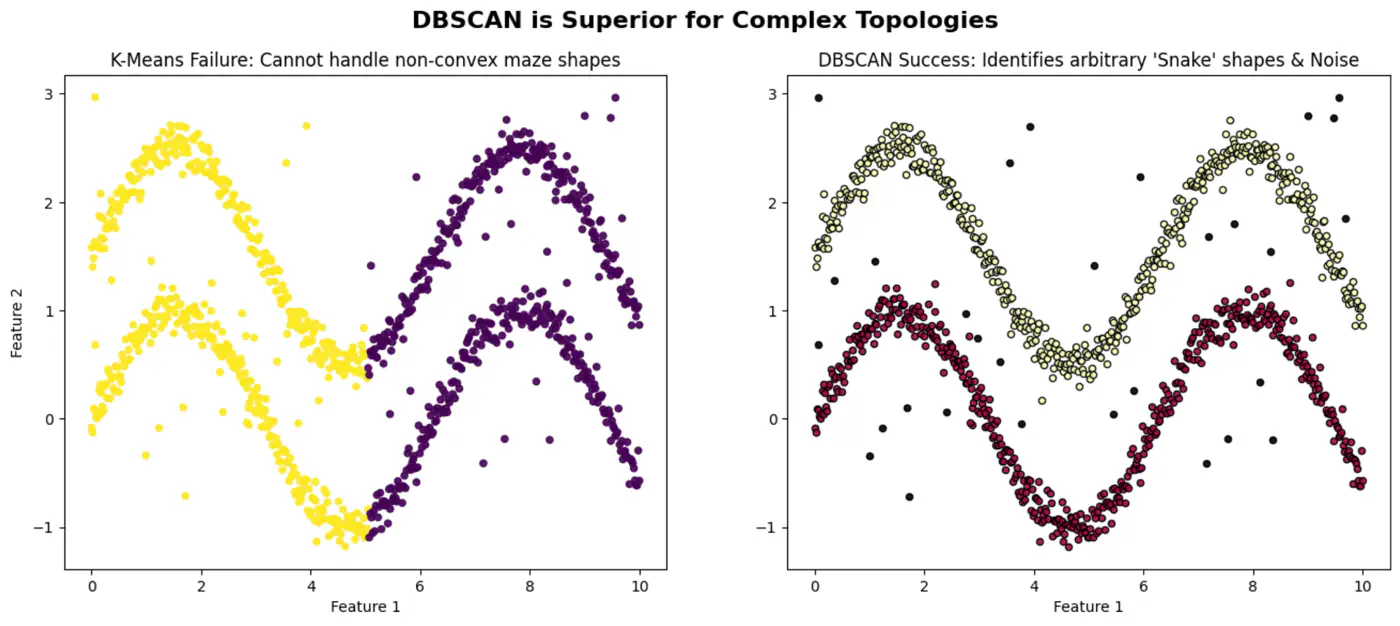

Density Based Spatial Clustering of Application with Noise

Issues with K-Means

Non-Convex Shapes: K-Means can not find ‘crescent’ or ‘ring’ shape clusters.

Noise: K-Means forces every point into a cluster, even outliers.

Main Question for Clustering ?

👉K-Means asks:

“Which center is closest to this point?”

👉DBSCAN asks:

“Is this point part of a dense neighborhood?”

Intuition 💡

Cluster is a contiguous region of high density in the data space, separated from other clusters by areas of low density.

DBSCAN

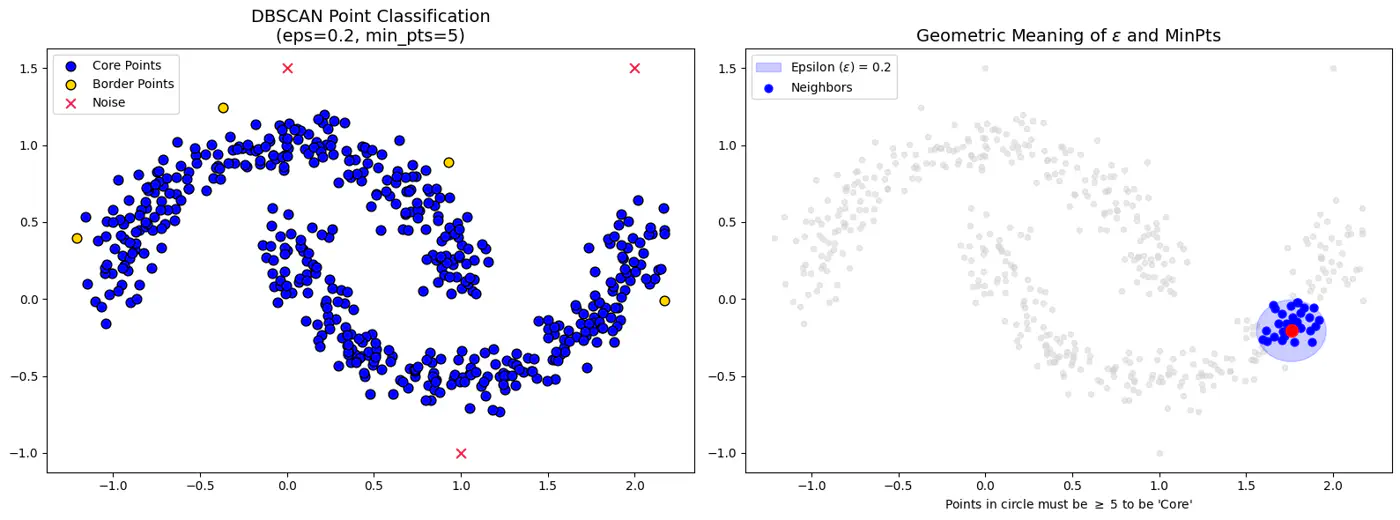

⭐️Groups closely packed data points into clusters based on their density, and marks points that lie alone in low-density regions as outliers or noise.

Note: Unlike K-means, DBSCAN can find arbitrarily shaped clusters and does not require the number of clusters to be specified beforehand.

Hyper-Parameters 🎛️

Epsilon (eps or \(\epsilon\)):

Radius that defines the neighborhood around a data point.

If it’s too small, many points will be noise, and if too large, distinct clusters may merge.

Minimum Points(minPts or min_samples):

Minimum number of data points required within a point’s -neighborhood for that point to be considered a dense region (a core point).

Defines threshold for ‘density’.

Rule of thumb: minPts dimensions + 1; use larger value for noisy data (minPts 2*dimensions).

Types of Points

Core Point:

If it has at least minPts (including itself) within its -neighborhood.

Forms the dense backbone of the clusters and can expand them.

Border Point:

If it has at fewer than minPts within its -neighborhood but falls within the -neighborhood of a core point.

Border points belong to a cluster but cannot expand it further.

Noise Point (Outlier):

If it is neither a core point nor a border point, i.e., it is not density-reachable from any core point.

Not assigned to any cluster.

DBSCAN Algorithm ⚙️

Random Start:

Mark all points as unvisited; pick an arbitrary unvisited point ‘P’ from the dataset.

Density Check:

Check the point P’s ϵ-neighborhood.

If ‘P’ has at least minPts, it is identified as a core point, and a new cluster is started.

If it has fewer than minPts, the point is temporarily labeled as noise (it might become a border point later).

Cluster Expansion:

Recursively visit all points in P’s ϵ-neighborhood.

If they are also core points, their neighbors are added to the cluster.

Iteration 🔁:

This ‘density-reachable’ logic continues until the cluster is fully expanded.

The algorithm then picks another unvisited point and repeats the process, discovering new clusters or marking more points as noise until all points are processed.

👉DBSCAN can correctly detect non-spherical clusters.

👉DBSCAN Points and Epsilon-Neighborhood.

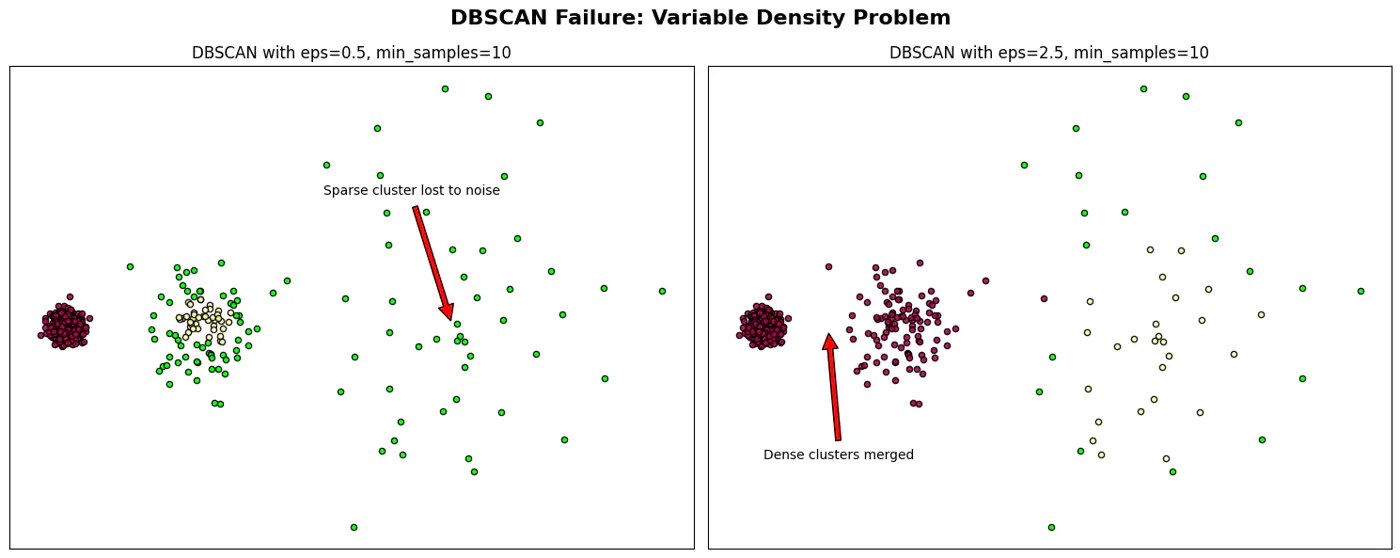

When DBSCAN Fails ?

Varying Density Clusters:

Say A cluster is very dense and B is sparse, a single cannot satisfy both clusters.

High Dimensional Data:

‘Curse of Dimensionality’ - In high-dimensional space, the distance between any two points converge.

Note: Sensitive to parameter eps and minPts; tricky to get it work.

👉DBSCAN Failure and Epsilon ((\epsilon)

When to use DBSCAN ?

Arbitrary Cluster Shapes:

When clusters are intertwined, nested, or ‘moon-shaped’; where K-Means would fail by splitting them.

Presence of Noise and Outliers:

Robust to noise and outliers because it explicitly identifies low-density points as noise (labeled as -1) rather than forcing them into a cluster.

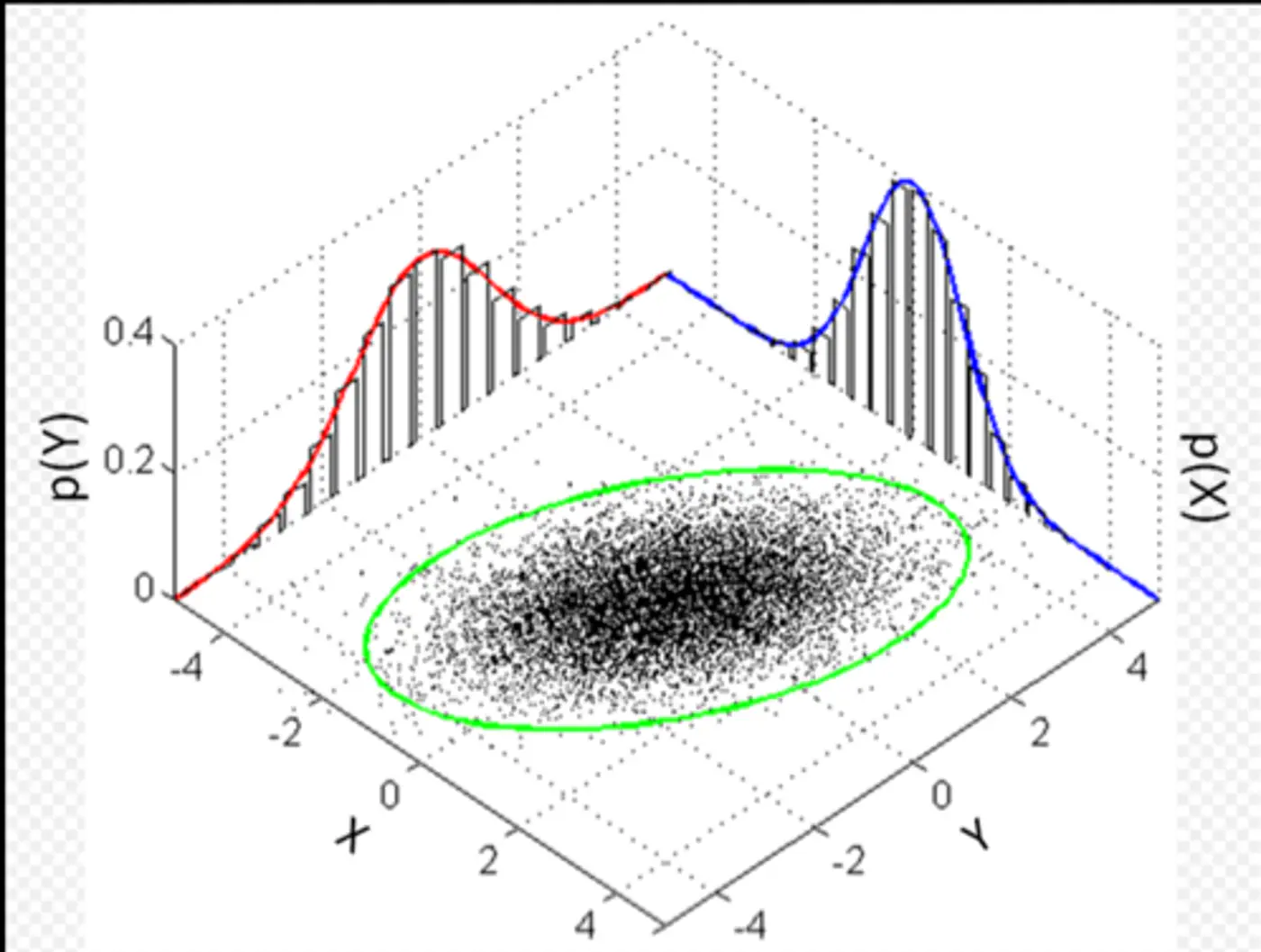

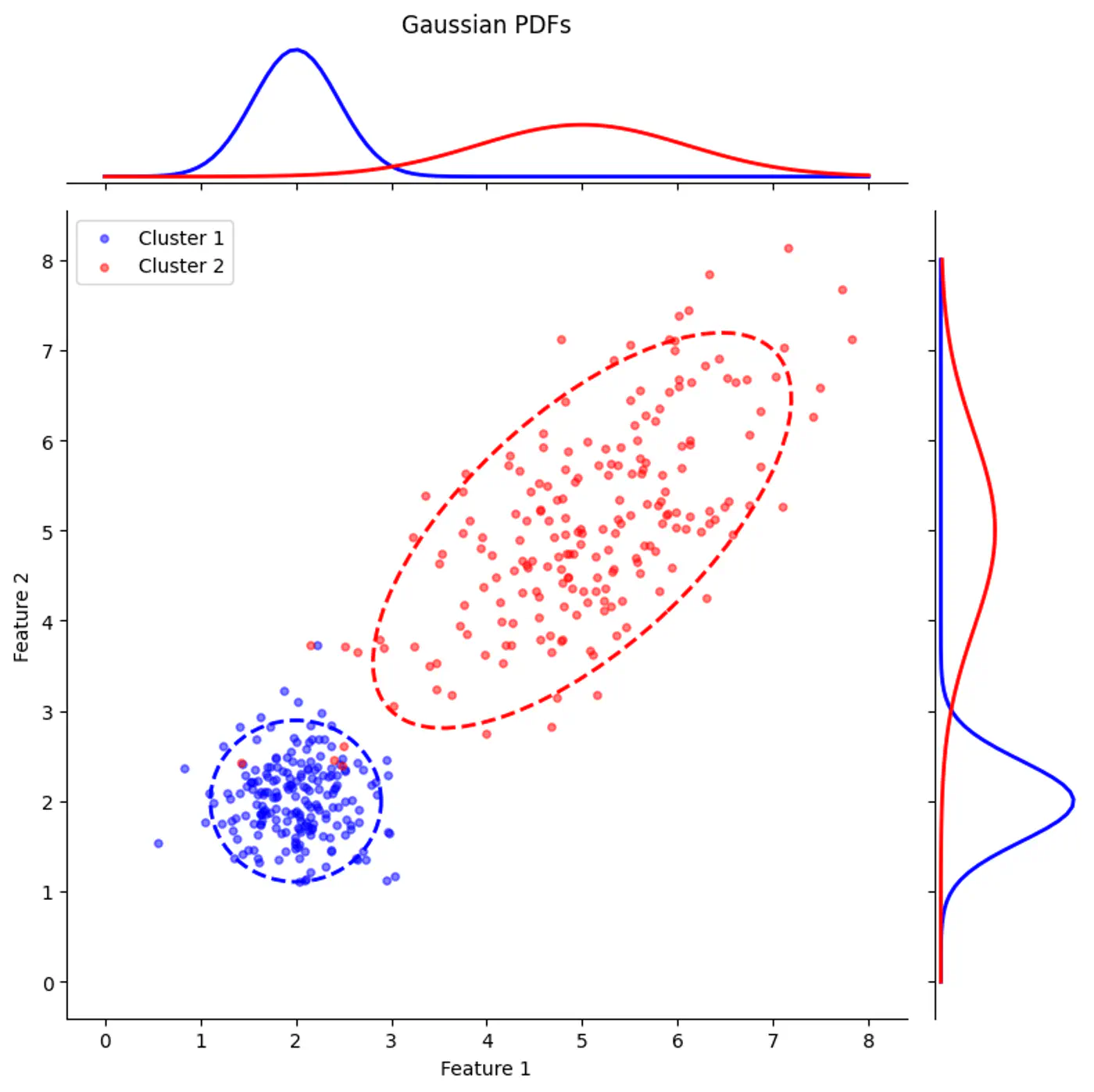

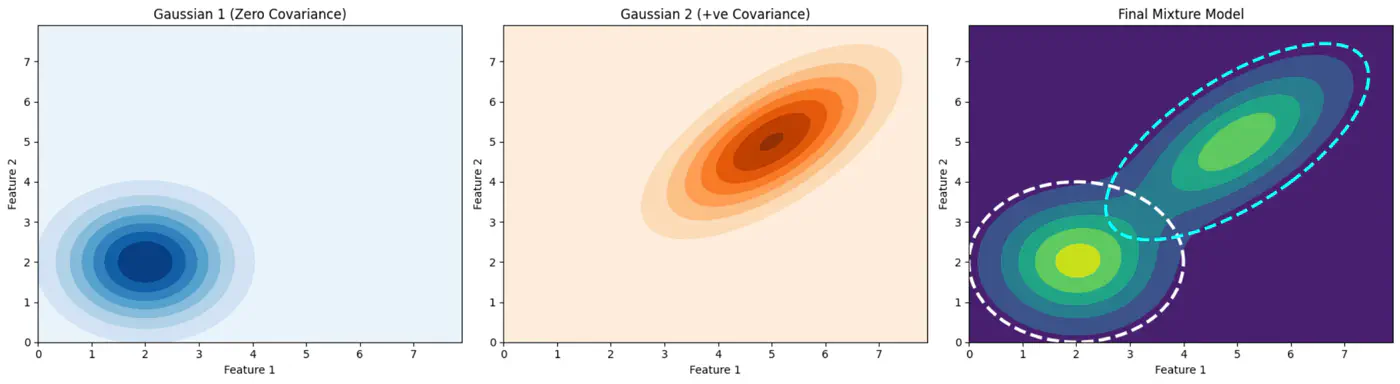

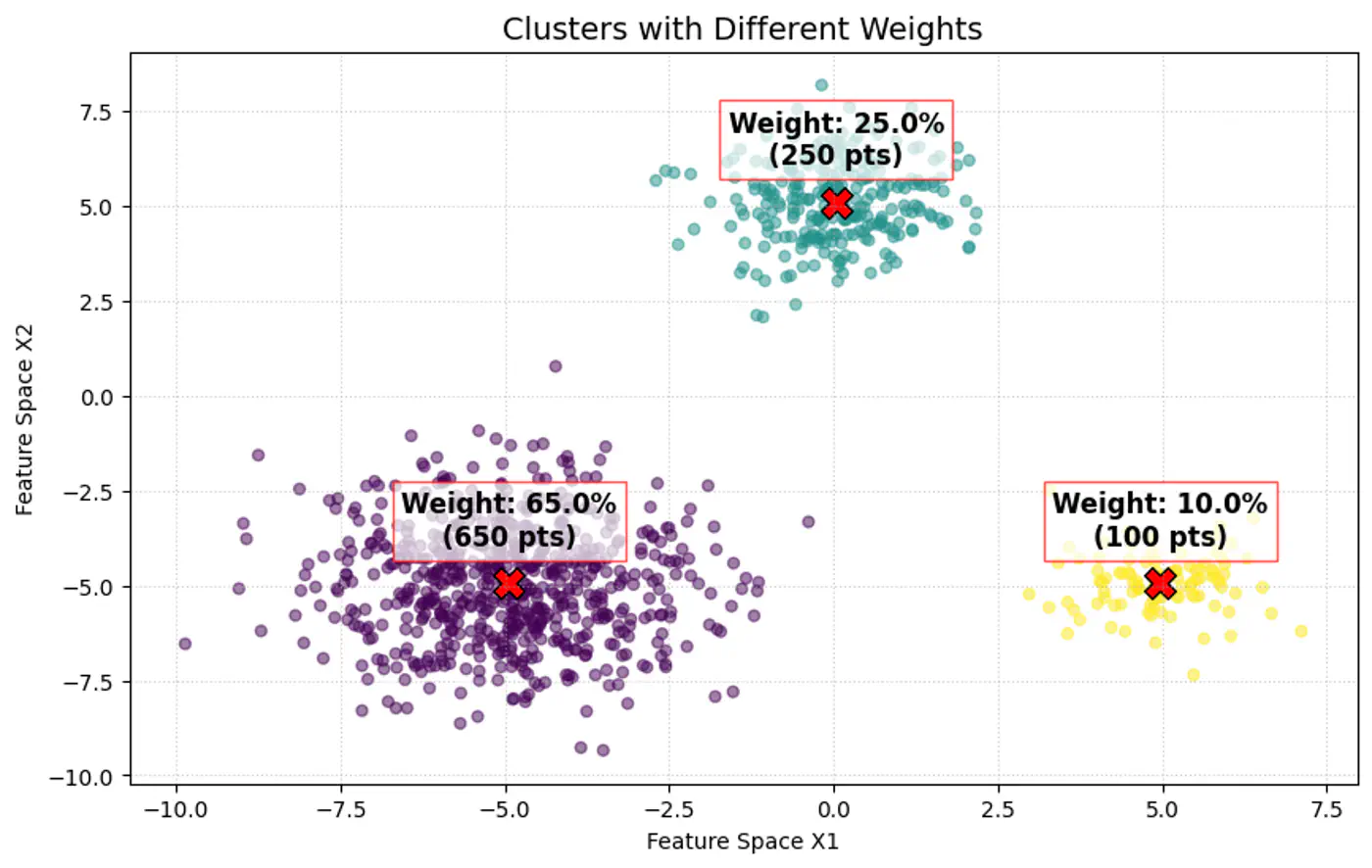

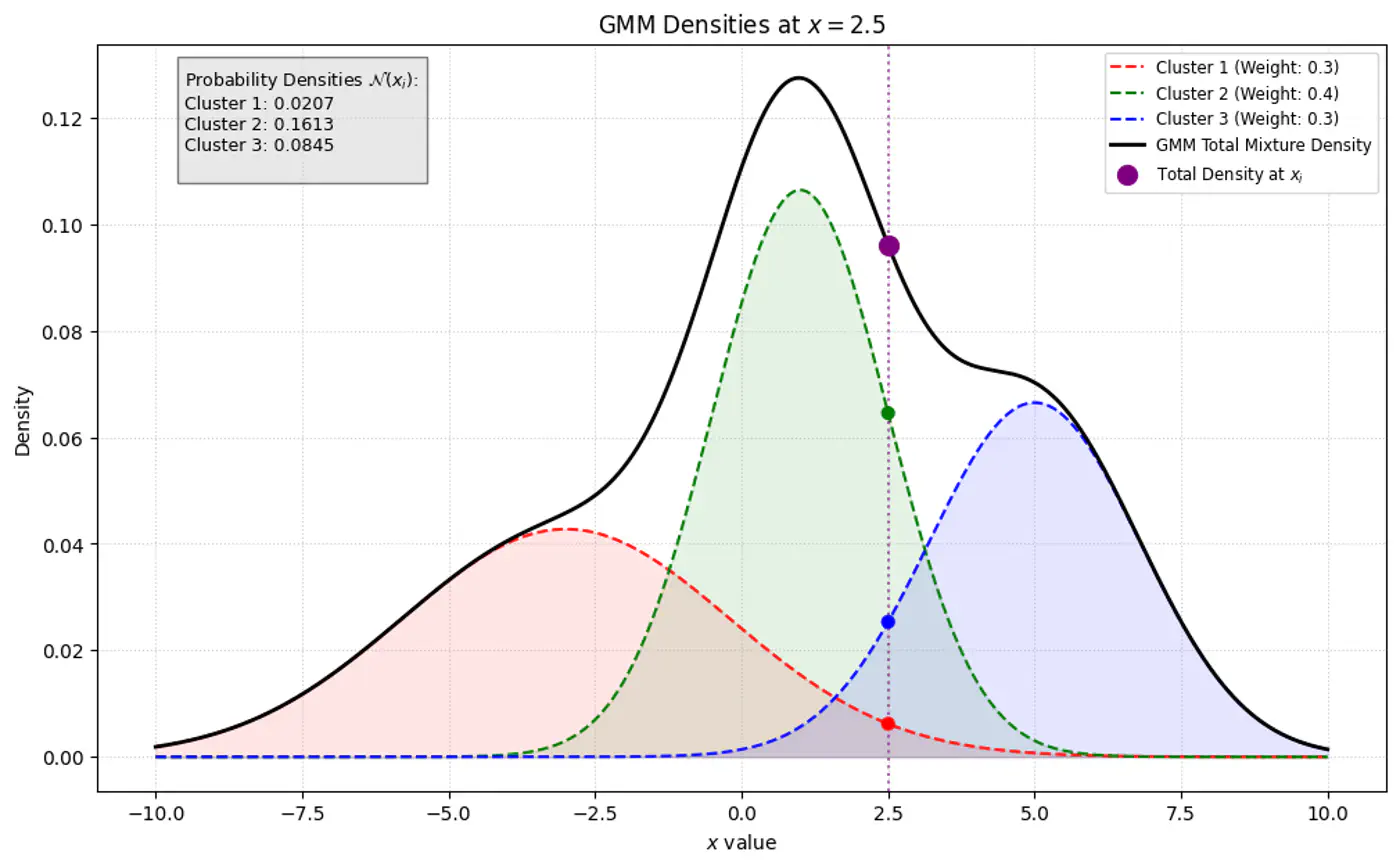

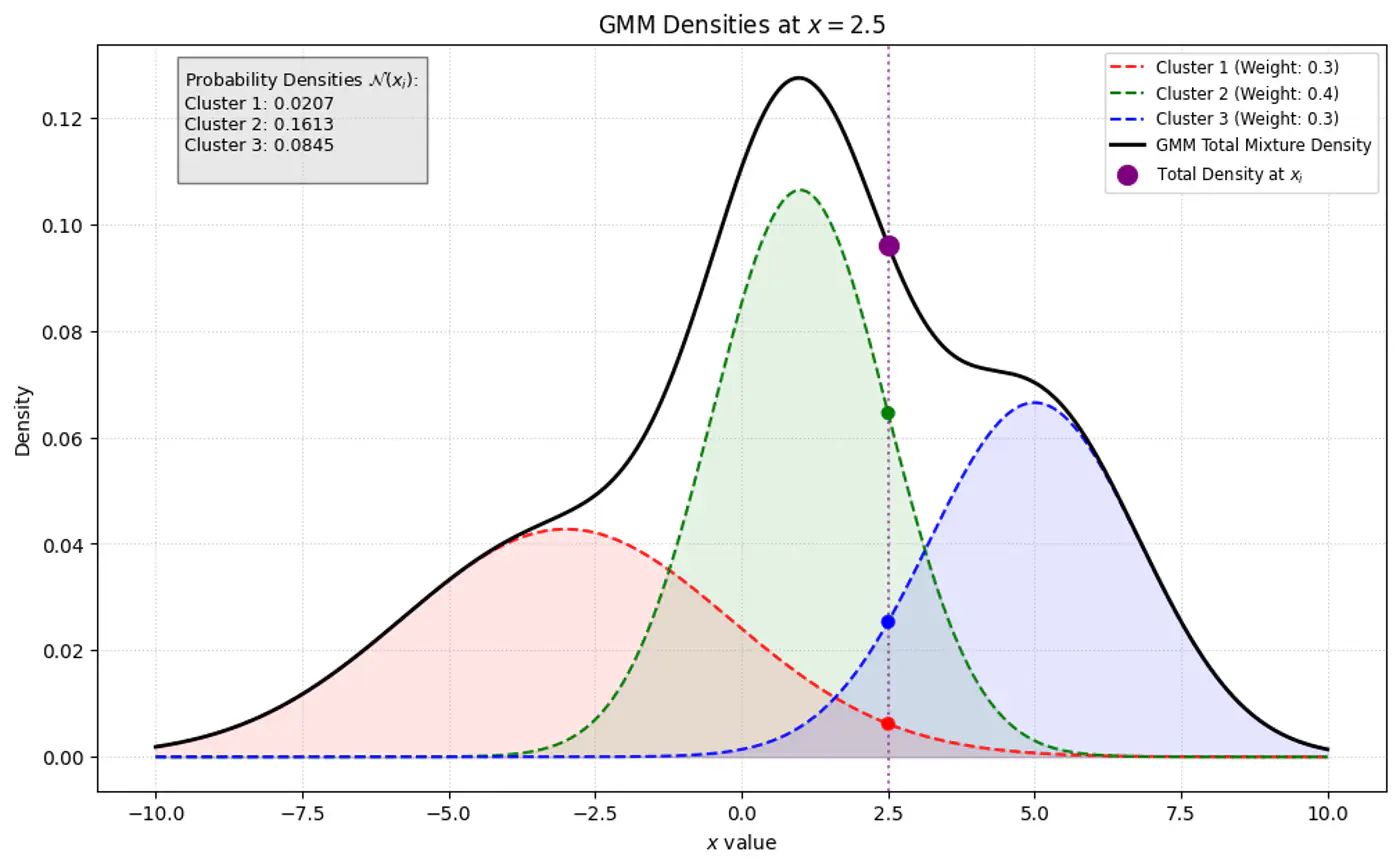

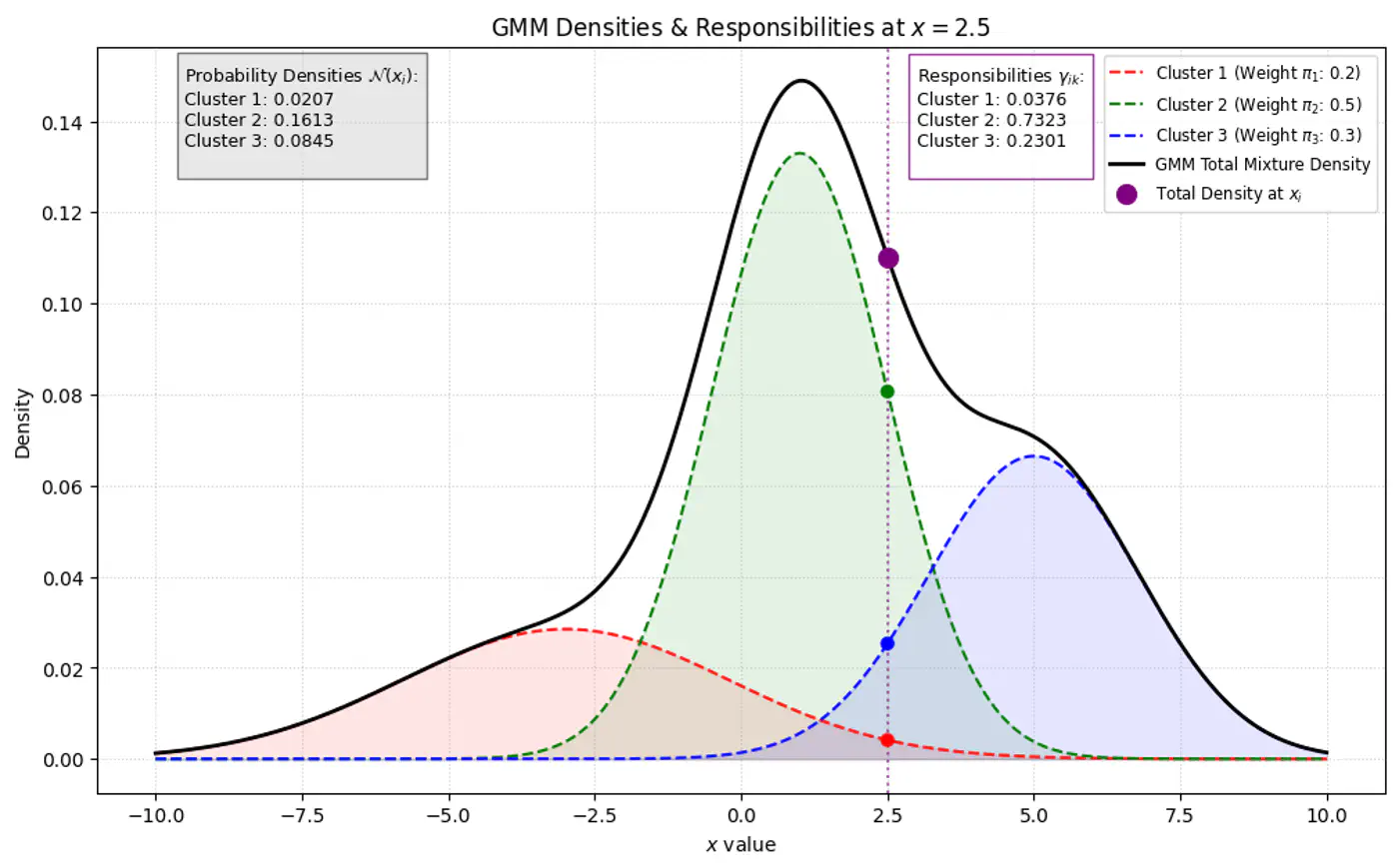

\(\pi_k\): mixing coefficient (weight) of the k-th component, such that, \(\pi_k \ge 0\) and \(\sum _{k=1}^{K}\pi _{k}=1\).

\(\mathcal{N}(x_i|\mathbf{\mu }_{k},\mathbf{\Sigma }_{k})\): probability density function of the k-th Gaussian component

with mean \(\mu_k\) and covariance matrix \(\Sigma_k\).

\(\mathbf{\theta }=\{(\pi _{k},\mathbf{\mu }_{k},\mathbf{\Sigma }_{k})\}_{k=1}^{K}\): complete set of parameters to be estimated.

👉 Weight of the cluster is proportional to the number of points in the cluster.

👉Below image shows the weighted Gaussian PDF, given the weights of clusters.

GMM Optimization (Why MLE Fails?)

🎯 Goal of a GMM optimization is to find the set of parameters \(\Theta =\{(\pi _{k},\mu _{k},\Sigma _{k})\mid k=1,\dots ,K\}\) that maximize the likelihood of observing the given data.

⭐️Imagine we are measuring the heights of people in a college.

We see a distribution with two peaks (bimodal).

We suspect there are two underlying groups:

Group A (Men) and Group B (Women).

Observation:

Observed Variable (X): Actual height measurements.

Latent Variable (Z): The ‘label’ (Man or Woman) for each person.

Note: We did not record gender, so it is ‘hidden’ or ‘latent’.

Latent Variable Model

A Latent Variable Model assumes that the observed data ‘X’ is generated by first picking a latent state ‘z’

and then drawing a sample from the distribution associated with that state.

GMM as Latent Variable Model

⭐️GMM is a latent variable model, meaning each data point \(\mathbf{x}_{i}\) is assumed to have an associated unobserved (latent) variable

\(z_{i}\in \{1,\dots ,K\}\) indicating which component generated it.

Note: We observe the data point, but we do not observe which cluster it belongs to (\(z_i\)).

Latent Variable Purpose

👉If we knew the value of \(z_i\) (component indicator) for every point, estimating the parameters of each Gaussian component would be straightforward.

Note: The challenge lies in estimatingboth the parameters of the Gaussians and the values

of the latent variables simultaneously.

The log-likelihood of the ‘complete data’ simplifies into a sum of logarithms:

\[\sum _{i}\log (\pi _{z_{i}}\mathcal{N}(x_{i}|\mu _{z_{i}},\Sigma _{z_{i}}))\]

Every point is assigned to exactly one cluster, so the sum disappears because there is only one cluster responsible for that point.

Note: This allows the logarithm to act directly on the exponential term of the Gaussian, leading to simple linear equations.

Hard Assignment Simplifies Estimation

👉When ‘z’ is known, every data point is ‘labeled’ with its parent component. To estimate the parameters (mean \(\mu_k\) and covariance \(\Sigma_k\)) for a specific component ‘k’ :

Gather all data points \(x_i\), where \(z_i\)= k.

Calculate the standard Maximum Likelihood Estimate.(MLE) for that single Gaussian using only those points.

Closed-Form Solution

⭐️ Knowing ‘z’ provides exact counts and component assignments, leading to direct formulae for the parameters:

Mean (\(\mu_k\)): Arithmetic average of all points assigned to component ‘k’.

Covariance (\(\Sigma_k\)): Sample covariance of all points assigned to component ‘k’.

Mixing Weight (\(\pi_k\)): Fraction of total points assigned to component ‘k’.

⭐️GMM is a latent variable model, where the variable \(z_i\) is a latent (hidden) variable that indicates which specific

Gaussian component or cluster generated a particular data point.

Chicken 🐓 & Egg 🥚 Problem

If we knew the parameters (\(\mu, \Sigma, \pi\)) we could easily calculate which cluster ‘z’ each point belongs to (using probability).

If we knew the cluster assignments ‘z’ of each point, we could easily calculate the parameters for each cluster (using simple averages).

🦉But we do not know either of them, as the parameters of the Gaussians - we aim to find and

cluster indicator latent variable is hidden.

Break the Loop 🔁

⛓️💥Guess one, i.e, cluster assignment ‘z’ to find the other, i.e, parameters \(\mu, \Sigma, \pi\).

But \(z_{ik}\) is a ‘hard’ assignment’ (either ‘0’ or ‘1’).

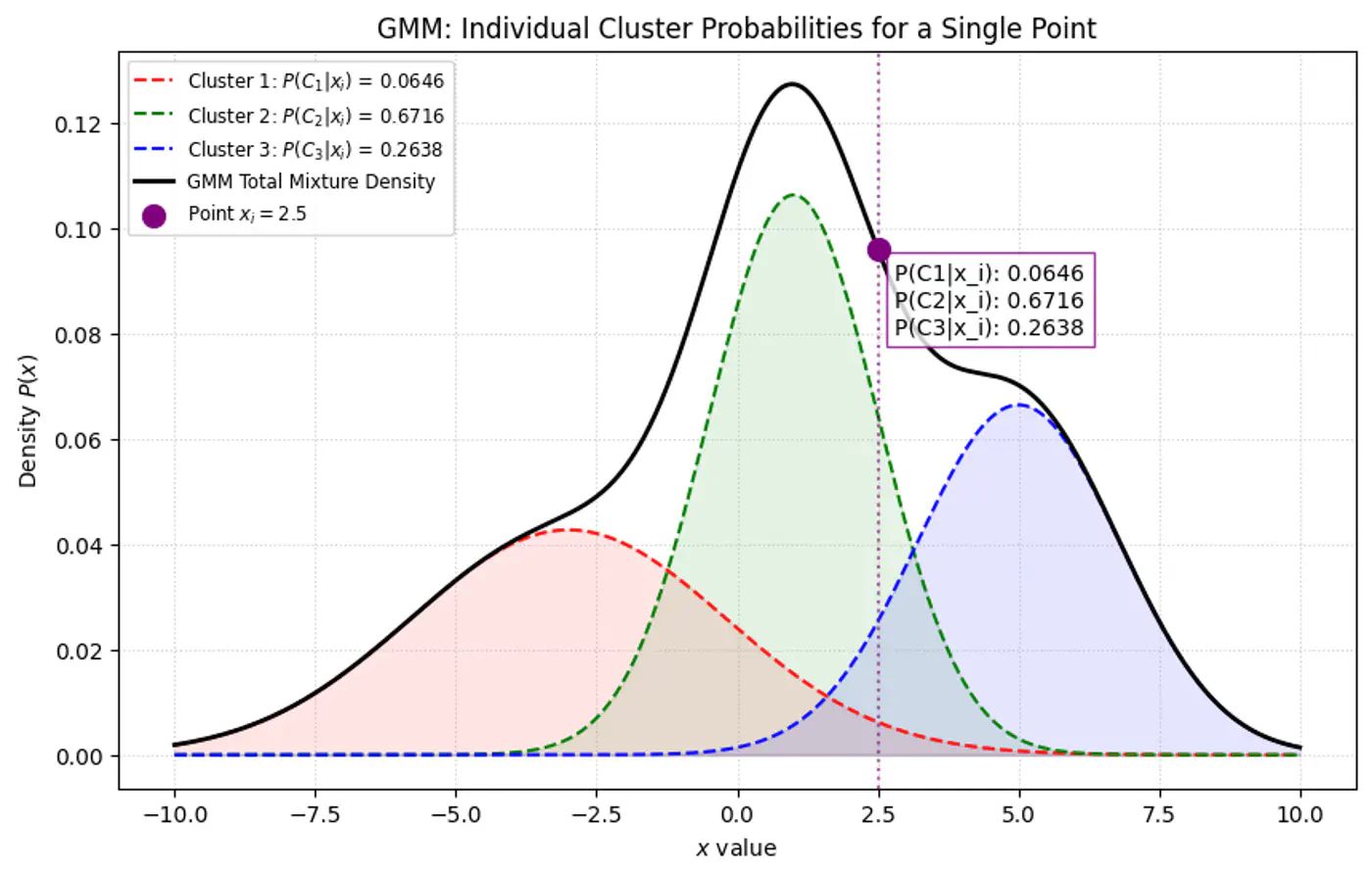

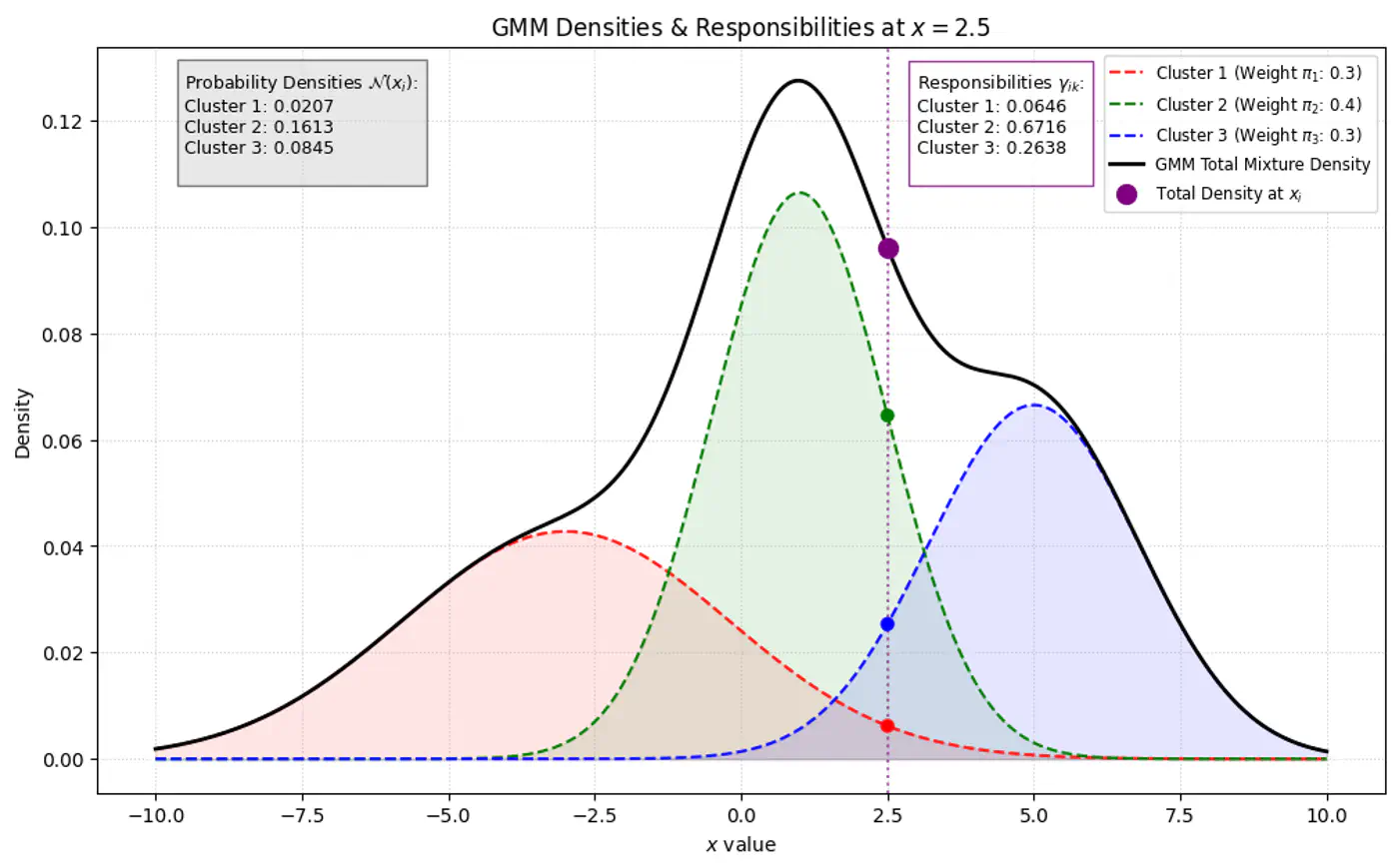

🦆 Because we do not observe ‘z’, we use another variable ‘Responsibility’ (\(\gamma_{ik}\)) as

a ‘soft’ assignment (value between 0 and 1).

🐣 \(\gamma_{ik}\) is the expected value of the latent variable \(z_{ik}\), given the observed data \(x_{i}\) and

parameters \(\Theta\).

\[\gamma _{ik}=E[z_{ik}\mid x_{i},\theta ]=P(z_{ik}=1\mid x_{i},\theta )\]

Note: \(\gamma_{ik}\) is the posterior probability (or ‘responsibility’) that cluster ‘k’ takes for

explaining data point \(x_{i}\).

⭐️Using Bayes’ Theorem, we derive responsibility (posterior probability that component ‘k’ generated data point \(x_i\))

by combining the prior/weights (\(\pi_k\)) and the likelihood (\(\mathcal{N}(x_{i}\mid \mu _{k},\Sigma _{k})\)).

\(\pi_k\) : Probability that a randomly selected data point \(x_i\) belongs to the k-th component before we even look

at the specific value of \(x_i\), such that \(\pi_k \ge 0\) and \(\sum _{k=1}^{K}\pi _{k}=1\).

Maximization Step

👉Update the parameters (\(\mu, \Sigma, \pi\)) by calculating weighted versions of the standard MLE formulas using responsibilities as weight 🏋️♀️.

🦄 Anomaly is a rare item, event or observation which deviates significantly from the majority of the data and does

not conform to a well-defined notion of normal behavior.

Note: Such examples may arouse suspicions of being generated by a different mechanism, or appear inconsistent

with the remainder of that set of data.

Anomaly Detection

🐙 Anomaly detection (Outlier detection or Novelty detection) is the identification of unusual patterns

or anomalies or outliers in a given dataset.

What to do with Outliers ?

❌ Remove Outliers:

Rejection or omission of outliers from the data to aid statistical analysis, for example to compute the mean or standard deviation of the dataset.

Remove outliers for better predictions from models, such as linear regression.

🔦Focus on Outliers:

Fraud detection in banking and financial services.

Cyber-security: intrusion detection, malware, or unusual user access patterns.

Anomaly Detection Methods 🐉

Supervised

Semi-Supervised

Unsupervised (most common) ✅

Note: Labeled anomaly data is often unavailable in real-world scenarios.

Known Methods 🐈

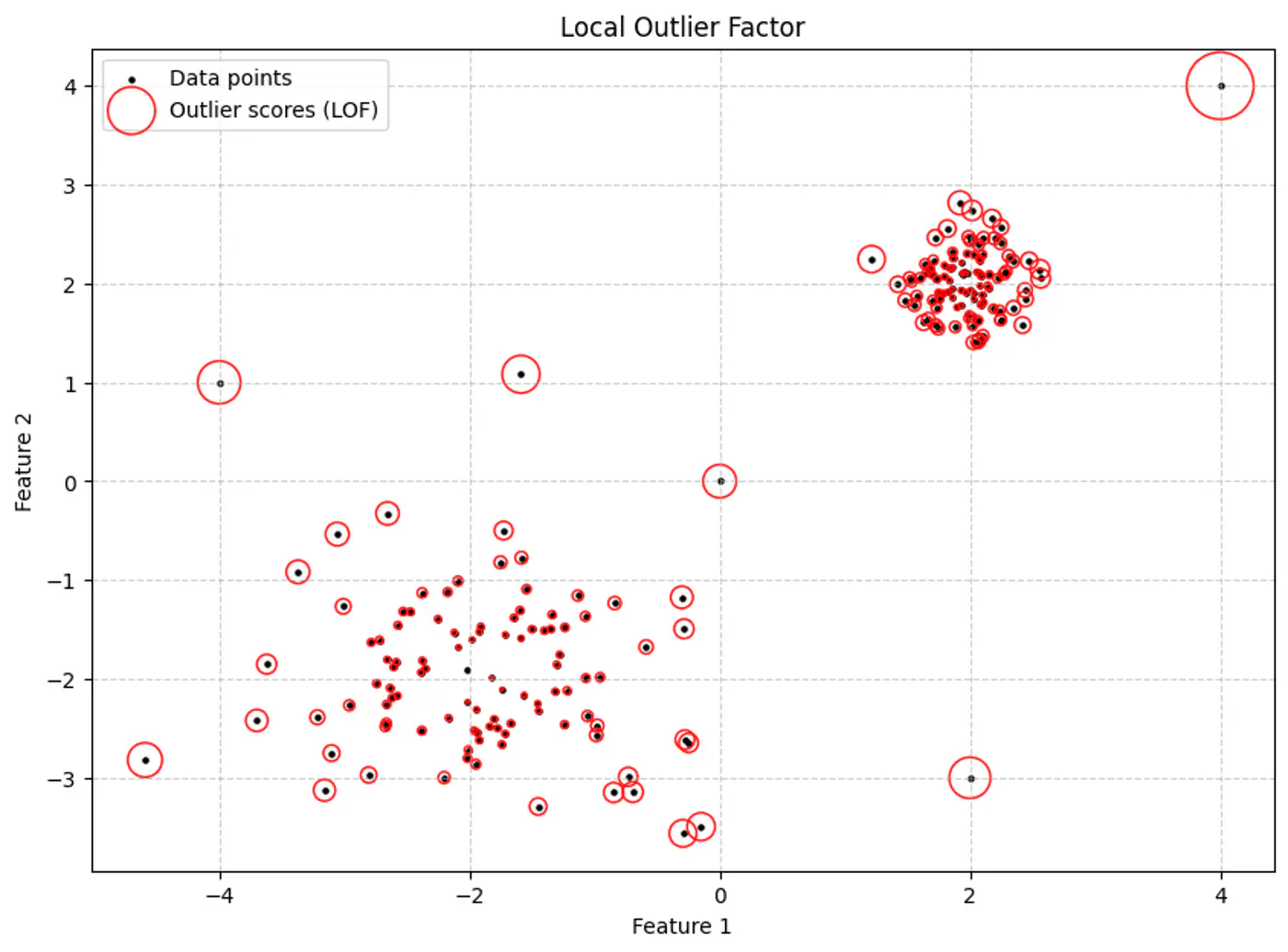

Statistical Methods: Z-Score, large value means outlier, IQR, point beyond fences (Q1 - 1.5*IQR or Q3 + 1.5*IQR) is flagged as an outlier.

Distance Based: KNN, points far from their neighbors as potential anomalies.

Density Based: DBSCAN, points in low density regions are considered outliers.

Clustering Based: K-Means, points far from cluster centroids that do not fit any cluster are anomalies.

Detect anomalies in multivariate Gaussian data, such as, biometric data (height/weight) where features

are normally distributed and correlated.

Assumption: The data can be modeled by a Gaussian distribution.

Intuition 💡

In a normal distribution, most data points cluster around the mean, and the probability density decreases

as we move farther away from the center.

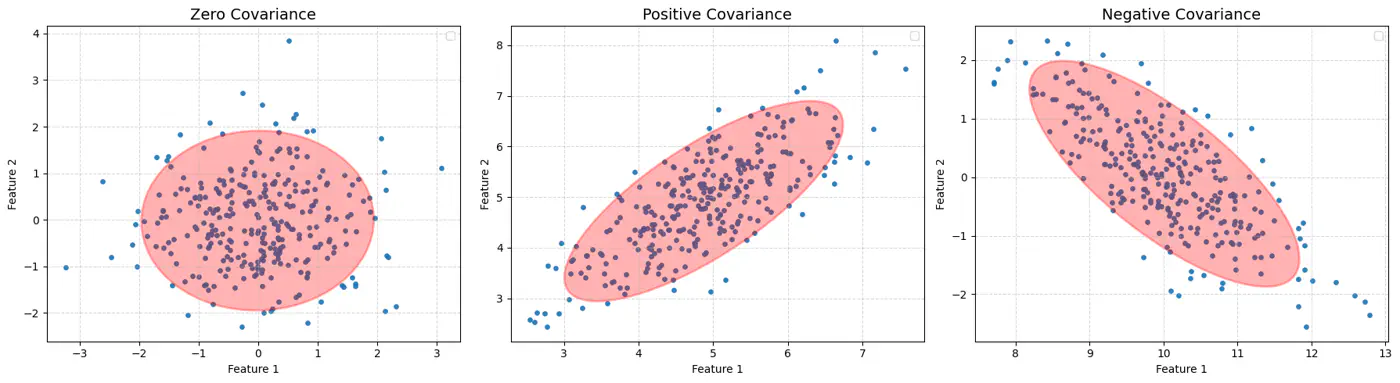

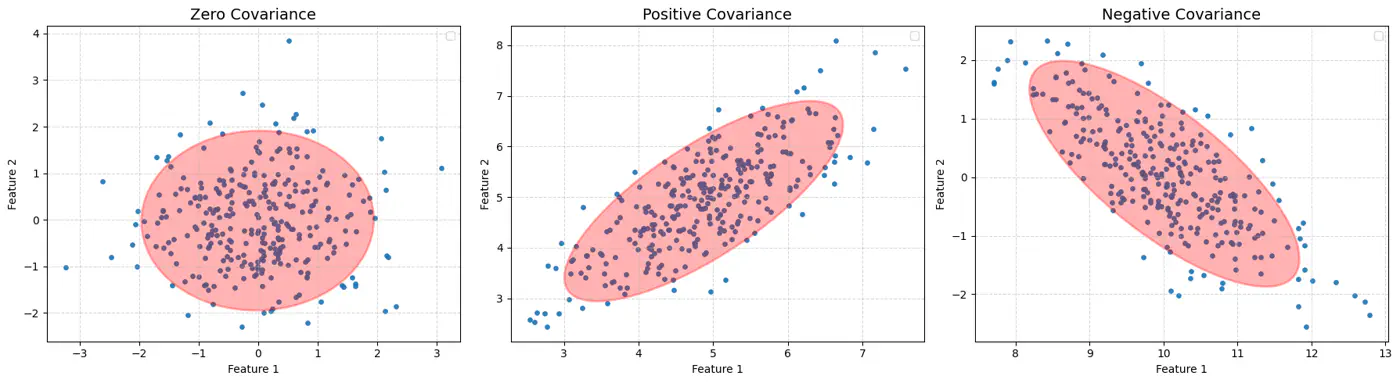

Issue with Euclidean Distance 🐲

🌍 Euclidean distance measures the simple straight-line distance from the center of the cloud.

👉If the data is spherical, this works fine.

🦕 However, real-world data is often stretched or skewed (e.g., taller people are generally heavier),

due to correlations between variables, forming an elliptical shape.

Mahalanobis Distance (Solution)

⭐️Mahalanobis distance essentially re-scales the data so that the elliptical distribution appears spherical,

and then measures the Euclidean distance in that transformed space.

👉This way, it measures how many standard deviations(\(\sigma\)) away a point is from the mean, considering the data’s spread and correlation (covariance).

MCD algorithm is used to find the covariance matrix \(\Sigma\) with minimum determinant, so that the

volume of the ellipsoid is minimized.

Initialization: Select several random subsets of size h < n (default h = \(\frac{n+d+1}{2}\), d = # dimensions),

representing ‘robust’ majority of the data.

Calculate preliminary mean (\(\mu\)) and covariance (\(\Sigma\)) for each random subset.

Concentration Step: Iterative core of the algorithm designed to ‘tighten’ the ellipsoid.

Calculate Distances: Compute the Mahalanobis distance of all ’n’ points in the dataset from the current

subset’s mean (\(\mu\)) and covariance (\(\Sigma\)).

Select New Subset: Identify the ‘h’ points with the smallest Mahalanobis distances.

These are the points most centrally located relative to the current ellipsoid.

Update Estimates: Calculate a new and based only on these ‘h’ most central points.

Repeat 🔁: The steps repeat until the determinant stops shrinking.

Note: Select the best subset that achieved the absolute minimum determinant.

Limitations

Assumptions

Gaussian data.

Unimodal data (single center).

Cost 💰of covariance matrix \(\Sigma^{-1}\) inversion is O(d^3).

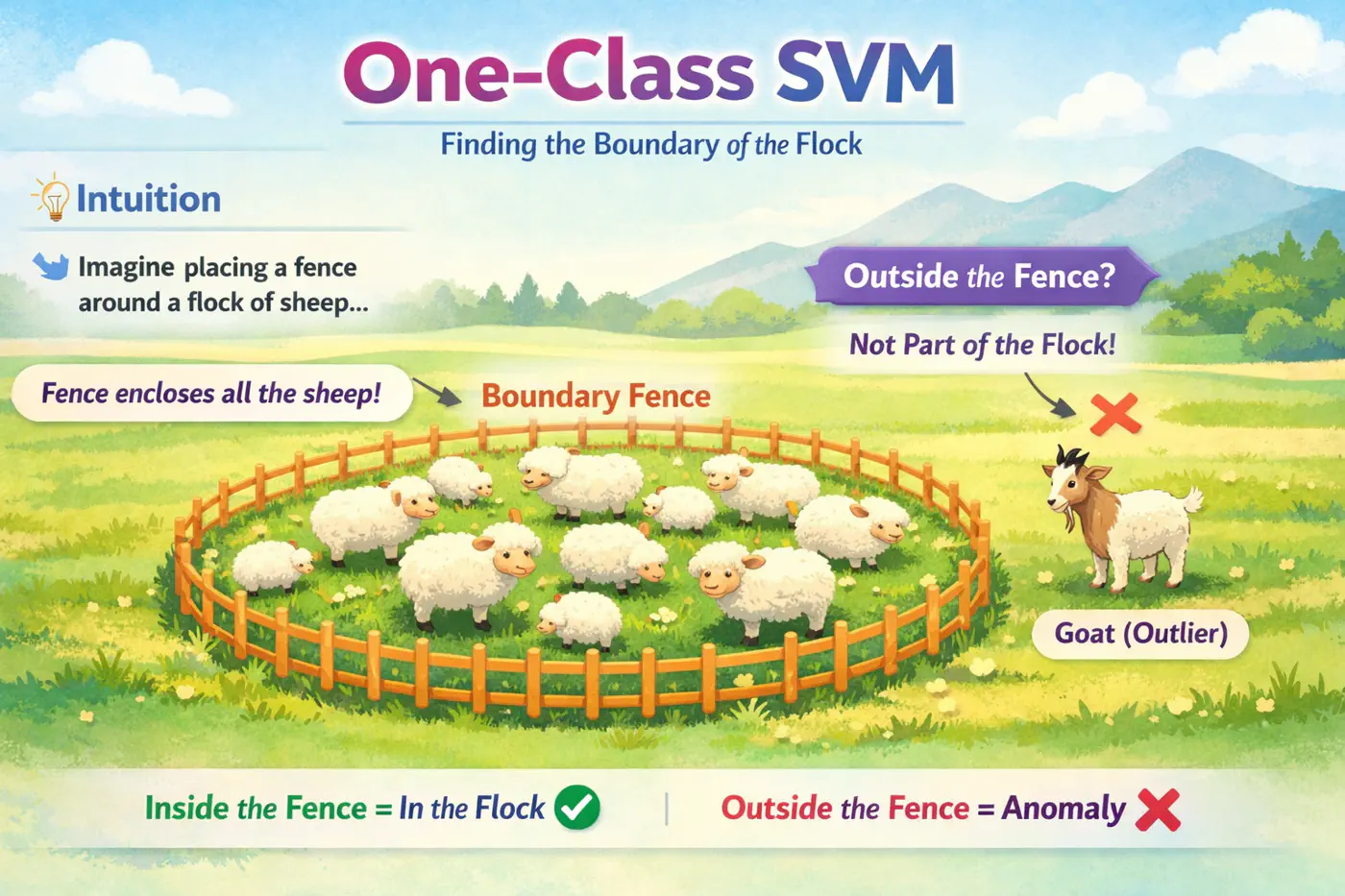

⭐️Only one class of data (normal, non-outlier) is available for training, making standard supervised learning

models impossible.

e.g. Only normal observations are available for fraud detection, cyber attack, fault detection etc.

Intuition

Problem 🦀

🦂 The core problem is to build a model that can distinguish between ‘normal’ and ‘anomalous’ data

when we only have examples of the ‘normal’ class during training.

🦖 We need to find a decision boundary that is as compact as possible while still encompassing the bulk of the

training data.

Solution 🦉

💡Instead of finding a hyperplane that separates two different classes, we find a hyperplane that best separates the

normal data points from the origin (0,0) in the feature space 🚀.

Goal 🎯

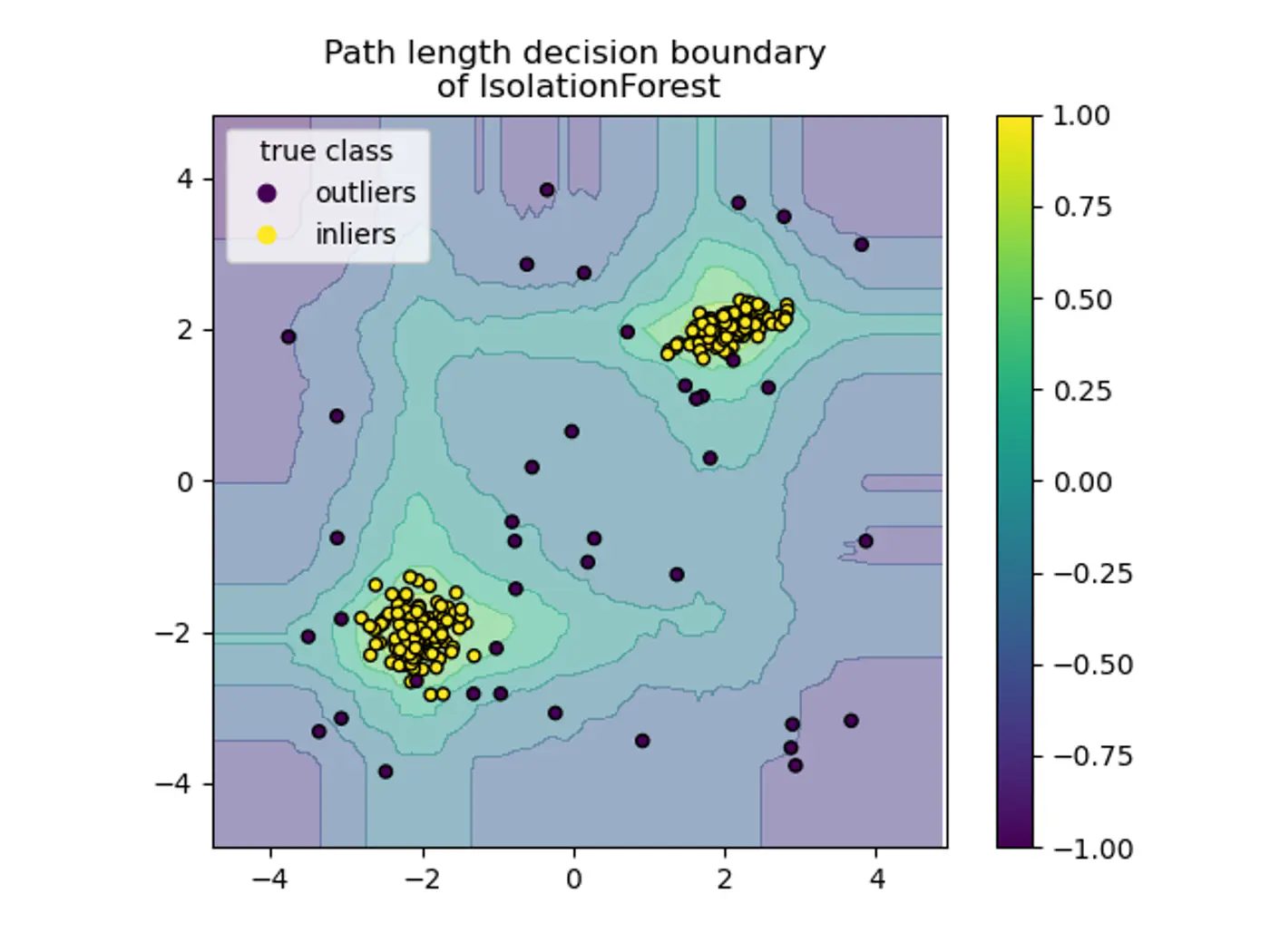

🦍 Define a boundary for a single class in high-dimensional space where data might be non-linearly distributed

(e.g.‘U’ shape).

🦧 Use the Kernel Trick to project data into a higher-dimensional space and find a hyperplane

that separates the data from the origin with the maximum margin.

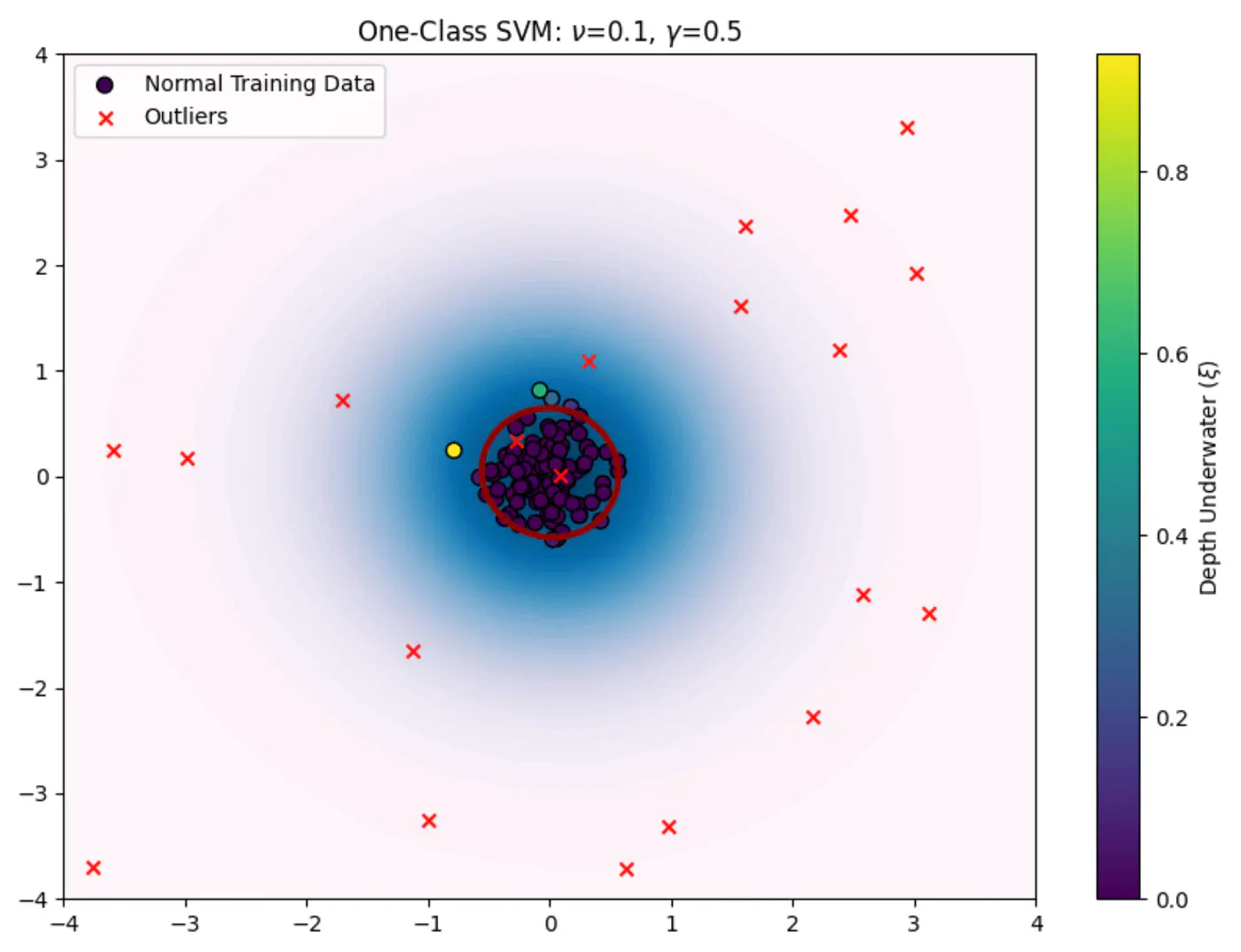

One Class SVM

⭐️OC-SVM, as introduced by Bernhard Schölkopf et al., uses a hyperplane ‘H’ defined by a weight vector \(\mathbf{w}\)

and a bias term \(\rho\).

\(\phi (\mathbf{x}_{i})\): RBF kernel function \(K(x, y) = \exp(-\gamma \|x-y\|^2)\) that maps the data into a higher-dimensional feature space, making it easier to separate from the origin.

\(\mathbf{w}\): normal vector to the separating hyperplane.

\(\rho\): scalar bias term that determines the offset of the hyperplane from the origin.

\(\xi_i\): Slack variables that allow some data points to fall on the ‘wrong’ side of the hyperplane (inside the anomalous region) to prevent overfitting.

N: total number of training points.

\(\nu\): hyper-parameter between 0 and 1. It acts as an upper bound on the fraction of outliers (training data points outside the boundary) and a lower bound on the fraction of support vectors.

Working 🦇

\(\frac{1}{2}\|\mathbf{w}\|^{2}\): aims to maximize the margin/compactness of the region.